Watches Of Switzerland Group: A Value Investor’s Rolex

Rolex is one of the world’s most prized brands. I’ve heard (but not verified) that certain three letter government agencies issue Rolex watches to employees working overseas to use as a last ditch bargaining chip in case they get caught in a pickle.

This anecdote may be more Ian Fleming than reality, but what’s important is that it is at least plausible. Whether crossing a border in Uganda, Ukraine, Uruguay, or the US, the guard at the gate will recognize a Rolex and its value. The Rolex brand has global recognition and desire.

One measure of the strength of a luxury brand is the ratio of the number of people who are aware of it relative to the number of people who can buy it. By this measure Rolex is in a league of its own, surpassed perhaps only by Ferrari.

Rolex’s brand strength grants it pricing power, which is the ability to raise prices without a decrease in unit volume. Pricing power is the holy grail of business qualities because price increases carry 100% incremental margins and require no capital investment. Rolexes are arguably Veblen goods which break the traditional laws of economics (and rationality) because demand for them increases as their prices increase. Men have relatively few ways to flaunt their wealth, and watches are one of them.

The chart below shows that Rolex has increased the price of a No-Date Submariner 7% per year since the 1970s. A no-date sub costs $9,100 today, but good luck actually buying one new. The Watches Of Switzerland explains: “The overall market demand for Swiss watches exceeds production levels and supply. Clients are required to ‘register interest’ for key products.”

All of this is to say that if Rolex were publicly traded, it would be an expensive stock. But we’ll never know for sure because it’s private. Rolex has been wholly owned by a charitable trust, the Hans Wilsdorf Foundation, since 1960.

The closest an investor can get to owning Rolex is owning a Rolex Authorized Dealer (AD) like Watches Of Switzerland Group (WOSG). Rolex’s closest comps, Ferrari and Hermes, trade for ~55x earnings. WOSG, which benefits from the flow-through of Rolex’s pricing power, trades for just 9x earnings, has a net cash balance sheet (prior to this week’s acquisition), and is down 60% from all-time highs.

Before I dive into why WOSG is so cheap, I’ll explain what they do.

WOSG describes themselves as “the biggest, the oldest retailer of Rolex.” Worldwide, it has about a 5% market share. Luxury watches (defined as costing more than CHF 3,000) represent 87% of sales. 7% is from jewelry and 6% is from services. WOSG sells all of the luxury watch brands, not just Rolex.

Rolex makes up about 50% of sales. Patek Philippe, and Audemars Piguet make up another 10%. WOSG refers to Rolex, Patek, and AP as “supply constrained” because demand is a multiple of the supply they have to sell. Cartier, OMEGA, Breitling, TAG Heuer are 15% of sales. A long tail of other brands, big and small, make up the rest .

WOSG has been selling Rolex since 1919, 105 years ago. It’s been selling Cartier for 71 years, Omega for 68 years, Longine for 65 years, Patek Philippe for 55 years, Breitling for 39 years, Hublot for 38 years, and Tag Heuer for 38 years, Jaeger LeCoulture for 32 year, and IWC for 26 years.

Many luxury watch brands are among the oldest businesses in the world: Blancpain dates to 1735, Vacheron Constantin to 1755, Breguet to 1775, Jaeger LeCoultre to 1833, and Patek Philippe to 1839. Rolex is a newcomer, founded in 1905.

These long-lived relationships are hard to replicate. If you or I wanted to become a Rolex Authorized Dealer, the Hans Wilsdorf Trust would tell us to pound sand. It’s not a matter of having deep enough pockets (though that helps), it's about trust. The value of a luxury business lies in their brand. Rolex and Patek Phillipe will not let someone represent them lightly.

WOSG enters into Selective Distribution Agreements with its brand partners. These are a lot like franchise agreements. They’re legally binding contracts that grant WOSG the right to sell their watches in a specific geography and require WOSG to maintain strict presentation standards.

60% of sales are from the UK, where WOSG has a dominant share (45% by value) with 140 showrooms. WOSG is more than twice the size of the next largest UK competitor. The WOSG annual report states:

“The UK market has outperformed the US market and all major European markets since 2000. The UK market has the highest per capita retail spend by domestic clients on luxury watches; we believe the differential to other markets reflects retail investment, not consumer behaviour, creating an opportunity to successfully replicate our model in other geographies and building on the success we have delivered in the US to date.”

