Enterprise Products Partners: Irreplaceable Assets and Long-Term Considerations

Enterprise Products Partners: Irreplaceable Assets and Long-Term Considerations

The oil and gas industry can loosely be separated into three spaces; upstream, midstream, and downstream. Historically I’ve been averse to anything associated with oil and gas because of the extreme dependency on extrinsic factors, namely the price of oil. Upstream exploration and production companies find and extract oil and natural gas while downstream companies process hydrocarbons and turn them into useful products like fuel and petrochemicals. Upstream and downstream companies make money in slightly different ways but each tend to be boom and bust because they both earn a commodity-based margin which is heavily influenced by market prices of said commodities. Midstream companies are a different animal, however, and in many cases behave more like a subscription business than a commodity-dependent cyclical.

Midstream Business Model and Background

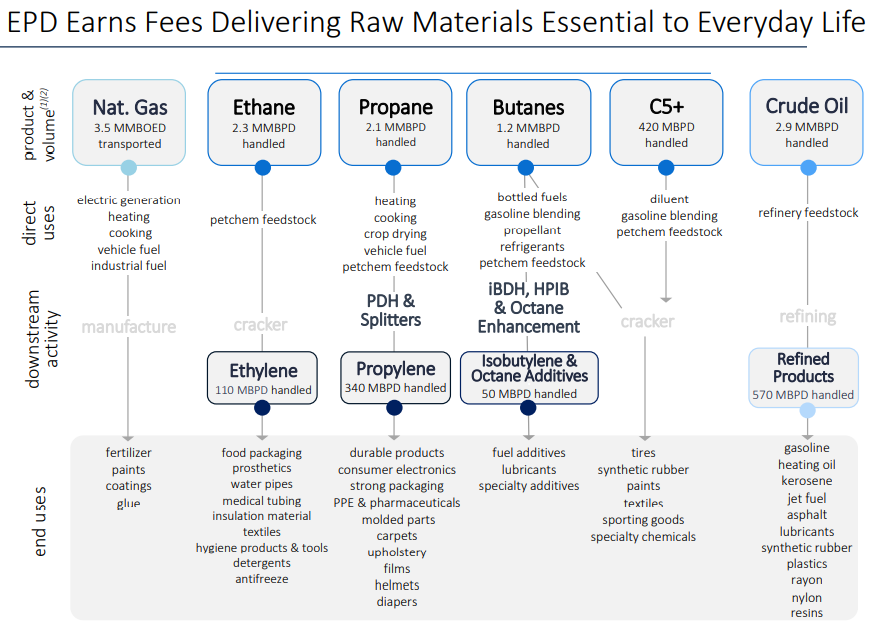

In general, midstream companies earn money by transporting and storing natural resources like crude oil, natural gas, and natural gas liquids (NGLs) from upstream producers to downstream refiners and again from downstream refiners to end users like gas stations or power companies. Oftentimes, rather than earning a spread on the input/output price of the raw material, midstream players earn fee-based revenue based on volumes with a minimum fixed-fee regardless of demand. These are called “take-or-pay” contracts. Below is an example of how a midstream business generates revenue.

Source: 2021 Analyst Day

Building a pipeline is expensive and difficult because of enormous regulatory hurdles. But, once in the ground, maintaining a pipeline is fairly inexpensive. Maintenance capital expenditures tend to be less than 10% of operating cash flow. Recently, it’s been nearly impossible to build new pipelines and delays and cancellations of projects are all over the news thanks to governmental red tape and environmental concerns.

Because of the nature of take-or-pay contracts some pipeline operators produce durable and predictable cash flows through violent commodity price cycles. More on that below.

In the past, most pipeline companies were similar to REITs in that they paid juicy dividends, but because the company didn’t produce enough cash to fund both capex and dividends, the yields were often offset by excessive share issuances to raise capital. A pipeline stock might have offered a 5% dividend yield but issued 3% more shares each year for a paltry 2% “shareholder yield”. This shareholder un-friendly approach has changed in many of the pipelines in recent years.

To make matters worse, pipelines were overinvested in for years during the last big up-cycle in the early 2010’s. Upstream, downstream, and pipeline operators expanded too quickly from 2008 to 2014 resulting in overcapacity across the entire industry when oil prices came crashing down in 2015. This resulted in pricing pressures abound.

Recently, and especially since the COVID-induced oil demand crush and coinciding OPEC price war, any stock associated with the oil and gas industry has performed horribly. Additionally, excitement over the eventual transition to electric vehicles and sustainable energy production along with an emphasis on “ESG” investing has resulted in capital markets largely abandoning energy stocks, pipeline operators included.

So, basically not a lot for investors to be excited about in recent years.

