Odds & Ends: May 2024

Thoughts on post-earnings sell-offs at Starbucks and Vestis along with some thoughts on the Berkshire AGM

Every so often we come across a handful of ideas that may not warrant a full blown deep dive, so instead we group them together in an “odds & ends” post. A few things that caught our eye over the last couple of weeks are the Starbucks post-earnings drawdown, a collapse in the share price of Vestis, and some reactions from the Berkshire annual meeting.

Do you have a “stranded” 401k from a past job that is neglected and unmanaged? These accounts are often an excellent fit for Eagle Point Capital’s long-term investment approach. Eagle Point manages separately manage accounts for retail investors. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Starbucks

Starbucks is an easy business to understand and a brand that almost everyone is familiar with. We love strong consumer brands that earn high returns on capital and are squarely in replication mode. On the surface, Starbucks appears to fit the bill.

The stock is in the midst of a sizeable drawdown and after falling 15% the day after the most recent earnings report, the stock is more than 40% below its 2021 high. Is Starbucks a fallen angel destined to return to glory or is the business facing potentially more long-term headwinds?

Fundamentals

Like many of the businesses we study and follow, Starbucks’ business is driven by the unit economics of its store base. Revenue from company-operated stores represents 81% of the company’s revenue with the remaining coming from licensed stores (13%) and “Other” (6%; mostly consisting of CPG items sold in stores and through other channels).

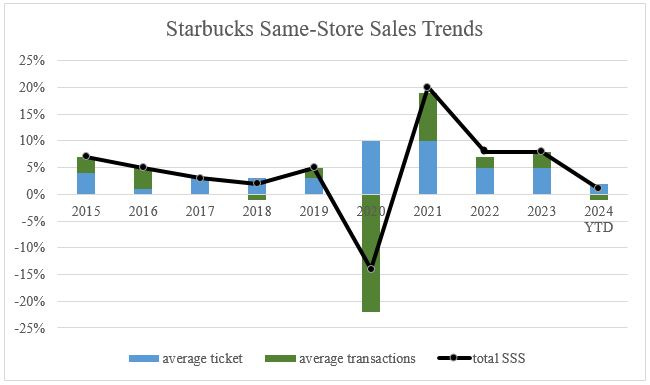

The business is driven by same-store sales, new units, and operating margins. Outside of 2020, for years the company has reliably grown both ticket size (pricing) and transactions (volumes).

Over the last decade same-store sales have grown at an average of 5% per year, and total stores have increased at ~6.5% annually. The result has been durable double-digit revenue growth and solid value creation for shareholders.

Historically, Starbucks has earned outstanding returns on capital. Pretax returns on capital were over 75% last year and the company has no equity employed in the business (i.e. all equity has been pulled out of the business and more than 100% of total capital is debt).

However, incremental returns on retained capital are, at least recently, less impressive. Over the last ten years the company has retained about 35% of cash and reinvested it at ~20% incremental returns. This is still very solid and better than most businesses, but a bit lower than I was expecting given the historically strong returns on capital. This has resulted in ~7% compounding in intrinsic value. Per share intrinsic value has compounded at closer to 10%+ thanks to a solid repurchase program.

The reason intrinsic value has compounded a hair below revenue growth is due to modest margin compression. Operating margins and operating cash flow margins have both come down a few percentage points since the mid-2010’s, suggesting a potentially deteriorating competitive position.

Competitive Position

Starbucks undoubtedly has a strong global brand. The brand strength is evidenced by the companies pricing power which, outside of 2020, has never resulted in average ticket size decreasing. It doesn’t take much more research than visiting virtually any Starbucks during the morning hours to gather that they are ingrained in many people’s daily commute to work or school.

The company’s focus on operating its own stores has given them a level of control not always present at franchised brands. Founder Howard Schultz installed a deeply rooted customer-centric ethos within the business from the start.

In recent years, the Starbucks app has been a significant growth driver. Over 32 million people are active rewards members and the pre-loaded cards/app acts as an interest-free bank within Starbucks. Programs like this generally lead to sticky customer relationships and are tremendous long-term value drivers.

Overall, Starbucks has an enviable brand, solid economics, and a seemingly long growth runway. However, recent results call some of these points that were formerly taken for granted into question.

Current Challenges

Despite a historically strong competitive position, Starbucks is running into growth challenges both at home and abroad. Same-store sales growth abruptly reversed and in the most recent quarter was -3% in the U.S. and, jarringly, -11% in China. The latter is particularly startling given the dependence on China to drive future unit growth.