One of WOSG’s growth strategies is to replicate its success in the UK in the US.

40% of sales are from the US with 47 showrooms. The WOSG entered the US in 2018 when it acquired Mayors in Florida and Georgia. WOSG purchased Wynn’s stores in Las Vegas in 2019 and built two new stores in NYC (SoHo and Hudson Yards). Since then it has continued to grow by acquisition and greenfield expansion.

The US is ripe for consolidation because it is large and highly fragmented. The US is by far the largest market for Swiss watches.

90% of US retailers are family owned groups that own a handful of stores. WOSG is one of the largest but has only about a 10% market share. Its largest competitor, Bucherer, is similarly sized in the US, much smaller in the UK (5% share), and much larger in Europe.

Every acquisition requires Rolex and the other brands' blessing. This limits competition for the assets and leads to high returns on equity (more on this later). Recently Rolex, Patek Philippe and other brands have been rationalizing distribution by reducing the number of dealers to a smaller number of higher quality retailers. They prefer to have a few, large showrooms in major cities rather than more, smaller, points of distribution in smaller cities and suburbs. This benefits WOSG, who has the capital and willingness to invest in large flagship stores. Rolex was happy to see WOSG enter the US for this reason.

WOSG’s SoHo store shows the level of investment Rolex wants. It’s an 8,000 sqft showroom that sells 15 brands, including Rolex, Jaeger-LeCoultre, Cartier, and Omega. It showcases several vintage timepieces, has an in-house cocktail bar, a curated library of collectible watch books and an evolving collection of photographic artwork available for purchase.

{kind=link}

WOSG’s market position reminds me of Alimentation Couche Tard’s today and AutoZone’s twenty years ago. It’s small in an absolute sense but dominant relative to its peers. It is one of two scaled incumbents who have an advantage over their mom-and-pop competitors.

Selling luxury watches is a much better business than your typical retail operation. First, there are barriers to entry. Rolex and the other brands grant their dealers geographic monopolies. Second, the inventory faces zero obsolescence risk. Rolex and the other brands have hardly changed their watches in over a hundred years. There is minimal technological change. Quartz and smart watches have already done all the damage they’re going to do. Luxury Swiss watches use technology developed in the 1700s. They’re about form, not function.

The picture below shows all three models of the Rolex Submariner released between 1988 and the present. It is an evolution, not a revolution, of design.

Discontinued watches instantly become rare and even more valuable. There are never discounts. Shrinkage is minimal, since inventory is held under lock and key.

The business is relatively inflation-proof because it operates under fixed margins with its brands. When Rolex increases wholesale prices, is flows through and benefits WOSG. Single-SKU inflation averaged 3% over the 30 years to 2020. The brands raised prices more aggressively since, to reflect inflation, the strength of the Swiss Franc, and the price of gold, platinum, and diamonds.

WOSG buys inventory in its local currency (USD or GBP). The brands take the FX risk. An appreciating Swiss Franc relative to the USD or GBP will prompt Rolex to increase USD and GBP prices, which benefits WOSG.

You may be surprised to find out that your local Rolex dealer doesn’t actually have inventory on hand to sell you. They’ll have a few display pieces, and that’s it. You’ll have to speak with an associate and explain what you want. They’ll fill out a “registry of interest,” put you on their wait list, and give you a call when they get your piece in.

If they call you, you have the option, but not the obligation, to buy the watch. If you don’t, the next person on the waitlist will. There’s no telling when you’ll get the call or how many people are on the list ahead of you. There is no official or public wait list. Wait times range from months to years, depending on the model. WOSG stops adding people to its wait list after it is two years long.

Buying a Rolex is an intentionally opaque process to make it a treasure-hunt experience. By the time Rolex calls you, you’ll consider it a privilege to fork over $10k+, which is exactly what they want. Wait list customers typically show up to buy their watch within 24 hours. WOSG reports that its waitlists are firm, even today.

