The Toll Roads of the Music Industry

The Toll Roads of the Music Industry

Streaming has transformed music labels into rapidly growing annuities with an exploding addressable market.

Few things are as ubiquitous as human’s love of music. People take for granted how easy it now is to access millions of songs with the touch of a button. What’s going on behind the scenes and who makes money from our voracious appetite for music new and old? The music industry is complex and has undergone a seismic shift over the last several years thanks to the emergence of Digital Streaming Platforms (DSPs) like Spotify and Apple Music. Here I’ll endeavor to tackle an overview of the recorded music industry and zoom in on what I consider one of the more attractive businesses in the world today; music labels.

Music Industry Overview

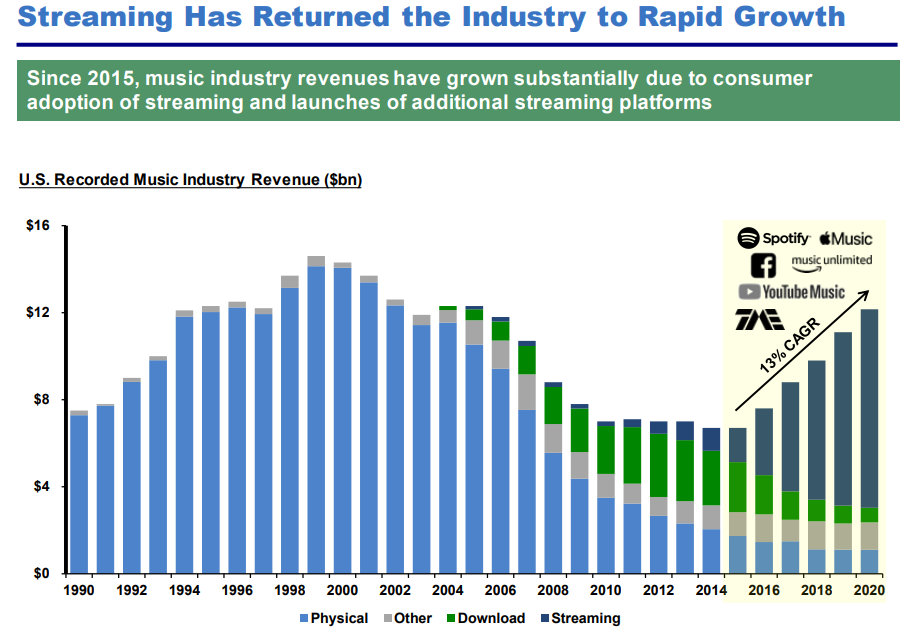

Music may sit behind food and water as one of the great commonalities across the globe. It has been around forever, though the industry has gone through periods of growth and decline over time. Sales of recorded music in the U.S. peaked in the late 1990’s. Any reference here to the music industry is to recorded music; live music is a whole different animal.

The way we access and listen to music has changed immensely in the last two decades. When the industry peaked in the ‘90s, sales were almost exclusively driven by one-time physical purchases of CDs or records. Listeners were basically forced into buying “bundles” of songs, regardless of whether they just wanted to listen to a few tracks from an album. In the early 2000s along came the internet and platforms like Napster allowed consumers to download (often pirated) versions of music. Apple launched iTunes which un-bundled albums and enabled single-song purchases for one dollar. YouTube and other social media platforms provided access to millions of songs for free and on demand in ways that were previously impossible. All of these developments resulted in a slow decay in recorded music sales until streaming started to take hold around 2014.

Source: PSTH Universal Music Group Presentation (June 2021)

Since 2014 the U.S. music industry has grown rapidly, but revenue per capita still sits 55% below its inflation-adjusted peak.

Source: PSTH Universal Music Group Presentation (June 2021)

Basically the industry was booming, the internet led to people spending far less money on music because they could get it for free, and now things are coming back. With that 50,000 foot view, let’s look at the players and how they make money.

