Playing Offense With The Defense Industry

At first blush, defense contractors may not seem like good businesses. They sell complex products that use edge technology, often at deflating unit prices, to a single buyer that has rapidly changing needs and minimal budgetary visibility.

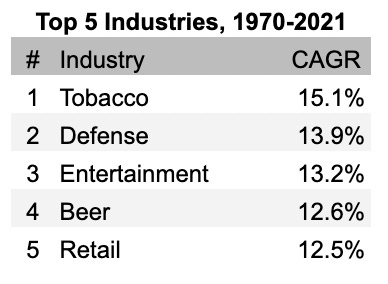

But if you think the defense contractors are bad businesses, you’d be wrong. Defense has been one of the best performing industries of the last fifty years. According to Prof. Ken French, the defense sector has produced 13.9% annual returns since 1970, lagging only tobacco.

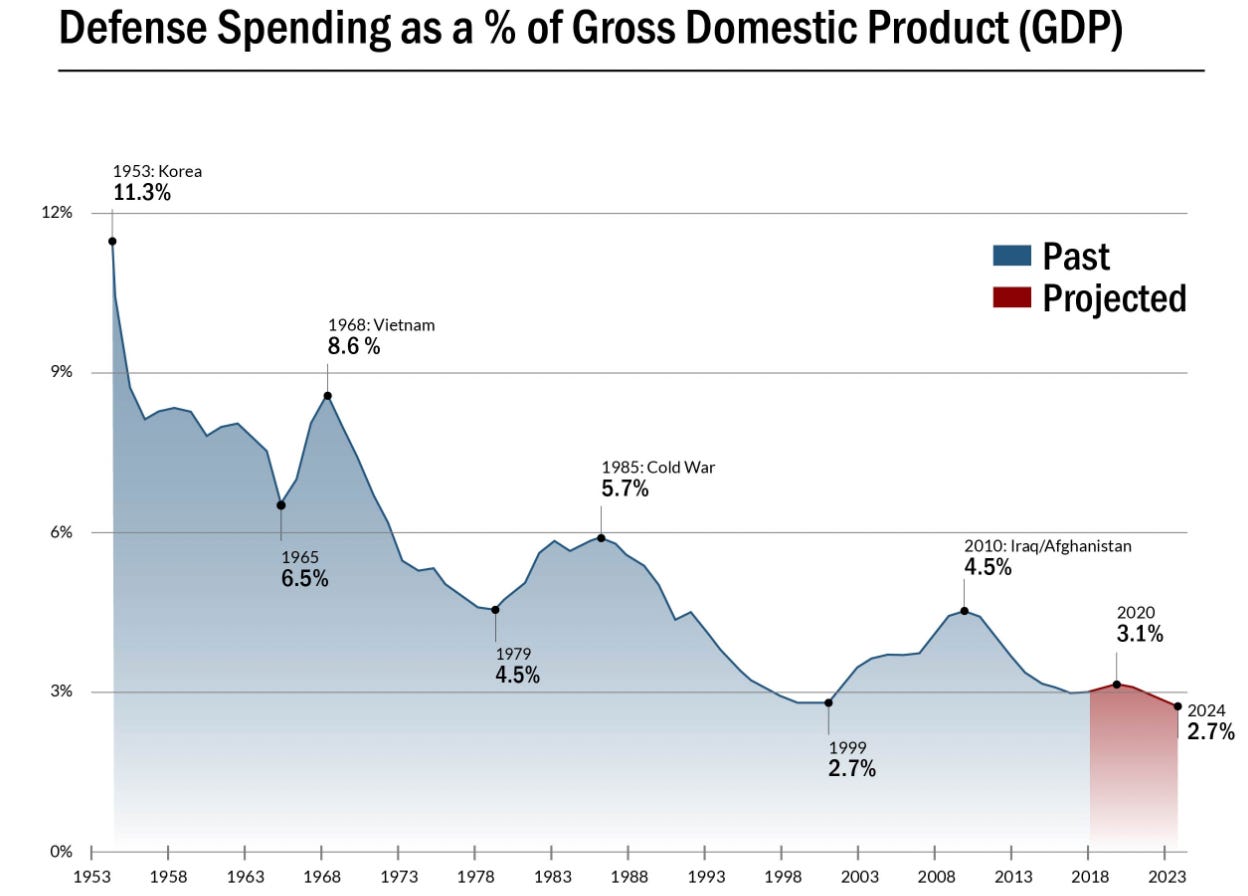

This is a remarkable result, especially considering the defense industry has been battling the headwind of a shrinkingUS defense budget (as a percent of GDP) since WW2 with only a few periods of relief. Today’s budget is tied for an all time low.