The majority of WOSG’s inventory is essentially pre-sold via these wait lists, producing rapid inventory turns and negative working capital. How long are the waitlists? WOSG commented in November 2022:

“Wait lists, we don't give out specific numbers, but it's not a percentage of annual revenue, it's more like a multiple. They’re pretty significant, the depth of the waiting lists.”

So WOSG has ~60% of sales essentially locked in for the next two years at ever increasing prices. It’s definitely not your typical retailer.

Since WOSG sells Rolex, Patek Philippe, and Audmars Piguet inventory instantly upon arrival and has 60 days to pay for it, it generates negative working capital. Negative working capital is one of my favorite business qualities (behind pricing power) because it produces high returns on equity and makes a business less susceptible to inflation. Since inventory is sold before it is paid for, negative working capital businesses do not have to invest ever-increasing amounts in inventory in an inflationary environment. McKesson, AutoZone, and Costco are some notable examples of negative working capital businesses.

Wait lists produce revenue visibility and minimize the need to warehouse inventory. Rolex ships directly from their factory to WOSG where the watches are vaulted and sold days later. Rolex prohibits selling new watches online. There’s no risk of Amazon coming in and disrupting WOSG. WOSG does sell pre-owned watches online. Some brands allow online sales, but only for dealers that already operate brick and mortar boutiques. WOSG stands to benefit from a shift towards multi-channel sales because it has the scale to build a top notch online shopping experience. A family that owns 1-3 dealers simply cannot afford to build the same online experience.

WOSG benefits from their partners' brands without having to do much advertising. They also benefit from the flow-through of brands’ price increases. All of this makes for an excellent financial profile: low teens gross margins, ~10% operating margins, and 20-30% unlevered ROEs.

Last year Rolex rolled out a certified pre-owned program (CPO). Dealers can now sell pre-owned watches with Rolex certifications and warranties. Rolex gets to directly influence second-hand prices and increase liquidity. Stable, liquid secondary market prices help frame a Rolex as an investment rather than consumption. Dealers benefit by getting more inventory to sell. Walk-ins ready to buy a Rolex but put off by a multi-year waitlist can leave with a CPO Rolex in like-new condition the same day. CPO will be a tailwind for WOSG.

The downside of WOSG’s retail model is that they’re beholden to a few key suppliers. The luxury Swiss watch industry is an oligopoly. Four groups collectively hold 76% market share: Rolex, Swatch, Richemont, and LVMH. Imagine if Costco bought 76% of its inventory from four suppliers. It wouldn’t have any bargaining power and wouldn’t be a great business. I’ll have more to say on WOSG’s relationship with the watch manufacturers later, because it is a key reason the stock is so cheap today.

