Murphy USA: A Low Cost, High Volume Retailer

Murphy USA: A Low Cost, High Volume Retailer

Murphy USA sells a lot of gasoline and a lot of cigarettes and buys back a lot of stock. This has worked well. Since its 2013 spinoff, Murphy's stock is up 673%, a 28.5% CAGR. EPS grew 21.5% per year, driven by 12.5% earnings growth and a 7.6% buyback CAGR.

Low costs and low prices are the keys to Murphy's success. These have been core values since day one.

Murphy opened its first store in 1997. Walmart wanted to sell fuel and tobacco at Super Centers but it didn't want to do it itself. So, they cut deals with Murphy Oil (Murphy USA's predecessor), Tesoro, and Sunoco. Murphy got the Southeast and later the Midwest.

The deals were simple. Walmart sold Murphy land on Super Center parking lots free and clear. There was no royalty, no lease, nor a cents per gallon payment of any kind. To this day Murphy owns 77% of its real estate (90% ex-QuickChek).

Murphy has a symbiotic relationship with Walmart because they drive traffic to each other. Super Centers attract a lot of value-conscious traffic, making them ideal locations for Murphy. Like Walmart, Murphy offers everyday low prices and targets blue-collar, value-conscious, semi-rural customers. Murphy aims to offer lower fuel prices than anyone except Costco. Costco targets a different demographic, so this isn't a big deal.

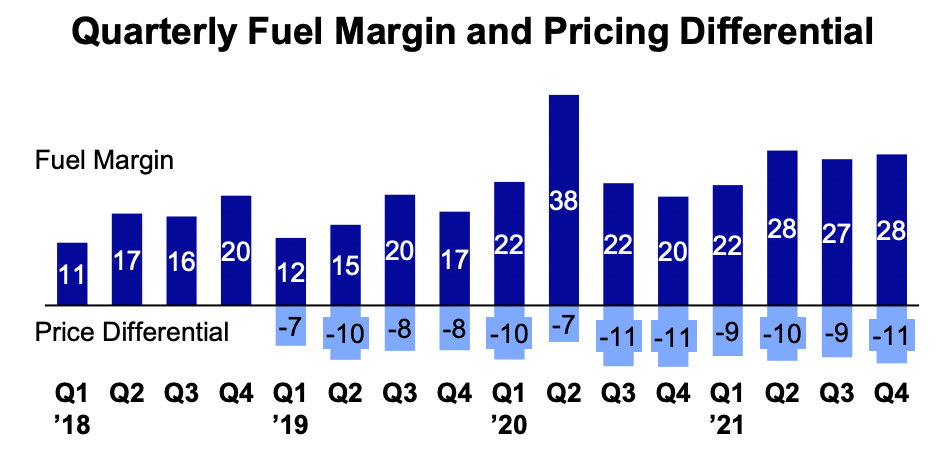

Murphy sells 3-4x more fuel than its competitors at slightly lower margins (e.g. 28c vs 39c per gallon in 2021 Q4). Co-locating low-cost fuel with Super Centers offers a win-win for Walmart and Murphy. Walmart gets more traffic and Murphy earns a high return on its investment.

Murphy can offer the lowest fuel prices because it has the lowest costs. Murphy's original stores were 150-208 square foot kiosks (pictured below). Kiosks had low up-front costs and required minimal maintenance. According to eMarketer, Murphy had higher sales per square foot than any retailer but Apple in 2014.

Between 1999 and 2005 Murphy built over 100 kiosks a year. But as Walmart's growth slowed, so did Murphy's. Around 2007 Murphy created Murphy Express and built them no more than a mile down the road from Super Centers.

In 2015 a new leadership team at Walmart decided they wanted to own and operate gas stations and would not sell Murphy any more land. Existing Murphy stores were unaffected, and the Walmart relationship remained strong.

In response, Murphy revealed its independent growth plan in January 2016. This marked a seminal moment in this company's history. The plan was to use half of its cash flow to grow and half to buy back stock. They continue to hold true to that today.

Murphy aimed to build 30-50 new Murphy Express stores and complete 20 raze-and-rebuilds per year. They'd cherry pick the best locations for the new builds near Super Centers or similar stores like Home Depot and Lowes.

From 2016 through 2020 Murphy built 168 stores, 34 per year. Murphy has struggled to find good store locations since QSRs (quick-serve restaurants) are often willing to pay more. More recently they’ve begun in-filling their best markets. They're building stores further from Super Centers but in areas where they are well known. The highest ROIC growth opportunities are behind Murphy but the current opportunity set still looks decent.