The end of the Cold War was particularly traumatic for the industry. The defense budget halved as a percent of GDP and fell over 30% in dollars, sparking a wave of rationalization and consolidation. But even that couldn’t slow defense stocks down. According to Prof. French, the defense industry has produced a positive total return (i.e. including dividends) in every rolling ten-year period since 1963.

Today I’ll take a look at some of the factors that have made the defense sector so lucrative for investors. I’ll discuss the industry in general more than companies in specific because I find the individual companies more complicated and difficult to analyze than the simpler businesses we usually discuss here. For one, many of the most important defense contracts are classified. They’re included in the company’s financial statements but not discussed.

Since you can't know the ins and outs of each contract, I think investors in the defense industry must focus how the industry's structure create durable competitive advantages for the incumbents.

A Rational Oligopoly

The best businesses are unregulated monopolies, but those are extremely rare. The second best (and much more common) are rational oligopolies. “Rational” means that the members of the oligopoly compete in a gentlemanly manner. They don’t slash prices in an attempt to steal market share. Price wars inevitably leave everyone worse off. Instead, rational oligopolies compete on quality of service while maintaining high returns on equity.

The defense industry has consolidated down to seven big global players over the last fifty years. Market share is stable — the top seven have been the same for the last fifteen years. They are: Lockheed Martin, Boeing, BAE Systems, Raytheon, Northrop Grumman, Airbus, and General Dynamics.

While seven players isn’t exactly what I’d call an oligopoly, usually just one or two of these companies can compete for any given contract. For example, Huntington Ingalls is the only company that can build aircraft carriers. And only Huntington Ingalls and General Dynamics can build nuclear powered submarines. Only Northrum Grumman can build the B-21 and inter-continental ballistic missiles. And on and on.

The Pentagon isn’t pleased with this, but has no one to blame but itself. The Wall Street Journal recently wrote:

The Pentagon has also streamlined military operations in ways that have left less room for multiple contractors. Lockheed Martin’s F-35 jet fighter, for instance, is meant to replace many other types of aircraft.

Similarly, there are only two big shipbuilders, General Dynamics Corp. and Huntington Ingalls Industries Inc. At most three companies typically submit bids for most big defense contracts.

“It’s pretty hard to have competition for something like an aircraft carrier when only one facility is able to build it,” said David Berteau, president of the Professional Services Council, a trade group, and a former Pentagon acquisition official.

The Pentagon’s pain is investor’s gain.

Teamwork

One unusual quality of the defense sector is that rival firms routinely work together on contracts. Often when two companies vie for a contract the winner becomes the prime contractor and the loser becomes a subcontractor. General Dynamics is the prime contractor on the Columbia-class submarine program but has subcontracted a significant portion of the work to Huntington Ingalls. Similarly, Lockheed is the prime on the F-35 but Northrup Grumman and virtually every other aerospace company has content on it.

It is most lucrative to own a program as a prime contractor, but still desirable to be a subcontractor. Rivals are less likely to try to win contracts at all costs since they know they’ll get a piece of the action if they loose. It’s a steady buffet rather than feast-or-famine.

Barriers To Entry

Market share is stable within the defense industry because of strong barriers to entry. The strongest barriers to entry are on programs that are A) the most technically advanced and B) extremely long-cycle contracts.

Fighter jets and nuclear-powered submarines are the best examples. Lockheed Martin has a contract to build and service the F-35 Lightning through 2070. General Dynamics has a contract to build and service the Columbia-class ballistic missile submarine through 2085.

Fighter jets and nuclear-powered submarines are improved incrementally, just like any other product. The technology is so specialized, so advanced, and so mission-critical that it is difficult to skip a generation of development. Without having built the F-16 and F-22, it’s doubtful Lockheed could build the F-35. In fact, the F-35 Lightning’s name is an ode Lockheed’s first fighter, the P-38 Lightning, the workhorse of WW2. These two airplanes look nothing alike, but are linked by continuous chain of incremental improvement spanning seven decades. While there are no guarantees, Lockheed is in a good position to win the contracts to build the F-22 and F-35’s successors. And if Lockheed isn’t the prime, they’ll be a major suncontractor.

Barriers to entry only appear to increasing as defense technology continues to get more complex and specialized. Today’s incumbents are likely to become further entrenched.