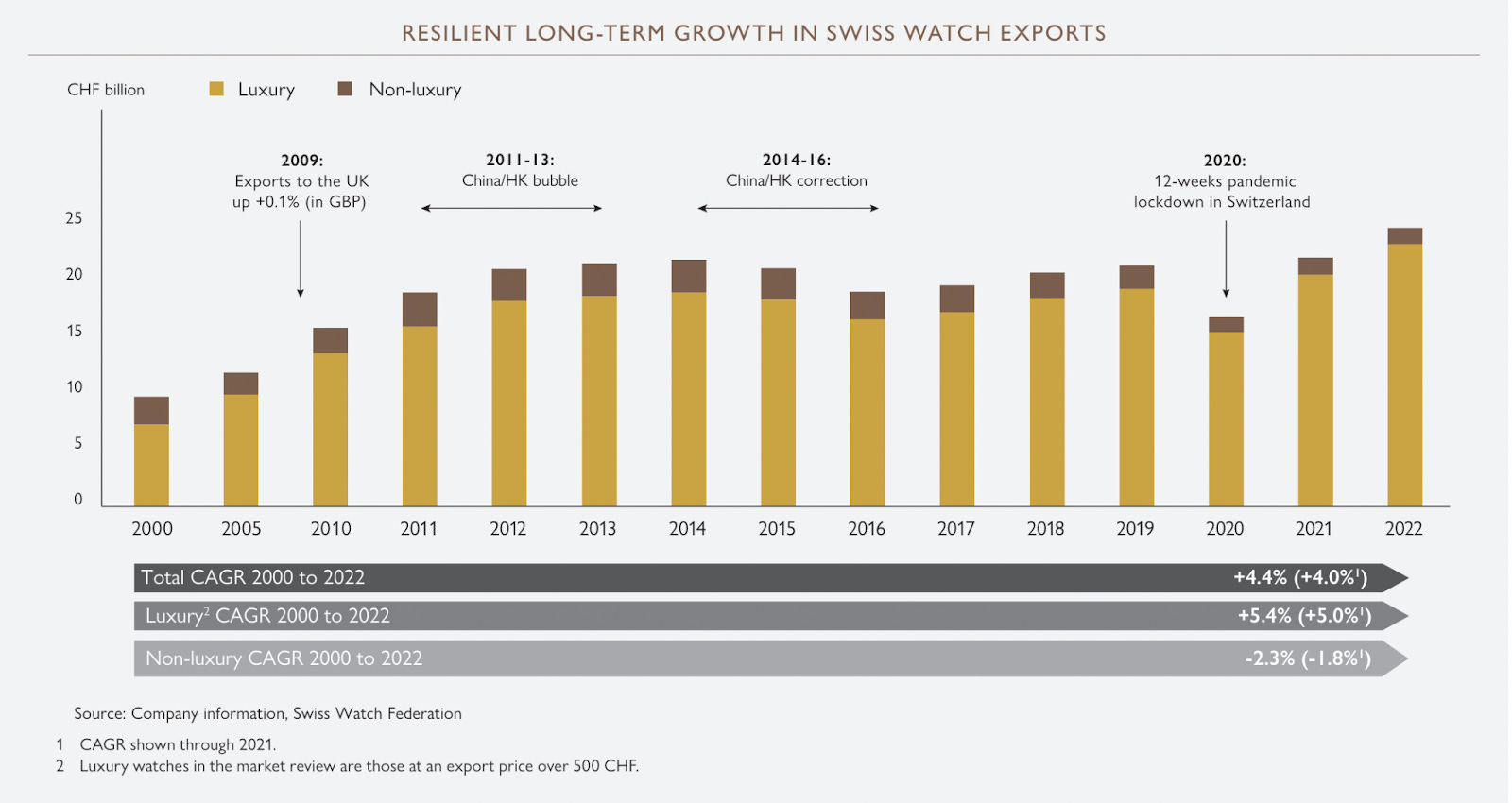

Why are Rolexes and other Swiss luxury watches in short supply? The pandemic produced a perfect storm of demand: stimulus, booming stock (and crypto) markets, and no services or experiences to spend on. Lockdowns in Switzerland reduced supply while demand was booming. One writer called it an “unprecedented feeding frenzy for stainless steel sports watches.”

Back in the 1990s you could usually walk into a Rolex dealer and walk out with a watch on the same day. Waitlists were only for the most sought-after, low production models, like the Rolex Daytona. Year by year, demand increased and waitlists become necessary for more and more models. By 2018-2019, a waitlist was necessary for virtually every Rolex model. The pandemic poured fuel on this fire.

It got so bad that in September 2021 Rolex broke its silence and issued a statement on the supply-demand mis-match:

“The scarcity of our products is not a strategy on our part. Our current production cannot meet the existing demand in an exhaustive way, at least not without reducing the quality of our watches – something we refuse to do as the quality of our products must never be compromised.”

Morgan Stanley estimates that Rolex sold 1.24 million watches in 2023, which is up from about 810,000 in 2019 (+53%, 8.8% CAGR). Rolex is building a new factory that will come online in 2029 and will reportedly have temporary facilities available by 2025. This should dramatically increase Rolex’s production capacity, but don’t expect it to flood the market. The luxury strategy dictates that supply should grow slower than demand and that quality must be maintained at all costs. Audmars Piguet has also broken ground on a new factory due to come on line in 2025. Increased supply will benefit WOSG.

Will waitlists always be necessary? They’re certainly good for dealers. It is hard to say for sure. The pandemic-induced boom in luxury watches is normalizing, but unlikely to fall off a cliff. Rolex and the other Swiss watch makers have every incentive to grow supply slower than demand, keep secondary market prices high, and prevent a flood of supply from watering down their brand. This isn’t a situation like auto OEMs who have an incentive to stuff their dealer channel full of inventory when the cycle begins to turn.