The raze-and-rebuild program replaced kiosks with 1,200-2,800 sqft stores. The new store format sells twice as much high-margin, non-tobacco merchandise as kiosks. Convenience stores average 7,000 sqft, so these are still tiny by comparison. Murphy’s small footprint makes them cheaper to build (they require 1 acre vs 2 for QuikTrip), cheaper to maintain, and easier to staff (1-2 people).

Replacing kiosks with stores has helped to diversify Murphy away from tobacco and lower their fuel breakeven cost.

Tobacco is a great business for Murphy and one they continue to "major in" because it drives habitual traffic. As retailers like Walgreens and CVS step back from tobacco, Murphy leans in. By its own estimates Murphy is the 2nd or 3rd largest tobacco retailer in the country.

Murphy applies the same high-volume, low-margin strategy to tobacco as they do fuel. Murphy sells 4x more tobacco per store than competitors. Cartons represent 50-60% of tobacco sales.

Murphy’s high volumes and technical prowess (they own their own point of sale system) makes them ideal partners for tobacco companies trying to learn about their customers, promote new products, and make digital connections. Tobacco companies often offer special promotions through Murphy since Murphy can handle the IT logistics and send back data. Vendor promotions lower’s Murphy’s tobacco prices which drives yet more volume and loyalty.

In 2013 80% of merchandise was tobacco versus less than 70% today. Murphy hasn't lost tobacco market share, they just sell a lot more non-tobacco merchandise now.

Tobacco has two downsides. First, cigarette volumes are in structural decline. Second, tobacco has lower margins than other merchandise (e.g. candy, salty snacks, lottery, beverage). The structural decline in cigarette volumes hasn't affected Murphy yet, and may never. Cigarette companies have been able to raise prices faster than volumes decline, which benefits Murphy.

Murphy also benefits from the growth of reduced-risk products like vapes and oral nicotine pouches. Selling cigarettes and RRPs is like selling picks and shovels to gold miners — Murphy doesn’t care which brands win or lose so long as people keep consuming nicotine. Humans have been using tobacco since 10,000 BC, so the Lindy Effect suggests Murphy is well positioned.

Murphy’s real goal in growing its non-tobacco merchandise business was to reduce its fuel breakeven costs. The company defines its fuel breakeven costs as: merchandise gross profit less all site operating costs, less all overhead costs divided by our retail gallons. The fuel breakeven measures the profit, in cents per gallon, Murphy must earn to breakeven after all costs and merchandise profits. There are three ways to improve the fuel breakeven: more merchandise profits, lower overhead costs, or more gallons sold.

In 2013, Murphy’s fuel breakeven was 3.5 cents. Today it is zero. Murphy's merchandise sales cover its overhead — they don’t need to sell fuel to make money. This is a huge advantage and one that separates Murphy’s from its competition.

Gas prices are set by the local marginal seller. These tend to be single-site operators or small chains with high fuel breakevens. Their high costs and high retail prices create a pricing umbrella for Murphy to operate under. Murphy can better the marginal seller’s price by a few pennies, attract volume with its relative value, and still earn healthy fuel margins.