For example, the contract for a new land-based intercontinental ballistic missile (ICBM) initially received interest from both Northrop Grumman and Boeing. However, after Northrop closed its acquisition of Orbital ATK, Boeing dropped out of the bidding. In acquiring Orbital ATK, Northrop had gained a monopoly on the American-made solid state rocket engines which power ICBMs (intercontinental ballistic missiles). It wasn’t economic for Boeing to design its own solid state rocket engines, and Boeing didn’t want to risk winning the contract and getting squeezed on price by Northrop. Product complexity and rational competition dictated that only one company had the know-how to deliver.

Classified programs pose another barrier to entry. These programs aren’t advertised or put out for public bid. Only the incumbents know about them. Likewise, a skilled labor force with the requisite security clearances gives incumbents a serious advantage.

Contract Structure

The DOD wants the defense industry to earn healthy, but not extravagant, profits. America’s national security depends on the defense contractors’ industrial capacity, so the DOD has an incentive to ensure that the defense industry is resilient and well capitalized.

One way the DOD achieves this is through its contract structure. Typically, initial contracts are put out for a competitive bid. The winner will often receive a cost-plus contract which shifts the financial burden of R&D and cost overruns to the DOD. As programs age, they tend to move toward fixed-price contracts.

Fixed price contracts are riskier for defense contractors, but also more lucrative. The DOD only moves mature programs where manufacturing costs are well known to fixed price contracts. In return, the DOD will often flex its bargaining power and extract deflationary unit costs from the contractor. Contractors must continually reduce manufacturing costs to maintain their margins. The DOD wants the contractors to succeed, so price deflation is realistic. Contractors are usually able to remove enough cost to offset the DOD’s deflationary pricing and then some so margins typically rise when firms transition to fixed-price contracts. As programs mature, margins typically expand and the products become cash cows. Many programs last for decades.

Change orders are another margin opportunity. The DOD often issues change orders for work outside of the original contract. Contractors can request additional payment for fulfilling them, often at attractive margins. Even when the DOD is dissatisfied with a product, they often find it is easier to work with the existing contractor on a redesign rather than award the contract to someone else.

The defense industry has been lobbying Congress for years to give the DOD more latitude to make multi-year spending commitments. Recently, they succeeded. The New York Times recently reported that, “Congress this year has moved to allow the Defense Department to more broadly make multi year spending commitments for certain weapons systems and shipbuilding operations.”

This arrangement is good for the DOD, who will be able more readily increase production capacity. It’s good for defense contractors, who get clear demand visibility. And it is good for shareholders, because it de-risks investments. Few industries have such a high degree of demand visibility before they invest in productive capacity.

Do Defense Companies Have A Place In A Portfolio?

The war in Ukraine seems to have jolted world leaders from their sleep. Everyone, from Sweden and Germany to Japan, are increasing their defense budgets to ensure they can respond to unprovoked aggression.

This ought to be a boon for the American military-industrial complex in the years ahead. Raytheon’s CEO recently told the New York Times, “We went through six years of Stingers in 10 months, so it will take us multiple years to restock and replenish.” However, making specific predictions is tough. Defense programs operate on long lead times so the effect of the war in Ukraine has yet to really be felt.

The biggest prime contractors currently trade toward the upper end of their historical valuation range, which makes sense. A global re-arming is a simple and pervasive narrative. However, investors rarely get paid well for following the obvious consensus narrative.

The time to buy defense companies with a margin of safety is when no one wants them. That was a few years ago. The good news is that while defense companies are relatively expensive relative to history, they are nowhere near nosebleed valuations. Investors buying here will probably do fine and perhaps spectacularly if current trends continue and intensify.

Besides being wonderful businesses, defense stocks are attractive because they don’t follow the general business cycle. The defense industry is cyclical with respect to the DOD’s budget, which is somewhat idiosyncratic. This means that defense companies offer a unique way to diversify a portfolio. US defense spending is near record lows relative to GDP. Mean reversion would offer a nice tailwind to the industry.

I would personally never buy a stock purely for diversification. Every one of EPC’s investments needs to stand on its own merit, which means that they have to be good business that we understand and sell at an attractive valuation. If, on top of that, I can diversify the (likely) cyclicality of my investment’s earnings, so much the better.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. You can also find more information on our website. We recommend starting with our Fundamentals. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

Thanks Matt 💚 🥃

Regarding the upcoming debt ceiling discussion, how do you view the possibility that defence spending is cut and thus, defence earnings might shrink?