Enterprise Products Partners

Enterprise Products Partners (EPD) is a midstream pipeline operator that is particularly interesting to me for several reasons.

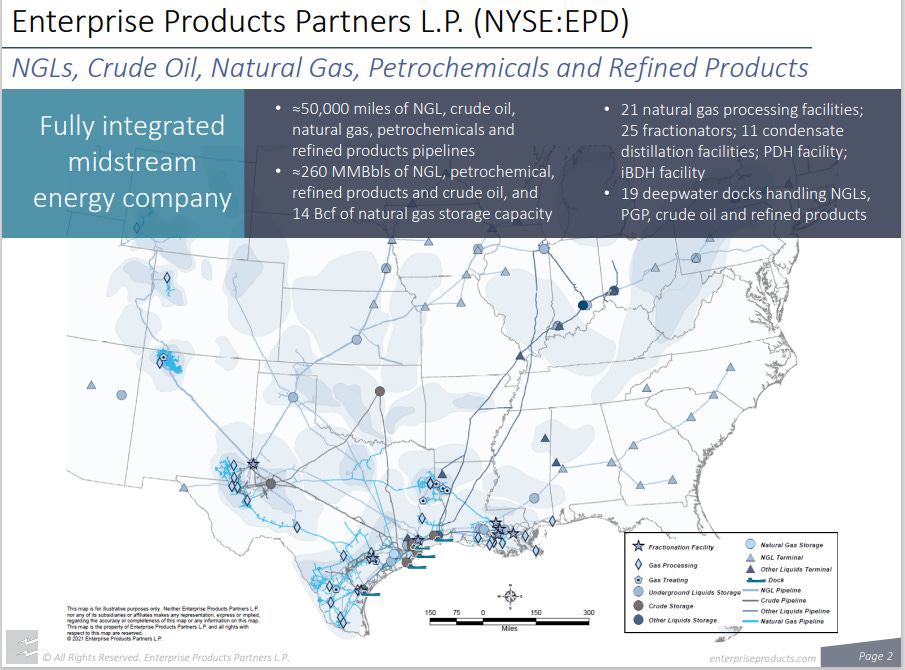

First, roughly 90% of EPD’s contracts are long-term take-or-pay arrangements. This provides excellent visibility into stable and recurring future cash flows. Second, EPD is the largest pipeline operator in the country, which confers a considerable competitive advantage. With 50,000 miles of interconnected pipelines sprawling across the country, EPD can move raw materials to the optimal location for both EPD and its customers. Brent Secrest, the company’s Commercial Officer, described this advantage during the 2021 Analyst day (referring to the map below):

“Virtually everything is connected to something that goes further downstream until it gets to the water, a refiner, a petrochemical facility or another end user. And by starting with the highest sales price and leveraging that through our assets, we are able to maintain volumes and margins throughout the system. What this map also depicts is a series of very valuable options. These options allow us to move hydrocarbons to the most valuable location, to upgrade hydrocarbons into more valuable products and to store these hydrocarbons to take advantage of a premium price at a different point in time. The value of options are time and volatility. You have heard us say in the past that we embrace volatility here at Enterprise. And the volatility in the market this past year and the flexibility of our assets is what allowed us to have such a strong 2020 in an industry that was brought to its knees by the sudden demand destruction”

Source: 2021 Analyst Day

The interconnected value chain is both a) essentially impossible to replicate by competitors and b) the main reason EPD has such a high percentage of take-or-pay contracts. No customer necessarily comes to the table wanting to sign up for a 10-year take-or-pay contract, but EPD is able to sign customers up on these terms because the customers want to leverage the flexibility of EPD’s value chain. EPD allows customers to shift volumes to the right demand centers across the country where they’ll get paid the most and maximize their profit per barrel. Not only does EPD’s massive pipeline system represent a significant moat, it’s also a moat that gets wider every day as new pipeline construction becomes harder. It isn’t hard to understand why Buffett spent $10B last year acquiring natural gas pipeline assets from Dominion Energy.

Next, EPD has a favorable product mix. Half of EPD’s revenue is tied to natural gas and liquid natural gas. Natural gas is likely to play a long-term and important role during the transition to cleaner energy. Someday the world may run strictly on sustainable energy like solar and wind, but we and the rest of the world are nowhere near that point. Natural gas stands to benefit as an important bridge as coal and other “dirty” sources of energy are deemphasized in the coming decades.