Industry Players

The main constituents in the recorded music industry are the artists, writers, music labels, DSPs, and listeners. Obviously in some cases the writer and artist/performer can be the same person, though often times they are not.

When an aspiring artist writes a song, or performs a song someone else writes, she needs to find a way to record it. This can be done as simply as recording it on her iPhone, or as sophisticated as recording it in an expensive studio. Most artists wish to become famous and have their music widely listened to. So, the song needs to get out to as many listeners as possible as efficiently as possible. Again the artist has some choices here. She can throw her song out on Youtube or TikTok, hoping it somehow goes viral, or she can turn to those that have the means to distribute her song across platforms all over the world.

Clearly, if the above aspiring artist has any real shot of making it in the music industry, she can’t go the iPhone and TikTok route to record and distribute her work; she needs the help of professionals. That’s where music labels come in.

Music labels play a central role in the music industry. There are three main labels that own over 70% of the music market in the “Western” World: Universal Music Group (32% share), Sony Music (21%), and Warner Music Group (16%). Music labels specialize in finding new artists, recording and producing their songs, and most importantly marketing and distributing their music to millions of listener’s ears across the globe in an efficient manner.

Industry Economics

In exchange for producing and distributing an artist’s music, the labels generally take ownership of the Intellectual Property (IP) of an artist’s songs and earn a substantial portion of the revenue derived from the artist’s songs.

As a quick but important aside, a song can be thought of as two separate pieces of IP; the Composition and the Recording (or Master). The Composition is the physical words and notes on paper (or a screen) while the Recording is the song that is recorded for us to listen to. Music labels make money on both aspects as they often serve as the publisher and as the distributor of recorded music. Publishers pitch compositions to artists and then earn money when they are recorded and distributed. Most of the labels revenue comes from the Recorded Music side in which they identify talent and orchestrate the production, marketing, distribution and monetization of the Master.

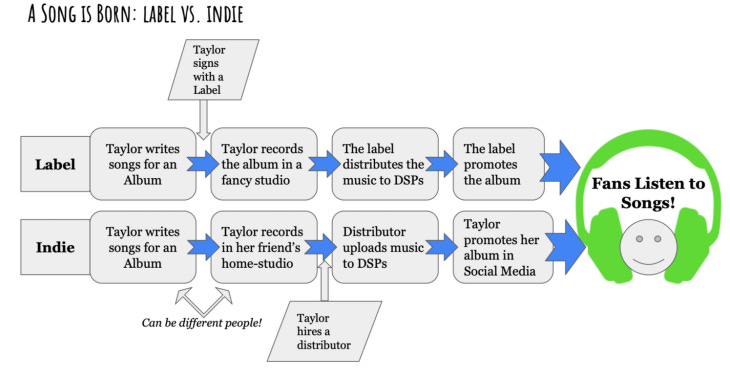

This graphic, which I’ll describe below, summarizes the process and role a label plays vs. an “Indie” artist (or one that attempts to go it alone without signing on with a major label).

Source: Music Streaming Royalties 101 (Sleepwell Strategy Blog)

A typical (simplified) arrangement might look like this. A hopeful singer-songwriter writes some songs and is discovered by a music label. The label thinks the artist has promise and the artist needs a way to professionally produce and distribute their music. It’s expensive to access a fancy music studio and market an album and the artist can’t come close to affording it on their own. So, the label gives the artist an advance “loan” to cover production costs, the artist’s cost of living while the album is being produced, and initial marketing expenses.

Let’s say the album turns out well and the label decides to market it across numerous platforms – Spotify, Amazon Music, physical retail locations, etc. – and the artist is a hit. Spotify pays the music label a percentage of it’s subscription and ad revenue in exchange for using its IP on the platform. Labels earn something like 70% of the revenue generated from their songs on streaming platforms. The label recoups its initial “loan” it made to the artist and then splits the ongoing royalty payments with the artists. Again the label keeps a majority of the earnings because they took the financial risk on the artist and own the IP, though agreements vary widely based on the popularity of an artist.

