Magellan Midstream Partners: Price and Value Divergence

It is well documented that stock market participants are often short-sighted. One bad quarter leads to analysts and investors extrapolating recent disappointing results forever. This can lead to undue drops in stocks over short periods of time and create short-term mispricings.

What is less discussed, and probably more rare, is that the stock market can occasionally be too long term focused. This sounds ridiculous coming from someone who consistently preaches about maintaining a long term view, so hear me out.

I’ve found a number of cases that if investors can identify a condition, however far into the future, that may result in a business being severely harmed, the stock will become priced in a way that suggests that the far-off future is instead on the company’s doorstep. The reality is, every business has a judgement day, and the value of a company is simply the amount of cash that the business will produce between now and said judgement day. Investing is about is paying less than the value of the discounted stream of cash that the business will produced for the rest of its life.

Sometimes, just because a potential cause of “death” is identifiable, the stock market places too steep of a discount on the businesses that may be impacted. Magellan Midstream Partners may be such a case.

Background

I’ve written about oil and natural gas pipelines before, so I won’t rehash every detail of the industry. At a high level, Magellan Midstream earns money in a few basic ways.

Magellan transports refined products, which include gasoline, diesel, distillate, and aviation fuel from refineries (who process raw material such as crude oil with additives and turn it into usable energy sources) to endpoints like gas stations, airports, or other fueling stations. About 70% of Magellan’s business involves refined products. The other 30% consists of transporting and storing crude oil.

The business also owns and maintains marine storage terminals in the gulf coast that connect petroleum products from its pipelines to ocean-going vessels.

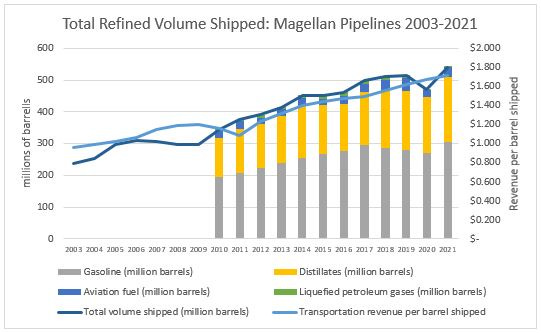

The key drivers for pipeline businesses are pricing and volume. Pricing can be measured by the revenue per barrel that Magellan earns and volume is measured in millions of barrels transported per year. If you listen to the narrative around energy businesses, or check what the stock prices have done in recent years, you’d expect to see both metrics going in the wrong direction, or at a minimum demonstrate great volatility. The facts indicate the opposite. Below are pricing and volume metrics for as long as Magellan has been a public company (they only began breaking out volume mix in 2010).

Source: Author, SEC filings

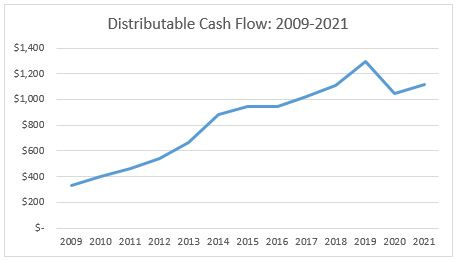

Since 2003, pricing has grown more than 3% annually and volume has grown close to 5% annually. Since the energy bust of 2014 price and volume have CAGR’d at 3% and 2.6%, respectively. Pipelines generate substantial free cash flow. Given the positive trends in price and volume, it isn’t surprising that distributable cash flow has grown steadily as well.

Source: Author, SEC filings

Thanks to expanding margins, a nice feature of businesses that possess pricing power, distributable cash flow has grown at 10.8% annually since 2009 (the earliest apples-apples comparison I can easily gather based on how the SEC filings are organized).

At least so far, the death of the pipeline has been greatly exaggerated. Over the last several years there has been a widening gap between the stock price and underlying business fundamentals for many pipeline companies. This reminds me a lot of tobacco and drug distribution companies over the past five years (each of which have now begun to meaningfully reverse). Of course, what matters is not what’s happened in the past, but what will happen in the future. More on that below.

Competitive Advantages

Pipelines in general, and Magellan specifically, benefit from a few important competitive advantages.