WOSG might be over earning a little right now, but not dramatically. The Swiss watch industry is resilient and only mildly cyclical. When it gets into a funk, it tends to snap back quickly. The second hand market (known as the “grey” market) got hot in 2021, but that’s limited to a few models and not reflective of the broad industry.

If the Swiss watch market is so stable then why is WOSG so cheap?

WOSG was founded in 1924 and has had a series of owners since then. Apollo bought it in 2013 and took it public in May 2019. The company’s stock rode the pandemic-induced watch feeding frenzy, peaking in December 2021 at 1,420 pence per share, a 54x P/E multiple. The stock drifted lower as the crypto/meme-stock bubble deflated in 2022. In 2023 WOSG began to report slowing growth and a softening watch market. Consumers began to prioritize travel and services over watches and jewelry. They were also pressured by a dramatic increase in the cost of living and watch prices. Its the same post-pandemic whiplash we’ve seen in other industries.

In August 2023 Rolex acquired one of its largest dealers, Bucherer AG. Investors took this as a sign that Rolex intends to disintermediate its dealer network. WOSG’s stock plummeted.

However, these fears are unfounded and don’t hold up under scrutiny. Rolex said:

“Following the choice made by Jörg Bucherer, in the absence of direct descendants, to sell his company’s business, Rolex has decided to acquire the watch retailer, which was until now an independent entity. This move reflects the Geneva-based brand’s desire to perpetuate the success of Bucherer and preserve the close partnership ties that have linked both companies since 1924”

Carl-Friedrich Bucherer founded Bucherer in 1888. Bucherer began working with Hans Wilsdorf to sell Rolexes in 1924. The company was under its third generation of ownership when Rolex bought it. The owner, Jörg Bucherer, was in his eighties and had no heirs. He wanted the company’s Swiss heritage to remain intact, which is why he ruled out a sale to WOSG.

Rolex bought Bucherer as a defensive move. It was an “elegant solution” in their words. Rolex did not want the company to fall into the hands of its competitors, Richemont, LVMH, or Swatch. Besides those, only private equity was likely to have the capital to pull off a ~$1 billion acquisition.

Rolex gave WOSG’s management a heads up that this deal was in the works. And Rolex has publicly declared that they will run Bucherer at arm's length. Nothing will change. Not management, nor Rolex’s allocation policies to its authorized dealers.

WOSG’s stock dropped 30% the day the Bucherer acquisition was announced and has continued to slide since. The market obviously doesn’t believe that Rolex’s stated intentions are earnest.

Audemars Piguet is probably the reason. In 2018 Reuters wrote:

Swiss watch brand Audemars Piguet wants to totally control the distribution of its luxury watches, cutting out third-party multibrand retailers, within three to five years, its head told Reuters, adding the integration would boost sales.

"We'll accelerate the consolidation process to arrive at a totally integrated retail network," Chief Executive Francois-Henry Bennahmias said in reply to emailed questions. "That should happen within three to five years.

Since then, Audemars Piguet has clarified that they want their watches sold exclusively through mono-brand boutiques. It will own and operate some, with others owned and operated by dealers like WOSG. This is an industry-wide trend, and one suited to WOSG.

At a upper end of the market, WOSG can spend millions to build state of the art flagships, like it's doing in a JV with Audmars Piguet in London. On the lower end, WOSG can create distinct storefronts next to each other, each a mono-brand. As far as the public is concerned, these stores are separate entities that happen to be clustered together. WOSG can run the bunch as if they were a single store.

The market is missing that it is a lot easier for Audemars Piguet to bring some of its distribution in house when they only sell 40,000 watches a year. Selling 40,000 watches is a completely different animal than selling 1.24 million watches like Rolex. Audemars Piguet needs a lot fewer points of sale than Rolex, and the expectations for those locations are higher, commensurate with Audemars Piguet’s substantially higher prices than Rolex.

Most brands lack the capital to bring distribution fully in-house. Smaller brands cannot justify too many mono-brand boutiques. The only way to increase the points of sale is to sell through multi-brand dealers. Some brands also sell better in a multi-brand boutique. Merely being sold in the same shop as a Rolex elevates their brand and perceived luxury.

