Vestis: Recent Spinoff in an Attractive Industry

Vestis’ business of supplying and laundering uniforms to industrial and service companies is about as mundane as it gets, making Vestis an ideal company for us to learn about. Combine a boring, predictable business with 90%+ recurring revenue, a significant margin expansion opportunity, and a motivated and seasoned management team and you’ve got my attention.

Vestis was recently spun-out of Aramark Corporation which is a food service and hospitality business that provides dining services and catering to businesses, schools, and healthcare facilities. Aramark split off its largely unrelated Uniform and Apparel segment in September in a classic spinoff to existing Aramark shareholders and renamed the newly independent company Vestis. As we know, spin offs can occasionally provide interesting investment opportunities, especially when the underlying business is high-quality in nature.

Do you have a “stranded” 401k from a past job that is neglected and unmanaged? These accounts are often an excellent fit for Eagle Point Capital’s long-term investment approach. Eagle Point manages separately manage accounts for retail investors. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Background

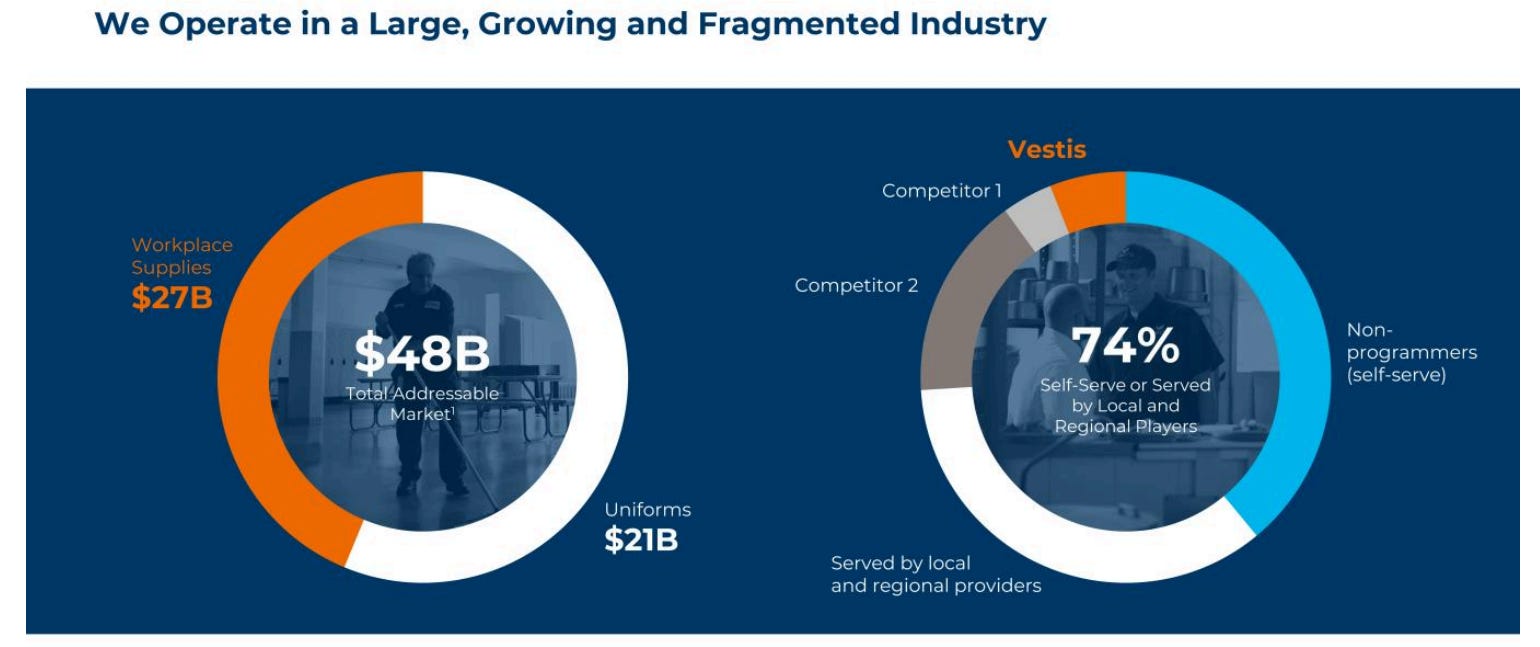

Vestis is the second largest player behind Cintas in the fragmented uniform and workwear industry. The company supplies and launders things like uniforms, towels, mats, and linens to companies in a myriad of industries from manufacturing to restaurants to airlines. They also manage and restock restroom and safety supplies for customers.