First, Magellan owns a collection of irreplaceable assets. There is virtually no regulatory appetite to build new pipelines in the U.S. Therefore, the pipelines that are in the ground now represent a fixed supply of irreplaceable and mission-critical assets amidst a backdrop of stable-to-growing demand. Magellan owns the longest refined products pipeline system in the nation, at about 9,800 miles. The company has access to over 50% of the nation’s refining capacity which enables customers to advantageously move product to the most profitable endpoints based on commodity prices in different areas of the country. The breadth of their system and independent service provider model give Magellan a strong competitive position compared to other pipelines.

Source: Investor Deck, 2022

In addition to owning high quality assets, Magellan benefits from its favorable contract structures. 85% of Magellan’s business is fee-based, meaning commodity prices have no bearing on profitability. Pipelines earn money based on the “tariff rate”, or prices, they charge customers, as well as volumes. However, many contracts are “take or pay” which means that customers make long term commitments to pay for a fixed volume of barrels and must pay a minimum guaranteed amount to the pipeline companies even if their volumes fall short of the guaranteed level.

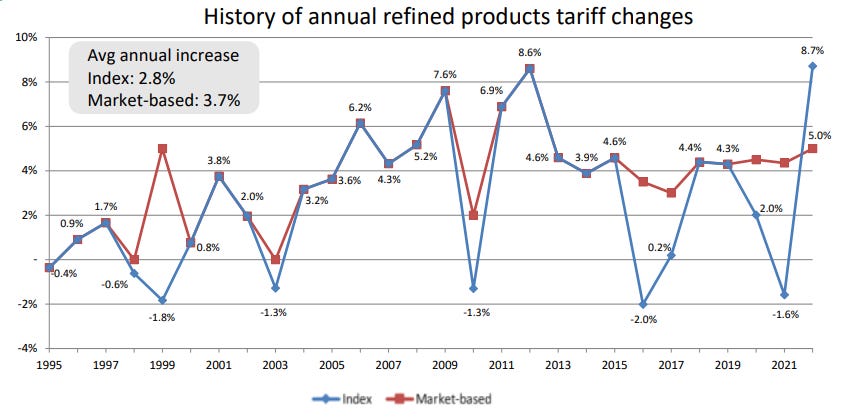

Much like utility companies, because pipelines provide a mission-critical service to the nation the government basically allows the pipeline operators to guarantee an acceptable return on their investments. Magellan’s prices are either indexed or market-based. Index-based prices are determined by the Federal Energy Regulatory Commission, or FERC. In markets deemed non-competitive (i.e. a monopoly), FERC dictates pricing. Historically, FERC has allowed the pipelines to increase rates based on inflation, which is determined by the finished goods PPI index plus 0.78%. This year, because of high rates of inflation, FERC price increases were reduced by about a percent. About 30% of Magellan’s business is subject to FERC regulations and the other 70% is “market-based”, meaning Magellan is free to set prices based on market conditions. Whether you look at index or market-based contracts there is one common theme: pricing power. Below are Magellan’s FERC-based (or index) and market-based price trends by year.

Source: Analyst Day 2022

Though not every year is smooth, the pricing trend is clear. The majority of Magellan’s business very rarely experiences price decreases, and on average they exert 3%+ pricing power annually. Over the next several years, increases are likely to be higher.

Importantly, the contracts allow for price increases to offset declining volumes – again a similar dynamic enjoyed by tobacco companies for decades. This is an aspect that appears to be greatly underappreciated by investors today.

Between formidable barriers to entry thanks to government regulation, a top-notch collection of pipeline assets, and sustained pricing power, Magellan enjoys an excellent business model.

Capital Allocation

Pipeline companies have a well-deserved reputation for poor capital allocation. In the past, pipelines almost universally issued excessive equity during boom times to finance growth projects. This diluted shareholders and resulted in excess capacity in the system coming out of the oil and gas boom during the early 2010s. The aftermath was poor returns for stakeholders across the energy landscape and lots of bankruptcies. In recent years, most pipeline management teams have pivoted to a capital return attitude and are now repurchasing shares, paying healthy dividends, and otherwise refraining from value-destructive growth spending.

Magellan is different. The management team has employed thoughtful capital allocation before thoughtful capital allocation was cool. They’ve issued virtually no stock, they’ve maintained responsible leverage, and have focused on shareholder returns. This has resulted in far superior returns on capital than the rest of the industry over every relevant time period.