There is quite a bit more to this process than I’ve outlined above, and if you’re interested in the gory details of how songs are monetized and split between artists, publishers, and distributors, I’d highly recommend Sleepwell Strategy’s blog post from earlier this year.

One way to think about the music label’s business model is that of a Venture Capitalist for music. The labels invest their own capital backing up and coming artists, the vast majority of whom do not become financially successful. The labels business is driven by power laws and the few big winners, much like a VC fund. The winners don’t love giving up economics to the label, much like a founder doesn’t like giving part of his business away to a VC fund. Nonetheless it’s a necessary relationship in order for the industry to exist as it does and the winners themselves largely wouldn’t exist without this dynamic.

The main functions of the major labels haven’t changed much over the decades. They have always and continue to specialize in discovering talented artists, making them famous, and profiting off of such activities. However, the shift to streaming has dramatically changed the labels competitive position and business model fundamentals.

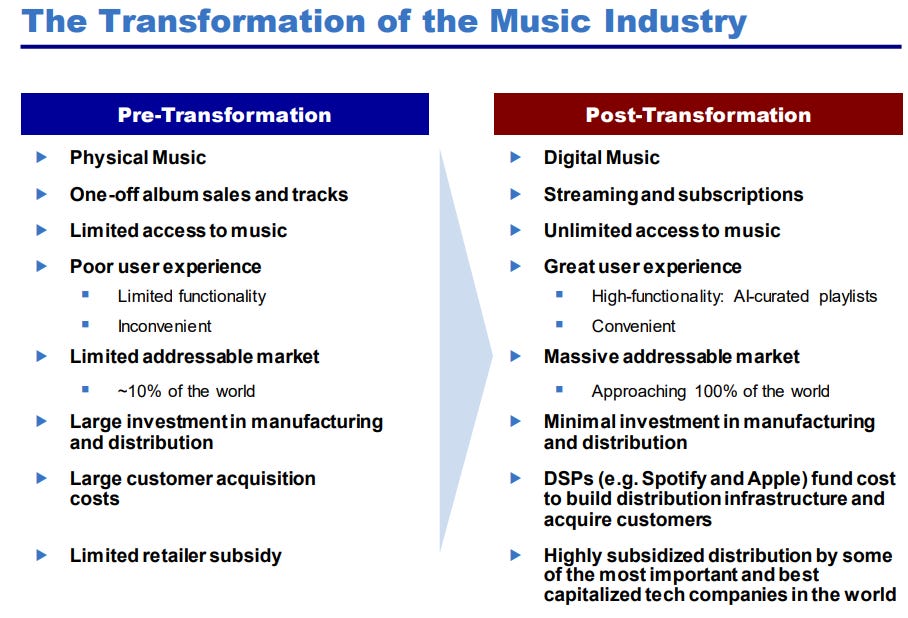

How Streaming Transformed the Industry

In the “olden days”, or prior to early 2010’s when streaming became mainstream, the music label business was good but not great. Producing songs was capital intensive as physical CDs had to be manufactured, stored and distributed across retail locations. This took a lot of money and resources. Further, monetization was lumpy and centered around new album releases.

Streaming changed things in a few important ways. First, monetization from music switched from being one-off to being perpetual and subscription-based. Second, producing music became capital light because music is now distributed as bits over the internet instead of physical CD’s through stores. Finally, the addressable market has exploded. Now, anyone with an internet connection is a potential monetize-able user.

Source: PSTH Universal Music Group Presentation (June 2021)

This transformation has not only made the music label business much more attractive, but it has cemented the labels competitive advantages in somewhat counterintuitive ways.