Vestis employees usually make weekly stops at their customers to pick up dirty supplies for laundering or repairing, and drop off clean or new uniforms and linens.

The industry structure reminds me of the C-Store space in which Alimentation Couche-Tarde and 7 Eleven dominate amidst a sea of smaller players. Cintas, Vestis, and No. 3 player UniFirst control about 25% of the market with the rest dominated by local and regional players, most of which are private. A large part of the market remains untapped by companies who retain uniform services in house rather than outsource to a dedicated uniform company. There is an ongoing trend of outsourcing this non-core and distracting work to specialists like Vestis and Cintas.

To get an idea of if this type of business can be attractive, look no further than Cintas, which has managed to do OK over the past 10 years. The stock has eked out a mere 25% annual return, or more than 825% in total, since 2014. What makes the business so appealing and potentially lucrative?

Business Model

Supplying and servicing uniforms is a simple, predictable, and cash generative business characterized by recurring revenue, sticky customer relationships, and incredibly high incremental margins.

Recurring Revenue

Vestis is the opposite of a lumpy, project-based business. Their customers need clean uniforms on a regular basis just as you or I need our waste management company to pick up our garbage every week. For instance, employees at Raising Cane’s or American Airlines – two of Vestis’ customers – need a fresh uniform every day, and management does not want to worry about making sure clean uniforms are there on demand, that’s what they pay Vestis for. About 93% of Vestis’ revenue is recurring in nature.

Additionally, the customer base is very diverse and fragmented, meaning Vestis is not subject to the vagaries of a specific industry, let alone customer.

In a broad-based recession when employment falls significantly, Vestis would likely see a temporary dip in its business. That aside, the business is unlikely to prove highly cyclical.

Sticky Customer Relationship

Vestis and Cintas benefit from the coveted “low price to value” customer relationship. Transdigm has thrived on this for principle decades. In other words, the products and services they provide are not a meaningful driver of their customer’s cost structure but it’s very important that clean uniforms arrive on time as employees can’t be expected to work in soiled clothes. Having clean uniforms for employees is not something that management wants to deal with - they have far bigger things to worry about - they just want it to happen automatically.

CEO Kim Scott explained this relationship during the recent analyst day:

“So it's very attractive if their spend with us is less than 1% of their total spend, because we're just a blip on the radar, something they've got to have, but it's a very low spend with low attention and low impact to their organization, or there's a regulatory reason. So they have an obligation. They have to use the product or service. And we can provide that product or service.”

I can speak from experience here. In a previous life I was an engineer and supervisor at a vitamin manufacturing plant. We wore uniforms every day and the last thing I wanted to deal with was finding a new vendor to wash our uniforms. I had too many fires to fight on a daily basis to worry about if we were going to have clean uniforms for the weekend shift, and I certainly was not about to look for a new uniform launderer during our annual budgeting process.

This low price to value relationship and critical nature of the service manifests itself in very high customer retention. Basically, you really need to screw up to lose the business. Vestis enjoys about 90% annual customer retention.

Route Density and High Incremental Margins

The uniform business is all about route density, or how many stops frontline employees can make with the shortest amount of driving. Just like a garbage collection company, if you have a driver already driving down a street it takes very little incremental time and cost to collect garbage from 10 houses rather than 5. You’re already there after all (the costs are largely fixed) so tacking on a few more houses nearby is incredibly profitable.

Unlike garbage companies, Vestis has the added benefit of cross-selling ancillary services at very little incremental cost. Presently customers are only utilizing 30-40% of Vestis’ services, which provides tremendous upside if that ratio can improve even modestly.

For example, management walked through an example of a customer in California that only utilized the uniform services. The delivery driver was able to add two mats to the location which improved margins by 373 basis points. Again, the driver is already there and it takes very little incremental cost for them to drop off two mats in addition to the uniforms.

A company that can get route-based density and cross-selling right should be very profitable – Cintas is and demonstrates where Vestis is trying to head. Cintas enjoys around 20% operating margins and 30%+ return on equity (without the use of substantial leverage) while Vestis’ operating (adjusted for the new cost structure post-spin) are less than half of that at around 9%. Management sees a path to 400-600 bps improvement in margins over the next several years to narrow the gap with Cintas appreciably.