Source: Magellan Analyst Day 2022

Expect more of the same going forward. The business has returned more than $8B to shareholders (compared to an $11B market cap) over the past ten years and has grown its distribution for 20 straight years. This all makes sense given the cash flows of the business are tremendously enduring and resilient.

As always, there is never a free lunch, and despite superior returns on capital and excellent capital allocation, Magellan’s stock has not performed well since the energy bust of 2014. A demanding initial valuation and long-term macro risks are to blame. Lets look at the risks first.

Risks

Magellan’s business is directly tied to gasoline demand which is inversely tied to electric vehicle adoption. As electric vehicle hype ramped up over the past several years, so did pessimism towards Magellan’s stock. The question is: how much will electric vehicle adoption impair the demand for the products that run through Magellan’s pipelines, and how quickly might that happen? All of this directly impacts the cash that will come out of the business over the subsequent years and impacts the value of the company for equity holders.

For starters, I am all for climate-friendly projects, electric vehicles, and everything else that might have a favorable impact on our world over the coming generations. My job as an investor, however, is to try to see the world as it is, not the way I want the world to be. Understanding whether or not Magellan’s stock price reflects a realistic future of gasoline consumption requires an understanding of how the world really is based on facts, data, and probabilities - not hope.

No one knows what electric vehicle adoption will look like, but we can use historical analogs as a guide to provide a range of possibilities. Below is an “s curve” adoption chart of game-changing technologies over the last few centuries. Note this graph is from the late-90’s, so the internet and mobile phone adoptions are far higher now. The point is to study adoption rates of comparable products. The graph shows the time period it took for various inventions to gain mass adoption. What trajectory might electric vehicles follow?

Source: Magellan 2022 Analyst Day

Tesla’s Roadster was introduced in 2008 and might be thought of as the first legitimate modern electric vehicle widely available. If EV adoption follows the same adoption curve as TVs, about 80-90% of cars sold in 2050 will be EVs. If it follows the automobile, we are looking at 2100. If it follows electricity adoption, EVs will dominate the market near 2080.

You can pick whatever adoption rate you think makes sense, but I consider electricity a reasonable analog. EVs are not to gas-powered vehicles what TVs were to Radios. The TV was so much more entertaining than the radio, and far less expensive than a car, that rapid adoption was possible and made sense. Having electricity was clearly orders of magnitudes better than previous options, but the nation’s infrastructure had to be built out and costs had to align with what consumers could pay. So far, EVs offer a fine alternative to internal-combustion engine cars, but it’s hard for me to argue they are orders of magnitudes better in terms of getting people from point A to point B. Our electric grid is not close to being able to handle mass EV adoption either, so that will take time to build out.

Regardless of what ends up happening, the base rate for mass adoption, despite whatever projections governments provide, the transition seems likely to take much, much longer than what most people are modeling today.

Even in a scenario where EV uptake is dramatically faster than any of these realistic examples would suggest, and 80% of cars sold are EVs in 2050, 40% of the vehicles in operation will still be gasoline powered in 2050. If the U.S. Energy Information Administration (EIA) is correct, a full 90% of vehicles in operation in 2050 will still be gas powered. Regardless of the projection, there is almost universal agreement that gasoline demand will be stable to growing for at least the next ten years. Beyond that there is a wide variety of projections, but I think the above information is useful in coming up with realistic potential outcomes.

Further, all of the concerns for Magellan’s future business prospects revolve around volume declines and disregard the businesses pricing power. At the risk of sounding repetitive, this is the same reason why tobacco stocks have performed so well in the face of declining volumes over the last several decades. Magellan is likely to exercise pricing power and enjoy expanding margins even when volumes eventually decline, whether that’s in 2040 or 2080. Taken together, it would not surprise me to see at least a stable business for many decades to come.

Valuation and Forward Returns

The narrative around pipeline stocks seems to be that the businesses are in terminal decline, they’re melting ice cubes, and basically un-investable. That may eventually prove true, but that narrative is a story not supported by the fundamentals of the business at present.