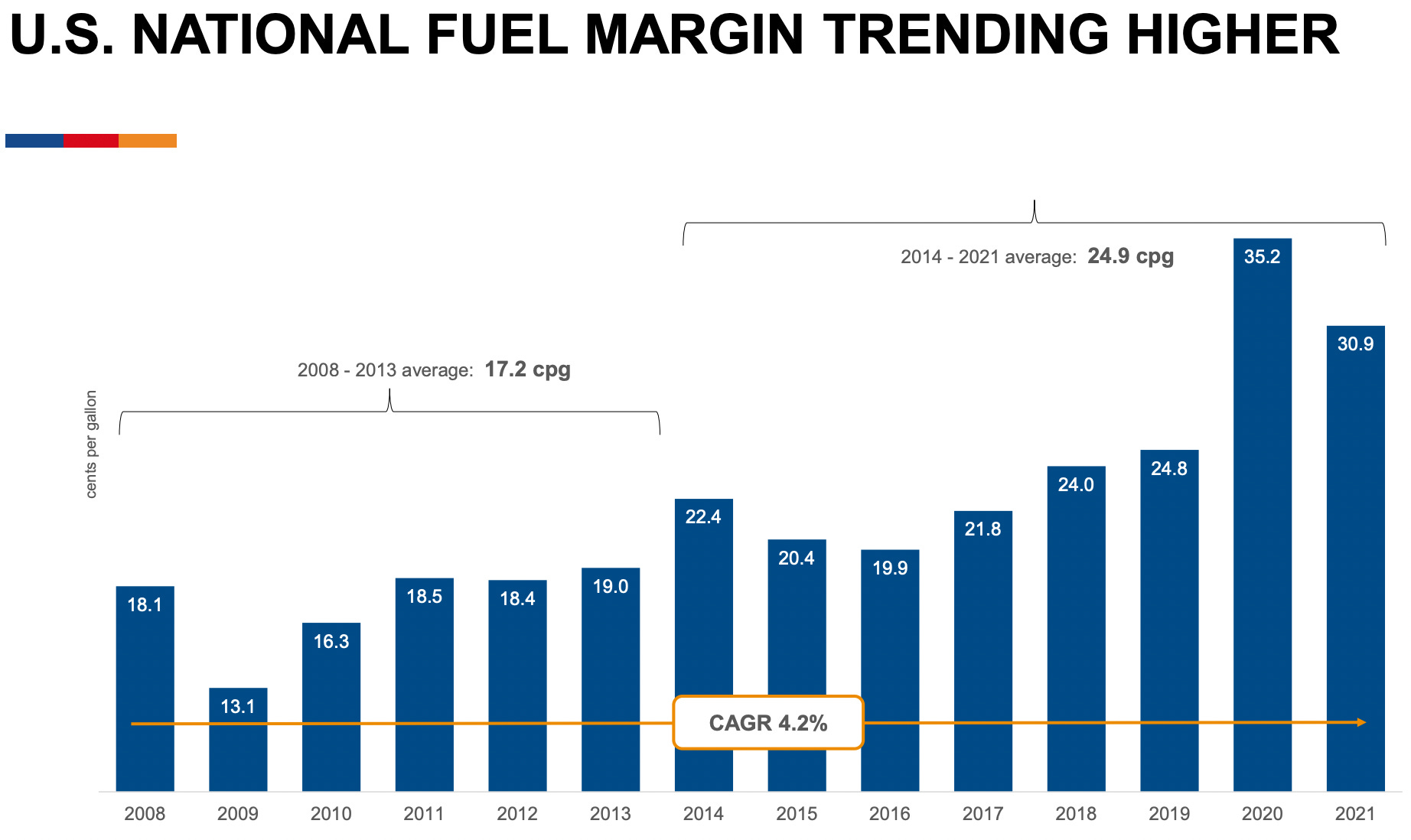

Before the pandemic, Murphy’s fuel margins were steady around 16c per gallon 2017-2019. Then the pandemic hit and its fuel margins skyrocketed to 25c in 2020 and 26c in 2021. Across the industry, margins moved higher.

Here’s what happened. The average gas station's fuel volume halved during the pandemic. Meanwhile, their costs increased. Utilities and labor cost more than ever now. These gas stations had no choice but to double their fuel margin to make ends meet.

Murphy’s fuel volume only decreased 12% during the pandemic. Super Center traffic didn’t decline much because people still needed to buy groceries and sought value and one-stop shopping. As gas prices rose, people became more price sensitive and favored Murphy’s everyday low price strategy.

The marginal gasoline seller’s high costs and high prices provided Murphy’s an umbrella under which they could provide lower relative prices and still earn higher margins. The company thinks higher fuel margins are here to stay because higher wages and utilities are here to stay. That said, fuel margins are unlikely to continue rising as rapidly since inflation is likely to moderate.

Although gas prices are the only price plastered on billboards everywhere you drive, their inherent volatility masks the industry’s margin expansion. When gas prices swing $0.50 or so, consumers don’t notice that Murphy’s is earnings 5c more per gallon. I’m not sure I’d call it pricing power, but Murphy’s does have an advantage over most retailers here.