An indication of Vestis’ business quality is its ability to pass on inflation related cost increases. While the company does not have unlimited pricing power, they were able to offset virtually all of the last several years’ worth of inflation-related cost increases through higher prices. Even this level of pricing power is exceedingly rare and shouldn’t be taken for granted. Cintas confirmed this dynamic in its most recent 10K, noting that inflation has not had any discernible impact on its profitability.

It’s pretty evident that now that Vestis is not lost in a big conglomerate and is free to pursue more ambitious growth plans that a sizeable margin-expansion opportunity exists. The question is, how could the company get there and can the company execute?

Margin Expansion Opportunity

As discussed above, the easiest way to lift margins for a recurring revenue business is to just sell more stuff to existing customers. Since Kim Scott, the CEO, joined from Terminix (another route-based/recurring revenue business) in 2021, she has implemented a number of logical initiatives to improve customer penetration.

Shockingly, prior to Kim joining the frontline drivers were not instructed or incentivized to cross-sell customers. Instead, the company had a dedicated sales force to drive incremental revenue. The frontline workers are the ones with the direct exposure to the people that interact with Vestis’ service on a weekly basis, have a relationship with customers, and therefore are best positioned to try and tack on additional revenue through cross-selling ancillary products and services. It appears that the company has some momentum so far, with frontline employees generating 108% more sales activity than in 2021. Scott elaborated during the analyst day:

“Do we know that it's working? Yes, we do. So if you go back, and you look at all of our routes in FY '21, and you look at the sales activity, so routes that we sold something on and you compare it to all of our routes in FY '23 year-to-date and all of the routes that we sold something on, 108% increase in selling activity on routes. So our route teammates are fully engaged. They are selling, they are excited. We're having contest. We're celebrating. We have winners. If you're the top provider or a top performer, you get a gift at your house from me and my team saying thank you. There's so much energy around those. People are so excited and fired up about cross-selling the base.”

The next initiative to drive topline is to target new verticals. Here is where it makes sense to engage targeted sales resources to go out and hunt for new business. Management has defined the types of companies to target and they include opportunities that are:

at least $300M in potential revenue;

high (>$300/week) potential revenue per stop;

an opportunity for high penetration (3-5 products) and;

a high price to value (cost is <1% of spend or a regulatory requirement).

Automotive dealers were a recent focus that check all of these boxes and have been a successful addition to the customer base.

Vestis has a 24% penetration in auto dealers on the west coast and significant opportunity to replicate the playbook in other regions, all of which are 15% or less penetrated.

The last area of margin expansion management is targeting is basic operational excellence. Scott is enacting a series of blocking and tackling measures that other route-based models have successfully employed. These un-sexy productivity initiatives include realigning and consolidating certain logistics resources, implementing route-optimization techniques and customer flows, and improving merchandising in stockrooms to rationalize SKU counts and improve turnover.

The company discussed examples of how these initiatives work during the analyst day and walked through southern California and Orlando as two case studies. By eliminating overlapping routes or disconnected customers the company reduced distance by over 20%, revenue per mile increased by 25-30%, revenue per hour increased by 3-6%, and fuel was lowered appreciably. This playbook can be rolled out over the company’s regions and result in meaningful (1-2%) overall higher operating margins.

Management and Incentives

To quickly hit on management; Vestis has done a nice job bringing in executives that can drive the types of changes the company needs to close the gap with Cintas. Kim Scott was the COO at Terminix Global before coming to lead the spinoff as CEO of Vestis. Terminix is very much a route-based and recurring revenue business and the route optimization efforts she led there directly apply to the work going on at Vestis. She is big on culture and incentives and by all accounts appears to be energizing the entire organization.

Scott has tapped other executives she’s worked with in the past to help with the growth initiatives, and the board is particularly impressive. For starters, the chairman of the board is the former COO of Cintas. He knows what good looks like in this business and should prove valuable. Other board members include the former CEO and Chairman of Brinks, former CEO and Chairman of Advanced Disposal Services, and the former CFO of Waste Connections. These businesses are as route-based as it gets. Finally, the COO of Casey’s General Stores is on the board, which is another outstanding business with sound capital allocation.

Incentives look good as well. Vestis measures ROIC and incorporates it into managements annual incentives. Anytime I see those four letters in an annual report or proxy I can safely assume the company is more rational with capital allocation than most other public companies. The company also incorporates free cash flow generation into the executives comp plans, another (shockingly) rare occurrence in today’s world.