Competition is fierce in China with QSRs and standalone coffee shops aggressively competing on price to take market share. After all, coffee consumption in China is 13 cups per capita vs. 280 cups per capita in Japan and 380 cups per capita in the U.S. The opportunity appears massive which attracts stiff competition. So far, in an effort to maintain their premium brand status, Starbucks has refused to compete on price. It’s not working particularly well yet, but there is a long ways to go before the story is written in China.

Additionally, late in 2023 the company guided for operating margins to continually expand. After the most recent results management now expects margins to remain flat. All full year financial targets have been ratcheted down.

To muddy the waters further, founder Howard Schultz (who has already come out of retirement to rescue the company’s growth prospects twice) wrote a public memo on LinkedIn calling on the company to refocus on the customer and in-store experience. I can’t imagine this makes the current CEO – an outsider from Pepsi recently brought in by Schultz– feel warm and fuzzy.

The fact that Schultz has had to return twice raises questions about the business. Buffett has famously said he wants businesses so good that ham sandwiches could run them. Schultz is far from a ham sandwich and him returning to save the day multiple times suggests maybe the brand is less impenetrable than it appears.

All of this resulted in Starbucks’ stock dropping 15% on the day of the earnings release. It’s down 30%+ over the last year and is 50%+ behind the S&P over that span. Over the last five years the stock is roughly flat. By no means does one year mean much in the long run, nonetheless it’s been a tough stretch.

The question that will determine forward returns is; are the current challenges temporary or signs of a narrowing moat and deteriorating competitive position? Equally importantly, how much margin of safety is built into the current stock price to protect against potential continued challenges?

At 20x forward earnings, the stock trades at a significant discount to its historical median of 29x. Relative valuations mean little to us, though, as absolute valuations are what count. That said, I’m far from certain there’s a margin of safety at present prices.

If growth reverts to historical trends in the U.S. and China, the company experiences operating margin expansion (as originally intended), and capital continues to come back to shareholders, today’s prices are likely to look like a bargain. We love “fallen angel” investments that often rhyme with what’s happening at Starbucks. However, if growth continues to stall and margins remain under pressure, investors could be looking at substantial additional downside, at least temporarily, in the future. Time will tell and it’ll be interesting to study and follow!

Vestis

Vestis is another interesting business that encountered a post-earnings call disaster. We’ve followed Vestis since the spinoff from Aramark and for a more detailed overview take a look at our original post.

Fast forward to last week and the company released Q1 results that resulted in a 45% sell-off in the stock in one day. While the stock has already bounced back ~15% it’s still down 45% this year and trading at a single-digit traililng earnings multiple.

A 45% single day decline is rare for any stock let alone one with as stable of an underlying business as Vestis, and I think there are some instructive takeaways.

As a quick refresher Vestis is basically a uniform launderer and the second largest player in the fragmented industry behind Cintas. It’s business and industry are characterized by unspectacular but steady growth, predictable and recurring revenues, a route density-based moat, and lots of free cash flow.

Just a quarter ago Vestis projected solid 4-4.5% revenue growth and 14%+ EBITDA margins for 2024. This was in the ballpark of what the company communicated around the time of the spin-off. Jump forward three months and management now expects revenue to be down 1% to flat for the year and EBITDA margins of 12-12.4%. These results are not disastrous (it’s not like the company is losing money or rapidly shrinking, and free cash flow is up dramatically), but the market threw a fit.

At 17x earnings as recently as early May, it’s not as if the stock traded at a demanding multiple coming into the earnings report. So why the panic? Two things stick out to me that likely contributed to an extreme reaction; expectations and leverage.

In the public markets, companies that consistently under-promise and over-deliver are rewarded by shareholders. Businesses with a track record of executing and delivering on their operational commitments are afforded leeway (to a degree) when they run in to inevitable hiccups.

When the company spun off from Aramark in 2023, management committed to steady revenue growth, continued margin expansion, and touted the stickiness of their customer relationships. Unfortunately, just two quarters into being a standalone public company, Vestis reported uncharacteristic customer churn which they have been slower to replace than anticipated. This resulted in moderated pricing (in an effort to not lose more customers) which in turn results in lower revenue growth and margin contraction.

I doubt any of the qualities management touted are seriously impaired, and with 93% retention YTD and 0.9% revenue growth, the company is not hemorrhaging customers. It appears there was outsized churn at the end of 2023 around the time of the spin off. I could be wrong, but it seems unlikely this will persist.