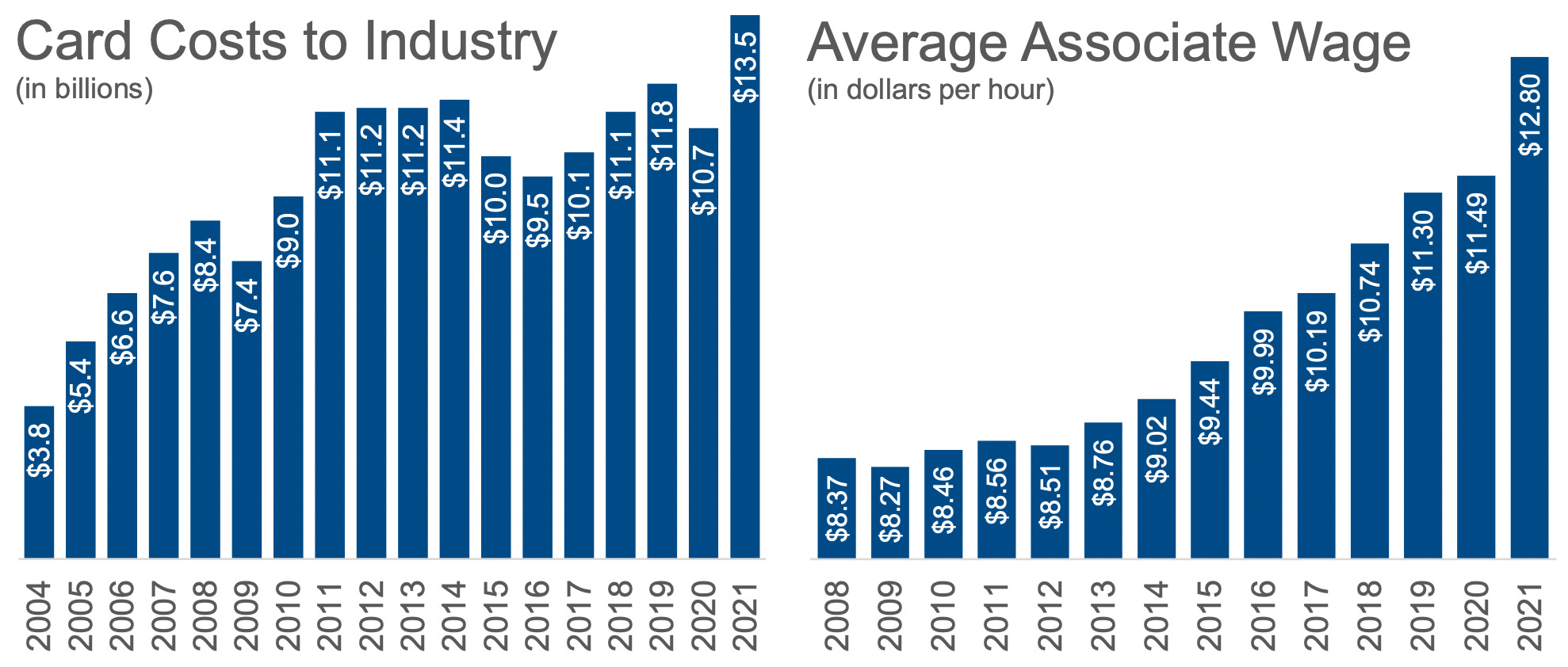

Where Murphy and the industry has a disadvantage versus other retailers is credit card fees. Credit card fees are calculated as a percentage of the final sale, but the industry manages its profits in cents per gallon, not a percentage per gallon. When gas prices rise, Murphy’s margin doesn’t necessarily expand but its credit card fees increase.

Murphy’s high volume, low overhead model has helped them weather the inflationary environment. The company thinks that in a worst case scenario wage inflation will cost it 1-2c per gallon but will cost its lower volume competitors closer to 7-11c per gallon.

Today single-store operators own 60% of US gas stations. The market remains extremely fragmented which means Murphy US will enjoy its relative cost advantage for a long time.

To understand the depth of Murphy’s low-cost advantage, it's worth stepping into the weeds a bit to understand how they buy fuel.

50% of Murphy’s fuel is proprietary — Murphy buys the fuel directly from refineries, ships it, and blends it itself. Murphy is one of the largest shippers on the Colonial pipeline and gets preferential treatment when the pipeline is at capacity (it usually is).

Murphy sources 40% of its fuel via 3rd party contracts with terminals. Prices are indexed to the spot rate. Murphy’s high volumes and strong credit give it bargaining power to gain preferential terms.

Murphy buys the final 10% of its volumes at the rack — i.e. from the local terminal at the spot rate.