Overall, I like management and the incentive structure, but everything comes down to execution and how much optimism is reflected in the current stock price.

Forward Returns and Valuation

If management achieves their targets, in five years Vestis will be a larger and substantially more profitable business. Thanks to cross-selling, targeted high-value growth verticals, and productivity initiatives, management is committing to a 400-600 bps lift in margins on 5-7% annual revenue growth.

Historically, the business has grown around 2% annually, so these results would require a departure from the past. It does seem Vestis was neglected as a part of Aramark, and I have a reasonable degree of confidence management can deliver on these targets, especially given the specific initiatives management can point to and the early success they’re having in each. It’s not as is it’s never been done before; using the same techniques Cintas has compounded revenue at 8% for the past decade, and intrinsic value by a low double-digits amount, while enjoying significant multiple expansion which has resulted in tremendous shareholder value.

About 50% of EBITDA converts to free cash flow, so at the midpoint of management’s targets (6% revenue growth, 19% EBITDA margins) free cash flow would compound at a mid-teens rate over the next five years. This is a little misleading though, because the 50% conversion was true when under the umbrella of Aramark. Now that the company has substantial debt (more on that below), a fair bit of operating free cash flow will go to debt service.

A recent Barron’s article highlighted Vestis as having an attractive valuation due to typical spinoff dynamics. Often times when a large parent company spins off a smaller subsidiary, the SpinCo is subject to indiscriminate selling from shareholders “cleaning up” their portfolio when they receive a few shares of an unknown stock. Some forced selling appears to have taken place and the stock is down ~10% since it was spun off in September. Barron’s also highlighted a seemingly attractive relative valuation of ~16.5x earnings compared to Cintas at 35x and UniFirst at 23x. While both are true on the surface, the valuation is a little deceptive given the hefty debt load Aramark saddled upon Vestis post-spin.

As is customary in spinoffs, Vestis sent a $1.5B dividend to Aramark funded with two tranches of debt with 7.5% interest rates. Presently the business is 4x levered and will need to spend the next several years delivering to a more appropriate ~2-2.5x. Interest expenses will eat up around 50% of free cash flow for the foreseeable future, meaning the stock isn’t as cheap as the P/E implies.

Still, if management delivers 6% growth, 19% EBITDA margins, 50% FCF conversion (before interest costs), and dedicates most of free cash flow to pay down debt for the next few years, I can pencil in high-teens or low-20% annual returns assuming a 18-20x exit valuation; hardly demanding for a business of this quality. A valuation multiple closer to direct peers Cintas or UniFirst would mean appreciably higher returns still. If management fails to execute, and the business continues its historical low-single-digit growth pattern, the stock is probably dead money.

An investment in Vestis is largely a levered-equity bet on the ability for management to execute its plan. If they can continue to drive cross-selling, improve route densities, and complete operational excellence initiatives, margins will be structurally higher. Earnings, returns on capital, and ultimately the stock price would likely all track materially higher. If the company doesn’t execute, earnings and the stock will probably disappoint. That said, given the predictability and quality of the business it’s hard to foretell a disaster for investors at present prices, hinting at some asymmetry.

A few final thoughts; management indicated that, while not significant, capex can be a little lumpy at times. Also, I wouldn’t be surprised if the business stumbles periodically in its transformation process. Fingers crossed that if and when the business hits a hiccup in its margin expansion efforts it has a “Dollar General moment” and investors get a chance to buy the business at a double-digit normalized free cash flow yield. It may not seem likely, but I wouldn’t write it off. There’s a reason one of Matt and my favorite sayings is “sooner or later everything trades for 10x earnings”.

Do you have a “stranded” 401k from a past job that is neglected and unmanaged? These accounts are often an excellent fit for Eagle Point Capital’s long-term investment approach. Eagle Point manages separately manage accounts for retail investors. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

Another outstanding article as $VSTS along with its competition is competing against non-consumption which is similar to the datacenter industry 15 years ago. For one to “bet” on $VSTS, one will need to track & monitor route density along with margin improvement. Can $VSTS, as a spin-off, focus on its operations and become $CTAS or will this segment of the market resemble auto parts where there is a clear leader ($CTAS) along with several laggards ($CTAS $UNF). Time will tell but one thing that makes me less optimistic is that few $ARMK leaders went to the spin whereas Greenblatt states to watch where the parent CEO goes. To be repetitive, time will tell

It appears they’re measuring operating income margin (not ROIC) in management incentives per the chart?