Cutting out dealers is easier said than done. It might look good on a spreadsheet, but in practice it's hard, messy work. Rolex operates in over 100 countries and would need to manage real estate and hiring in each. The only practical route to bring distribution in house would be to buy its dealers, which would require paying a premium for WOSG. If Rolex were to bring distribution in house, it would proceed at a glacial pace. Rolex is run by a charitable trust and thinks generationally. They’re in no hurry.

Absolute worst case, if Rolex did disintermediate WOSG tomorrow, their stock would still have all of its other brands to sell and would trade at a 18x PE instead of a 9x. I attach zero probability to this, but include it to illustrate how cheap WOSG is.

Besides disintermediation, there’s a fear that the watch cycle has turned for the worse. While that’s certainly true, the luxury watch market’s troughs are not usually too deep. The wealthy are much more insulated from macroeconomic pressures than your typical consumer. Long wait lists, stretching years, underpin the stability of WOSG’s revenues. Sure, people on the waitlist could flake. At the margin, that’s beginning to happen. But WOSG stresses that it is minor and marginal. The vast majority of people who “get the call” are there within 24 hours. Rolex and Audmars Piguet would not be building new factories if they thought their products' popularity was a fad.

On Thursday (May 16) WOSG reported earnings and the stock rallied 20%. Notably, they announced that they’ve acquired the North American distributor for Roberto Coin branded jewelry. They announced that they’ll exit their few stores in Europe and focus on the large opportunity in America. And, perhaps most importantly, they reported relatively stable earnings. The US continues to power ahead (sales +10%) while the UK languishes (sales -4%) under more severe cost of living pressures. All and all pretty solid and showcasing the resilience of the business.

WOSG has discussions every January with its major brand partners to discuss inventory allocations for the year ahead. Rolex will commit to deliver a specific number of units to WOSG. WOSG says they're never short and always keep to their word. If anything, they deliver a little extra.

WOSG doesn’t know exactly what will be delivered. Rolex adjusts its manufacturing to demand. During the pandemic there was a premiumization effect. Customers preferred watches made of gold and precious metals. These carry higher prices, which benefitted WOSG. As the market has cooled and inflation bites, customers have shifted back towards cheaper stainless steel options. Rolex began delivering more of these in 2023, pressuring WOSG’s average selling price. It is a modest headwind that will even out over the long haul.

WOSG’s costs in the watch business are roughly 75% inventory, 10% people, <10% rent, and smaller amount of marketing spend. Watches are sold on fixed margins. Rolex allows dealers higher margins to compensate them for lower productivity stores. Historically, WOSG’s Rolex margins were higher in the US than the UK. As WOSG invested and the US market began to perform, Rolex took away some of WOSG’s US margin. On balance, WOSG earns a higher return on equity which is all that really matters.

WOSG leases real estate on largely fixed terms. Spaces are typically let on 5 year terms with an optional 5 year renewal. If WOSG keeps the store after 5 years, they’ll usually remodel. Stores are always in the nice part of town, but small: 1,000-3,000 sqft.

Last week’s acquisition of Roberto Coin pushes WOSG more firmly into the banded jewelry space. Branded jewelry continues to take share of total jewelry sales, has more pricing power, and is more collectible. WOSG is already in the jewelry business and likes it. The gross margins are better than watches (45%) but sales are slightly more cyclical and seasonal (winter). Roberto Coin sells at a price point a bit above Tiffany’s. I’d have preferred WOSG stick to acquiring and building Rolex dealers, but this acquisition was in-line with what the company has communicated for years and not outside of their circle of competence. It helps WOSG diversify its business and supplier base.

After the acquisition, WOSG will have 0.8x debt. Historically WOSG has delivered quickly following an acquisition. The company generates lots of cash flow and has minimal maintenance capex requirements (leased, small footprint real estate, minimal/negative working capital). It reinvests virtually 100% of its prodigious owner’s earnings at 20-30% incremental ROEs.

Last year it earned GBP 210 million of operating cash flow. It plans to spend, on average, GBP 60-70 million to remodel, relocate, or expand existing showrooms. These have a 2-4 year payback and are a “a proven model with good returns.” They’ll spend another GBP 70-100m on acquisitions and greenfield store expansion. They have a good track record here with payback averaging 4-4.5 years. Over time, WOSG expects operating leverage to average 50-150bps per year.