Murphy loves price volatility because it can mix and match these procurement channels to find relative value. Murphy’s single-store competitors are limited to buying at the rack and are at the mercy of the market. Murphy’s high volume stores mean it rarely has significant inventory in its tanks subject to price risk. While crude oil prices do affect Murphy, they tend to affect Murphy less than its competitors.

The company gave two examples of its procurement prowess at its 2015 investor day.

Usually the price differential between New York Harbor and Houston is less than the cost to ship gasoline between the two. Sometimes supplies in New York get tight and prices rise. Imagine that the price of gas in New York might be $2.00 versus $1.80 in Houston. It costs $0.05 to ship between the two cities on the Colonial Pipeline so the arbitrage is open.

At these prices, traders will ship gasoline all the way from Houston to New York. Terminals along the way, in places like Atlanta, will need to pay more than $2.00 to attract product.

Murphy can buy gasoline in Houston at $1.80 and ship it to Atlanta for $0.03, for an all-in cost of $1.83. Other Atlanta gas stations will be paying over $2.00, so Murphy will have a $0.17+ cost advantage. Murphy will price its gas to be the cheapest by a few pennies and take the rest of the margin itself.

Another example is Murphy’s El Dorado, Arkansas location. Most gas stations in El Dorado buy from the local refinery and pay $0.01 to truck it to their store. Another option is to buy gasoline from a refinery in Oklahoma, ship it to Ft. Smith on Magellen’s pipeline, and pay $0.12 to truck it to the store. Since the Oklahoma pipelines receive low-cost crude oil from the Gulf Coast and Bakken, it’s often cheaper for Murphy to buy in Oklahoma and ship it versus buying it in Arkansas. The single-store operators in El Dorado can’t access the pipeline and don’t have the opportunity to match Murphy’s low costs.

These examples show how Murphy’s scale and low costs give it a leg up in procurement. Murphy passes enough of these benefits on to the customer via lower prices — enough to be the lowest (besides Costco) — and takes the rest for itself.

In this regard, Murphy is somewhat antifragile — it benefits from disorderly markets. Murphy’s cost advantage allows it to face tough environments from a position of relative strength.

EVs are one threat facing all fuel retailers. Murphy’s demographics will insulate it for a while, but it will eventually have to adapt to an electrified world. In September 2021 Murphy’s CEO stated:

Our mission is to provide low-cost motor fuel for mobility for Americans. And whether that motor fuel is a hydrocarbon or an electron, we're going to be there. But our customers are going to get served through our current offer for a long time.

Murphy has EV chargers at 8 locations (QuickCheks). However, Murphy’s customer demographics don’t support building more yet. EVs are luxury cars and there are not a lot of BMWs and Mercedes at Murphy's. Murphy’s customers skew blue collar, value conscious, and rural. Murphy’s approaches electrification on a site-by-site basis, just like they approach gasoline procurement and pricing.

For example, one of Murphy’s charging stations is in Kingston, New York. The site is halfway between New York City and Albany and there’s nothing else nearby. So, the location has the utilization to make sense. Tesla actually built, owns, and operates the chargers. Murphy gets crossover sales when people inevitably walk inside for a snack.

The Kingston, NY location is unusual. Murphy’s El Dorodo, AR location is more typical. It’s a 1,400 sqft store two hours south of Little Rock on I-20 with little competition nearby. Murphy considered building EV chargers and determined they’d need 800 EVs driving by the store a month or about 300 EVs in El Dorado to justify one. However, there are only 2 EVs registered in El Dorado and only 1,440 registered in the state. EV penetration needs to improve a lot before they will affect Murphy.

Still, Murphy is preparing. In January 2021 they bought QuickChek. QuickChek is a sandwich and coffee shop located in New York and New Jersey. They offer fuel at many of their stores and actually sell more gallons per store than Murphy, an exceedingly rare feat.

Murphy bought QuickChek to acquire fresh food know-how. It’s unclear exactly how Murphy plans to add food to its tiny stores. One risk is that Murphy slowly abandons its low overhead model in search of higher QSR-like margins. While QSRs has enviable margins, they also use more capital.

The acquisition makes sense from a long-term strategic positioning though. When people charge EVs away from the home, it takes at least 30 minutes. Such a long duration virtually ensures drivers will go inside and buy something. The quality of a store’s food may sway where the driver charges, so a high quality offering is mandatory.

Murphy doesn’t expect to do any more M&A. The only deals they see are low volume fixer-uppers, and that’s not Murphy’s game. QuickChek was a particularly good fit for Murphy because it didn’t dilute the company’s high gallons per store.