Music Label’s Competitive Advantages

A great distillation of the inherent strength of the large music labels was summarized in an interview with Arman Gokgol-Kline, a partner and investor at Ruane, Cunniff & Goldfarb, when he joined Patrick O'Shaughnessy on the “Business Breakdowns” podcast earlier this year. Gokgol-Kline described a conversation he had with a music professor from the esteemed Berkeley College of Music (emphasis mine):

“It’s funny, I spoke to a professor at Berkeley College of Music, which one of creme-de-la-creme music schools in the country, about various aspects of this business. And one of my favorite stories he told me is every year I ask my students to raise their hand when I say to them, “Who likes labels and wants to work with a label?” And nobody raises their hand. And then he says, “Okay, now imagine one of the major labels comes to you and gives you an upfront and wants to sign you. Who would sign on with them?” And everyone raises their hand. I think it’s part of this is as an artist, you don’t love the idea of being beholden to profit driven organization that’s going to take a cut of your profits...But the reality is we’ve seen from share that they’re necessary. And to this day, the number of artists that have come to market and succeeded like a Billie Eilish without the support of a major label, I can certainly count them on one hand. It’s just not a very big number. It’s a very difficult thing to do.”

Of course an artist would prefer to not sign with a label and become famous on their own accord without sharing profits with anyone else. That’s just not the reality of the industry, though. Labels are an integral part of promoting artists music and without their marketing and distribution know-how across the world, far fewer artists would become successful.

Distribution Moat

I like to think of distributors in two categories: middlemen who take an unnecessary cut of profits because they happen to own legacy distribution channels, or integral players in an industry that cannot be easily replaced or replicated. The latter group adds value as a whole and increases the size of the industry pie.

Initially I suspected that music labels could be compared to linear cable networks. Take CBS for example. Basically the only reason to still subscribe to linear cable is to have access to networks like CBS (you can get anything else through streaming services). For most people the primary reason to subscribe to networks like CBS is to have access to live sports as CBS has distribution rights for popular sports like the NFL and College Football. To be sure, these contracts are valuable now to CBS, but I don’t believe CBS adds much value and subsequently eventually most of the value will accrue to the NFL over time, not CBS. The network doesn’t own the football teams, cultivate talent on the football teams, or need to do much in the way of marketing for the football teams. CBS simply streams the product to your television which can be done by any number of other services, and we’re seeing a slow transition already. Amazon Prime has begun winning Thursday Night Football distribution rights and I suspect we’ll continue to see a bidding war for the commoditized product of football streaming. Ultimately I suspect more value accrues to the NFL owners than to the distributors of the content.

Music labels are much different. Most importantly, they enable artists to gain recognition who otherwise wouldn’t have become successful musicians. It’s impossible to gain access to streaming platforms and music distributors without having the scale, connections, and know-how of the music labels. This is just not something that can be recreated by individual artists or any other business. A closer analogy may be: music labels are to musicians as McKesson is to pharmaceutical companies. Pharma companies cannot profitably distribute their drugs across the country because no one pharma company is large enough to bear the costs and complexities of distribution, and therefore they have to pay the few large drug distributors to do it for them. The same logic roughly applies to artists and labels.

Additionally, consider the relative bargaining power of a label versus an individual artist. Even the most popular artist on a per-stream basis will generate a low-single-digit percentage of streams in any given year. Also, the top artists usually change every year. Universal Music Group owns more than 30% of the streams year in and year out. It’s clear who consistently will be in the best position to negotiate and distribute with the major DSP’s, and it’s not even close.

Nowadays the biggest artists in the world make most of their money from touring and live shows. It’s almost as if streaming is the top of the funnel advertising for artists to garner interest in their far more lucrative live shows. Instead of paying for that top of funnel advertising, they actually get paid a portion of the revenue generated from streaming that ultimately benefits their live tours and merchandise sales.