Management incentives are good. They’re compensated on 3-year average return on capital employed (ROCE) and three-year cumulative EPS.

Looking ahead, WOSG’s growth will be driven primarily by acquiring and building new boutiques for Rolex and its other brand partners. The company has tailwinds from Certified Pre-Owned and e-commerce. WOSG will benefit from the pricing pass-through on brands. Long, multi-year waitlists for WOSG’s “supply-constrained brands” that make up the majority of sales mute some of the industry’ cyclicality as the pandemic’s effects wear off. It is a simple, predictable, and profitable business with proven economics and a long runway to replicate them. After this week’s earnings pop, the stock trades for 9x earnings. While earnings could certainly fluctuate downward, I don’t see this business losing money in any given year. Earnings are virtually certain to be materially higher in several years time. And if that’s the case, the multiple will very likely also move higher too.

Further Reading

Do you have a “stranded” 401k from a past job that is neglected and unmanaged? These accounts are often an excellent fit for Eagle Point Capital’s long-term investment approach. Eagle Point manages separately manage accounts for retail investors. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

Thanks again Matt for the write up on WOSG. I’ve spent the last 3-4 weeks doing a deep dive into them, and the value proposition at their current valuation looks very attractive. The main reason for the current price as you mentioned does seem to be the market seeing a risk in Rolex taking away product from WOSG altogether (even if 100% did go overnight, the stock would likely still be BE over the next few years).

The main focus therefore was on evidence for and against Rolex doing this. The only evidence for Rolex wanting to do this is their purchase of Bucherer, which if the current owner had someone in the family to succeed him, wouldn’t even be a point. Rolex didn’t go out to buy a dealer as part of a new plan, it seems likely to be (nearly) entirely motivated by just keeping Bucherer out of the hands of a luxury fashion rival.

However, for arguments that Rolex and WOSG will keep their strong partnership, there are many:

WOSG is the largest Rolex AD in the UK and the U.S

They have a 100 year partnership selling Rolex, which itself respects longevity and generational change.

As stated in their YE24 report, WOSG have their strongest ever lineup of new showrooms including Rolex, out to YE26. Each showroom is individually approved by Rolex. Why would they be approving a record level of new showrooms if their plan was to suddenly take away WOSG as an authorized dealer.

WOSG’s long term plan going to YE28 was also fully discussed with Rolex, after the Bucherer announcement. Rolex is strongly incentivised to provide WOSG with more supply, so they can in turn invest in better showrooms in more prestigious locations, a win-win. Rolex also works with WOSG on their service and marketing, so it’s already co-working with them on all aspects of retail.

Rolex is building new manufacturing capacity, which a) takes capital, b) the new supply needs new showrooms to sell in, making it even less likely for Rolex to want build out a whole retail operation to replace their current AD’s

Given all these points, my conclusion is currently that there is below a 2% chance of Rolex cutting WOSG out completely. My conservative Base Case for WOSG is for them to hit just 2/3rds of their Long Term Plan (£1bill rev increase vs their plan for at least an additional £1.5bill in revenue vs FY23), flat Adj EBIT margins (vs their goal of 50bp to 150bp expansion and a conservative P/E of 15x by YE28 (April 2028) (given that the UK and U.S luxury watch markets are likely to continue growing at >5% a year, even without WOGS taking more share (not even accounting for Certified Pre-Owned and luxury jewelry which is likely faster)

= £10.80 per share, 29% IRR for nearly 4 years.

Bull case growing 17% CAGR from YE23, P/E 20 gets a April 2028 share price of £23.00

(WOSG rev growth in the 8 years to YE23 was 19.8% CAGR)

(Taking the view that the luxury watch market in UK and U.S will continue growing similar to as it has, second hand luxury watch market will bottom out in next 1-2 years. Rolex has raised prices slightly above inflation (on average over multi-year period) for the last 70 years+)

Best regards

Jack

If it's a home-run investment, I owe you a beer

Enjoyed this, thanks. Regarding waitlists, found this video on YT doing some DD that gives an interesting perspective.

https://youtu.be/YbQTCrW2L_4?si=lOYpHv0TOchyPj8m