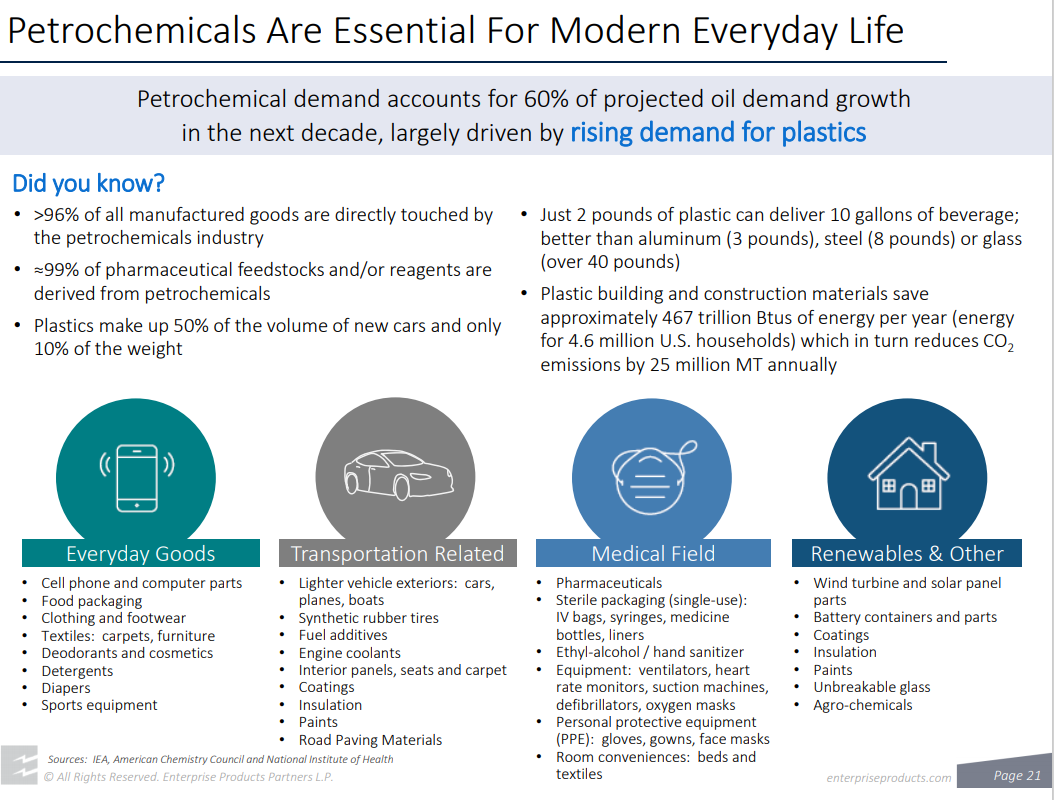

Petrochemicals like ethane, butane, and propane that go into a myriad of consumer products make up ~25% of revenue and represent a significant growth opportunity. As shown below, regardless of what happens in transportation and electricity markets, demand for petrochemicals is not going anywhere and is only set to increase. EPD stands to benefit from this trend.

Source: 2021 Analyst Day

Finally, crude oil transportation and services make up 25% of revenue. While there may come a day when we no longer need large amounts of oil, I doubt anyone reading this article will be alive when that day comes. Energy transitions (from wood to coal, coal to oil, etc.) have historically taken 70-100 years, and one could argue that the U.S. and parts of Europe may be at the beginning of a potential transition away from oil in some areas. Most of the world hasn’t started this transition. With extensive debate and media coverage over a long-term energy transition, at times it feels like many oil and gas companies are on deaths doorstep when in reality that transition seems to be many decades away.

Management and Capital Allocation

Enterprise Products Partners has quality management and is 30% owned by the founding Duncan family. In 2017 management pivoted away from the industry-norm capital allocation approach. The business is now self-funding, no longer issues shares to pay for growth and dividends, and has recently become a net purchaser of its own stock. Leverage has come down and capital expenditures have moderated, resulting in blossoming free cash flow. Christian Nelly, the treasurer, noted the desire to become less dependent on capital markets during this years’ analyst day:

“And we've tried to stay ahead on trends, I'd like to say, because we -- the old MLP model was to pay out all your capital. And then whenever you got ready to either do an acquisition or come in and do make organic growth opportunities, capital expenditures, you had to go out and raise debt capital but also equity capital. I think we were one of the first midstreams that said, okay, we're going to go to equity self-funding…We recognized the need to become less reliant on the equity capital markets. In October 2017, we made the decision to moderate our distribution growth rate. This not only immediately lowered our payout ratio, but we've also not issued external equity since then.”