Looking ahead, and assuming there’s no impact from EVs for at least a decade, Murphy’s looks likely to produce decent, but not spectacular, returns.

Murphy’s current fuel volumes are still 8% below their pre-pandemic peak. They might revert back to 2019 levels, but are unlikely to grow beyond that. Fuel demand will likely be flat, as EPA-mandated MPG efficiencies offset an increase in miles driven.

Fuel margins are likely to remain elevated, though it’s unclear exactly where they’ll stabilize. Long-term, I’d bet they rise. Short term, they may take a step back as they digest their recent leap.

If fuel demand wanes, Murphy's higher cost competitors will need to increase their fuel margins to continue covering their inflating overhead. That will provide cover for low-cost operators like Murphy's to increase margins. This somewhat mitigates the terminal value risk the company is perceived to face. Like tobacco companies, Murphy will likely be able to mitigate lower volumes with higher prices. I don’t think the market understands this even though it is similar to the current dynamic in the oil and gas E&P industry today.

Merchandise contribution will be a focus going forward as the company continues upgrading to bigger stores with more coolers and fresh food. I’d expect something on the order of 3-4% same store sales growth, including fuel. Industry fuel margins have grown at a 4% CAGR from 2008 through 2021.

Store count is likely to increase as Murphy focuses on infilling its best markets, but only modestly. I’m only willing to underwrite 1-2% growth.

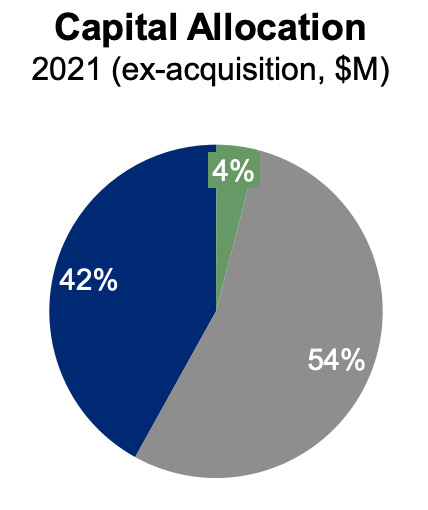

Finally, Murphy will return a significant portion of earnings to shareholders. Since 2016, the company has spent 55% of cash flows on buybacks, and I’d bet that will increase. If future buybacks are done at 16x (the broad market’s median multiple) then EPS will grow 4%. If buybacks are done at a lower multiple (likely) or the company borrows to maintain its leverage as it grows (likely) the stock’s buyback yield could be a little higher.

The company also pays a modest dividend, yielding 0.5%. Murphy has pledged to grow the dividend per share at a double digit rate. That should be easy given how low their payout ratio is and how large their buyback program is.

The stock currently trades for about $300 or 13x trailing 12-month EPS. Value Line’s market median is 16.1x, which seems like a reasonable multiple for Murphy. Over five years multiple expansion from 13x to 16x would add 4% to the stock’s return.

All together, I could foresee 3% same store sales, 2% store growth, 5% yield (buybacks and dividends), and 4% from a multiple re-rating. That sums to 14%. If the multiple re-rating fails to materialize, then the stock’s yield will be a little higher. The business could return about 10% and the stock could do a little better. That is admittedly not the most conservative forecast, but it also doesn't seem crazy.

I'd prefer to buy Murphy’s on a dip closer to 10x earnings than at $300 per share. When buying low growth stocks, buying at a low multiple is absolutely critical.

Historically, Murphy’s stock price is correlated with its fuel margins. After the present period of margin expansion, I wouldn't be shocked to see margins, and the stock, take a step backwards.

It is interesting to compare Murphy USA and Alimentation Couche-Tard because they’re in the same line of business but use different strategies. Alimentation grows by acquisition and is willing to turn around underperforming stores. They may pay 13x EBITDA, but extract synergies so that it works out to 7-8x. Alimentation doesn’t try to sell the cheapest gas on the block so they have higher fuel margins than Murphy but smaller per store volumes.

History has shown that both approaches work well. Murphy’s strategy is more growth constrained, while Alimentation retains a long runway to make acquisitions. The real question will be how these companies cope with EVs and the potential for decline fuel volumes. Alimentation operates a huge network of stores in Norway and is likely to be well prepared, but Murphy’s QuickChek acquisitions suggest they are preparing too.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

Hi Matt, have you planned on revisiting older theses like these after some time has passed?