A temporary energy fee rolled off last quarter as well, distorting prior years’ margins and providing a tougher comparison. After accounting for this, it certainly doesn’t appear margins are structurally impaired. But, it also doesn’t mean they’ll expand to the 18% that management is targeting by 2028.

Still, not a good look for a newly public company. Vestis has now broken trust with the public markets and it may take some time to be restored.

The second takeaway is simple; the sell-off in Vestis’ stock is a reminder of how dramatically equity prices can respond to even small changes in the underlying business when there are high levels of leverage at the business. It reminds me of some of the cable companies (Charter, Altice, etc.) as well as Davita in recent years. All of these companies’ underlying business trends move in basis points and are very predictable and stable year-to-year. But, because they have significant levels of debt, there can be wild swings in stock prices with small changes in the business. This provides both risk and opportunity.

It’s just another reinforcer that it pays to be patient, and let valuations come to you. In our original write-up, I wrote:

I wouldn’t be surprised if the business stumbles periodically in its transformation process. Fingers crossed that if and when the business hits a hiccup in its margin expansion efforts it has a “Dollar General moment” and investors get a chance to buy the business at a double-digit normalized free cash flow yield. It may not seem likely, but I wouldn’t write it off. There’s a reason one of Matt and my favorite sayings is “sooner or later everything trades for 10x earnings”.

Well, that stumbling came sooner than expected and the business trades for a double-digit trailing free cash flow yield (the key is; what is normalized free cash flow). The leverage still makes me uncomfortable, but a lot less so than when the stock was twice as expensive.

One final thought; this is just another example of a business running into a no-growth quarter or two and the market, perhaps blindly, de-rating the stock to a no-growth terminal multiple. It may prove correct; perhaps Vestis has a vastly inferior competitive position compared to Cintas and growth will never materialize. Or, perhaps, this is another wild overreaction from an impatient and manic depressive stock market.

Thoughts on the Berkshire AGM

Thanks to everyone that we got together with in Omaha last weekend; it was a blast as always and we hope to see you all again next year. There are many great summaries of the meeting, so I’ll be brief.

Buffett Selling down Apple

The biggest news seemed to be Buffett selling 13% of his largest (by far) stock position. Everyone wants to know what this means regarding Buffett’s view of Apple’s stock. Of course, he will never give his direct thoughts on any of the public securities he owns, but his actions speak pretty loudly. Buffett has virtually never trimmed his large holdings, he’s either a buyer or a seller.

Apple is growing very slowly, running into problems with demand in China, and has not come out with any transformational products in years. It’s an exceptional business, but it’s also a different business selling for a different valuation than when Buffett purchased it. At 27x earnings and with modest growth prospects, beginning to sell down his position seems pretty logical to me. Now that I’ve put that in writing the stock will probably double this year. Either way, it’s interesting to watch play out.

Berkshire’s Cash Pile

At every meeting there are questions about why Berkshire’s cash pile is so large. Every meeting it’s the same answer; if Buffett found a better use for the cash (in size) that he thought was virtually certain to not lose money, he would deploy the capital at scale.

Buffett mentioned he expects Berkshire’s cash pile to be ~$200B at the end of this quarter. What I find fascinating is the amount of interest Berkshire is earning on its cash pile. Let’s assume the $200B will earn around 5% over the next year (invested in U.S. Treasuries). That will generate around $10B of interest income for Berkshire. Think about that. How many companies even earn $10B per year, let alone on their excess cash?

A little Googling tells me that there are only 120 companies in the world that earn more than $10B (this is not exactly apples to apples as the list I found is post-tax, but whatever). To illuminate the point, McDonalds earned around $8.5B last year. So, Berkshire has a McDonald’s sized business held just within its interest income. What a beast.

Charlie Munger Tribute

Each year Berkshire kicks off the meeting with a 30 minute movie. Usually the company is very strict about a “no phones” policy during the movie and it is never made public. This year was different, and Berkshire released the full shareholder’s movie to the public. It is a tribute to Charlie Munger, and I highly recommend everyone watch it.

It was bizarre and sad to not have Munger on stage with Buffett, but his legacy will live on forever.

Thanks for reading.

Do you have a “stranded” 401k from a past job that is neglected and unmanaged? These accounts are often an excellent fit for Eagle Point Capital’s long-term investment approach. Eagle Point manages separately manage accounts for retail investors. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

Excellent remark on Starbucks without Schultz: it's possible that when you replace Schultz (who has the EQ/inspiration to keep the baristas motivated) with KPI-focused corporate types (who tend to treat employees like numbers), the customer experience and ROIIC won't be the same, and neither will the valuation.