Source: 2021 Analyst Day

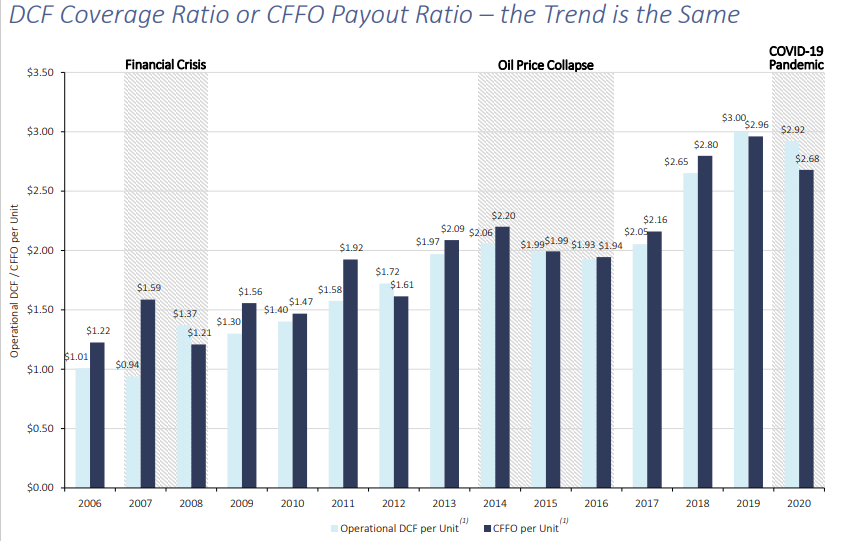

The company has navigated a number of vicious commodity price cycles over the past three decades. Thanks to the take-or-pay nature of customer contracts and the aforementioned competitive advantages, distributable cash flow per unit has grown almost 8% annually since 2006 despite multiple recessions and commodity price collapses.

Source: 2021 Analyst Day

Nothing suggests to me that growth will moderate significantly away from historical trends.

Forward Returns

EPD pays $1.80 per share in dividends, corresponding to an ~8% yield. The dividends are well covered by predictable and growing cash flows. I expect the business to continue growing cash flow per share by mid single-digits for the foreseeable future. The business retains about 40% of earnings and reinvests in its pipeline network at 10-12% incremental returns. This is a decent, not a great, return but the earnings are very durable. This corresponds to ~5% growth in intrinsic value per share on top of the 8% yield. Recently initiated buybacks will likely add modestly to per share returns. The company should see solid growth in demand for petrochemicals while demand for natural gas and crude oil are likely to plod along for decades. All told it does not take any herculean assumptions to envision low-teens annual business return from yield + growth. How about the stock?

EPD trades for about 10x earnings, roughly half of its median P/E over the past decade. You can quibble about what the fair multiple for a high-quality midstream company might be, but I’d argue it is decidedly higher than 10x earnings. Just GDP-like growth of 3% over the long term is worth 15x earnings, and I expect the company to do better than that. If the stock eventually rerates to 15x, annual stock returns could easily exceed 20% annually for many years.

Risks

What could go wrong? The biggest risks I see are a faster decline than expected in volumes and/or an overbuilding of new pipelines. Both scenarios could result in pricing pressures on take-or-pay contracts in future years due to an imbalance in supply and demand. Alternatively, if supply of oil and natural gas is held in check compared to demand (either supply falls less fast or grows slower than demand), pipelines are likely to see pricing power.

I don’t see rapid volume declines or industry-wide over capacity as likely given the demand outlook for and dependency on natural resources, new-found capacity discipline in the industry, and the extreme difficulty of building new pipelines in today’s regulatory environment. Still, these risks shouldn’t be dismissed out of hand for anyone thinking about owning the stock.

The uncertainties appear to be more than discounted by the market today. In recent years the stock price has come untethered from fundamentals. Management commented on this during the Q2 earnings call. Co-CEO W. Randall Fowler said:

“3 years, 5 years, 10 years, we actually have -- our unit price has an inverse correlation to cash flow per unit. It has an inverse correlation to EBITDA. And really, the only correlation, the highest correlation that it has, is to the price of the XLE, the S&P energy sector. So I scratch my head anyway that the cash that we generate, our unit price isn't correlated to the cash that we generate anyway.”

The unhinging of price vs. fundamentals came to a head during COVID when investors could buy the stock for an almost laughable 17% annual dividend yield. Because of the stable nature of EPD’s customer contracts, a dividend cut was never likely, and it never materialized. In fact, EPD raised the dividend modestly in 2020.

The market has not rewarded EPD’s stable and growing cash flows in recent years and the stock has instead traded in-line with boom and bust cyclical commodity businesses. Over the long-run, stock prices tend to follow fundamentals, but it can sometimes take a frustratingly long time for the price and value gap to close. Concerns over long-term threats to the industry from clean energy alternatives may keep valuations down, but substantial cash flow generation cannot be ignored forever. An 8% annual dividend and already low valuation seems likely to provide a margin of safety against bad outcomes for investors at recent prices.

For those willing to stomach some likely share price volatility and industry pessimism, EPD represents a business with a durable competitive advantage linked to irreplaceable assets that generate stable and growing cash flow and can be purchased for roughly half of the current valuation of the S&P 500.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.