For the last several years, pipeline stocks, including Magellan, have traded in tandem with the broader energy index, despite the underlying businesses being far less volatile and much more resilient than upstream energy businesses. A lot of this is a function of demanding starting valuations. In 2014, Magellan’s stock was valued at more than 30x distributable cash flow, a price that reflected an ongoing rosy outlook. Today, thanks to the concerns discussed above and general negative sentiment towards anything related to oil and gas, Magellan trades for around 10x distributable cash flow, or a 10% cash flow yield. The dividend yield is around 8% and management uses excess cash not distributed to unitholders to repurchase shares at bargain prices.

Looking out over the next ten years, Magellan seems likely to grow. Price increases should drive 4-6% growth, and demand for Magellan’s products is likely to be stable to modestly growing. Conservatively, if sales grow 5% and margins hold steady, I can pencil in mid-teens annual returns for stockholders before any sort of valuation re-rating. Magellan has historically traded at 18x earnings, and I believe a mid-teens multiple of earnings is fair for the business. A 3% long-term growth rate in earnings warrants a 15x multiple using a 10% discount rate. Should Magellan trade closer to fair value within five years, it’s not hard to imagine 20%+ total annual returns from recent prices, factoring in dividends. Magellan’s valuation multiple would have to compress substantially further to offset cash distributions and growth over the coming decade. Anything can happen, but resilient businesses backstopped by tremendous cash flow don’t often trade below a 10% cash flow yield for extended periods of time.

Whether or not Magellan’s stock re-rates I do not know, but because the business is drowning in cash and likely to grow, investors do not need a multiple re-rating to achieve satisfactory returns.

Magellan CFO Jeff Holeman captured my thoughts towards the stock’s valuation at the end of the company’s analyst day in March, saying:

The last thing I want to leave you with here today is just a brief comment here on the total return proposition that we think Magellan offers at this point.

We really believe it's a uniquely compelling investment. One thing that we should discuss is our yield remains historically high, okay? And what we tried to show in this low chart to the right, it just shows in green there is our yield going back to '01 and in yellow is the yield on the 10-year treasury. The spread between those 2 yields has averaged about 2.5%, up until the time of the pandemic.

In the last 5 years before the pandemic, it had widened out a little bit to closer to 3%. But since the pandemic, it's been well over 8% on average. And currently, it still sits well over 6%, okay? That doesn't make a lot of sense to us. We think the only way you can justify a spread that wide you have to assume, one, that our cash flows have become way more volatile, which as we've discussed all day, we don't think that's the case. We think they're still very, very predictable. Or two, you have to assume a negative growth rate in the business. And we don't think that makes a lot of sense either for all the reasons we've talked about. Aaron, talked about projections going out to 2050. We think we've got a lot of reasons to feel very confident, certainly about the next 10 years and really longer than that, such that these kinds of negative growth rates that would be necessary to justify this spread, don't really make any sense, okay?

Holeman is basically saying based on the businesses fundamentals it makes no sense that the valuation has compressed so much (another way of saying that the yield has increased). The company certainly thinks the stock is mispriced, and it’s hard for me to disagree.

Summary

I don’t mind owning a volatile stock but I do not prefer to own a volatile business. Magellan’s cash flows are about as predictable as they come. Despite a steady compounding in intrinsic value over the past 10 years, Magellan’s stock price has become unhinged from business fundamentals thanks to concerns about the super long-term outlook for gasoline. Some day Magellan’s pipelines may not be needed, but that day is likely many decades away and investors should collect a lot of cash in the meantime. This may be a rare case of the market thinking too long term.

Simply because a potential cause of “death” is known for a business does not make the business more risky than businesses whose cause of death is unknown. In fact, it can make an investment less risky. Virtually the only thing that can kill Magellan’s business is the obsolescence of gasoline, so investors simply need to focus on thinking critically about how likely that is to occur and when it might start to happen, and then pay a price that more than compensates for that risk.

Whose cash flows are more likely to be impaired in 2050: Magellan’s or a leading technology company? I don’t know the answer for sure, but I will venture to guess that the landscape for every technology business will change much faster than the landscape for a pipeline business over the next 30 years.

A great deal of pessimism and uncertainty is embedded in Magellan’s stock price, and the same can’t be said for many technology stocks, despite recent price declines. Hidden risks are all too often ignored in valuations while known risks can occasionally be over-incorporated into stock prices.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.