Finally, contrary to what I initially expected, labels are more important now for megastars than they were in decades past. This is because music has gotten so much easier and cheaper to create. As Gokgol-Kline noted in the interview with O'Shaughnessy, in 2000 there were around 1.5 million songs released. Last year the number was closer to 22 million. Spotify uploads 60,000 new songs per day. It is a daunting proposition, even for the most famous artists, to compete with 22 million songs annually. The only way to stay top of mind is with the marketing and promotional heft of the music labels.

Ultimately, I don’t see the labels as dispensable middle men who are bound to be replaced.

Catalog Moat

Another key difference in the music industry is the importance of the historical catalog versus other forms of entertainment like video.

By the time someone is in their late 20’s or early 30’s, their music taste is largely cemented and they’ll spend most of the rest of their life listening to their favorite songs. In this sense, musical content is evergreen and the importance of owning an immense historical catalog of songs is crucial. The music labels own the vast majority of modern music which is essential for streaming services. For example, I love music from the ’60’s and ‘70’s (thanks Dad) and ’m not signing up for Spotify if I can’t listen to Neil Young and Bob Dylan songs, regardless of how great the new content is. Alternatively, I don’t need Netflix to carry every show ever made to get enough value out of my subscription to make it worthwhile.

Also, people will listen to their favorite songs hundreds of times over the years, but they won’t watch their favorite TV shows hundreds of times. Constant new content creation is much more important in video than in music, and because of these dynamics, the owners of the historical catalog are in a much stronger position in music than in video.

Source: PSTH Universal Music Group Presentation (June 2021)

Another major difference between the labels and DSPs is the DSPs don’t really get operating leverage on streaming because they pay out so much of the royalty’s to the labels. They make up for this by launching podcasts and with advertising dollars, but they don’t strike me as nearly as good of businesses as the labels.

Data Moat

Data is becoming an increasingly important part of the music industry as streaming takes over. Given that the labels own the IP they have access to unprecedented amounts of performance and listener data. Enhanced data and analytics strengthens the labels marketing capabilities as well as improves their “hit rate” on predicting success for new artists. This is improving their ROI for finding and developing the next generation of stars.

To assess the importance of music labels, look no further than Taylor Swift. If any artist could have succeeded without a label, it’s Taylor Swift. She’s world famous, business savvy, and motivated to reap the rewards of her musical empire. Nevertheless Swift signed a new agreement with Universal Music Group in 2018. As Arman said, you can count the number of successful artists that are not signed to a label on one hand, and there’s a reason for that.

Growth Prospects

Streaming platforms have turned music labels effectively into annuities on the music industry. Better yet, they’re annuities that are growing rapidly.

Labels earn a cut of revenue from subscription revenue generated by DSPs. This is usually based on a percentage of streams basis. They also earn a portion of advertising dollars that the DSPs generate from non-paying users.

The main drivers in the decade ahead for music labels are growth in paid streaming subscribers, growth in non-paid users and improved monetization of ad-supported streaming services, and new areas of monetization such as gaming, connected exercise, and social media. Overall, the runway looks immense.

In paid streaming, growth is largely up to the DSPs. Platforms like Spotify will look to grow via both increased penetration in markets around the world as well as increasing pricing (ARPU). Smartphone penetration is an important driver of new users. From 2015 to 2019 smartphone penetration went from 55% to 75% in developed markets and 17% to 35% in emerging markets. Those numbers are likely to rise towards 90% and 60% respectively by 2030.

Additionally, paid streaming penetration is improving in developed markets. The Nordic region (the birthplace of Spotify) has a 43% penetration of paid streaming among smartphone owners. The U.S. is not far behind at 41%, but the rest of the developed world has only a 28% penetration. Emerging markets are a fraction of that.

The music labels stand to benefit from some of the most valuable and well capitalized companies in the world, like Apple, Amazon, and Google, in addition to Spotify, spending huge sums of money in the intervening years to grow their subscription platforms. Music is important to all of these companies as a complement to other parts of their businesses, and a high proportion of the dollars they spend to grow their streaming business will accrue to the music labels without the labels laying out much capital of their own.

Last, ARPU is likely to rise over time in every region as DSPs gradually raise prices as they reach mass adoption, much like Netflix has done. It’s entirely possible that while prices rise across regions the faster growing emerging markets whose prices start from a lower base will actually offset overall ARPU growth and global ARPU rates remain somewhat flat. Either way it’s unlikely to be a headwind.

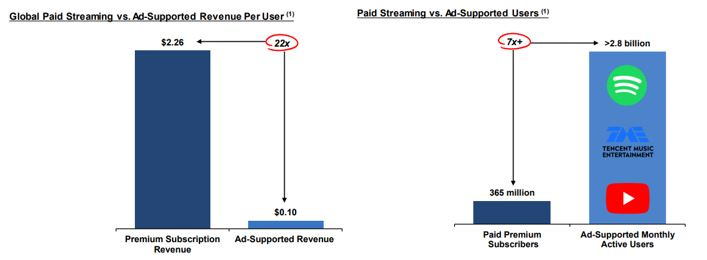

There’s a huge opportunity to better monetize ad-supported streaming. As Pershing Square highlighted when discussing their investment in UMG, the ad-supported music streaming market is both vastly larger and grossly under-monetized when compared to paid streaming subscriptions. Specifically, revenue per user is 22x higher in subscription while the user base is 7x larger in ad-supported users.

Source: PSTH Universal Music Group Presentation (June 2021)

DSPs are likely to continue to close this gap as they optimize advertising dollars across platforms which represents huge upside for both the DSPs and music labels.

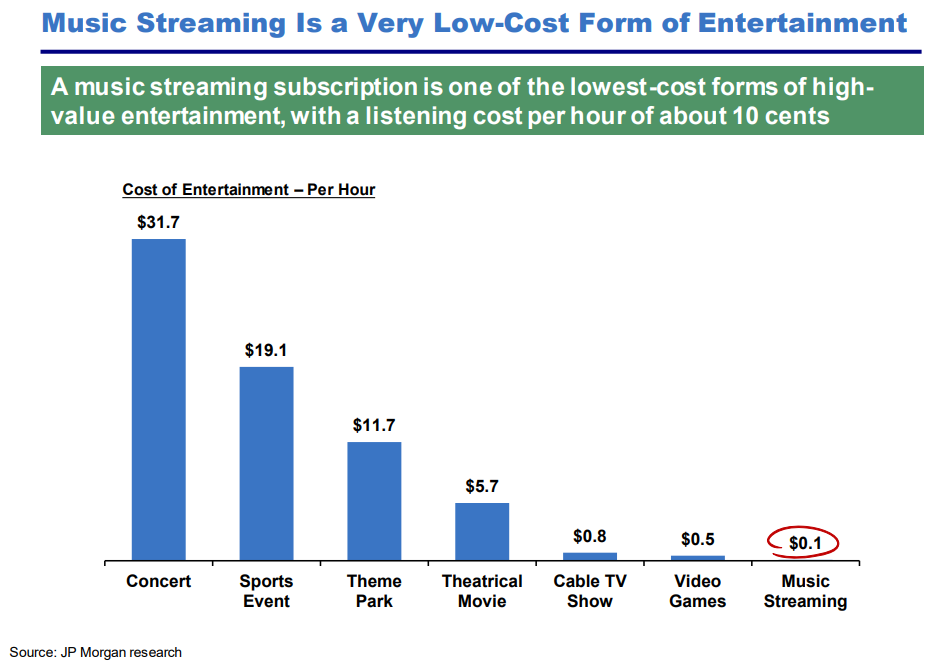

Finally, the music industry benefits from the best value proposition of any form of modern entertainment. JP Morgan research estimates that streaming costs about $0.10/hour, a fraction of most other forms of entertainment.

Source: PSTH Universal Music Group Presentation (June 2021)

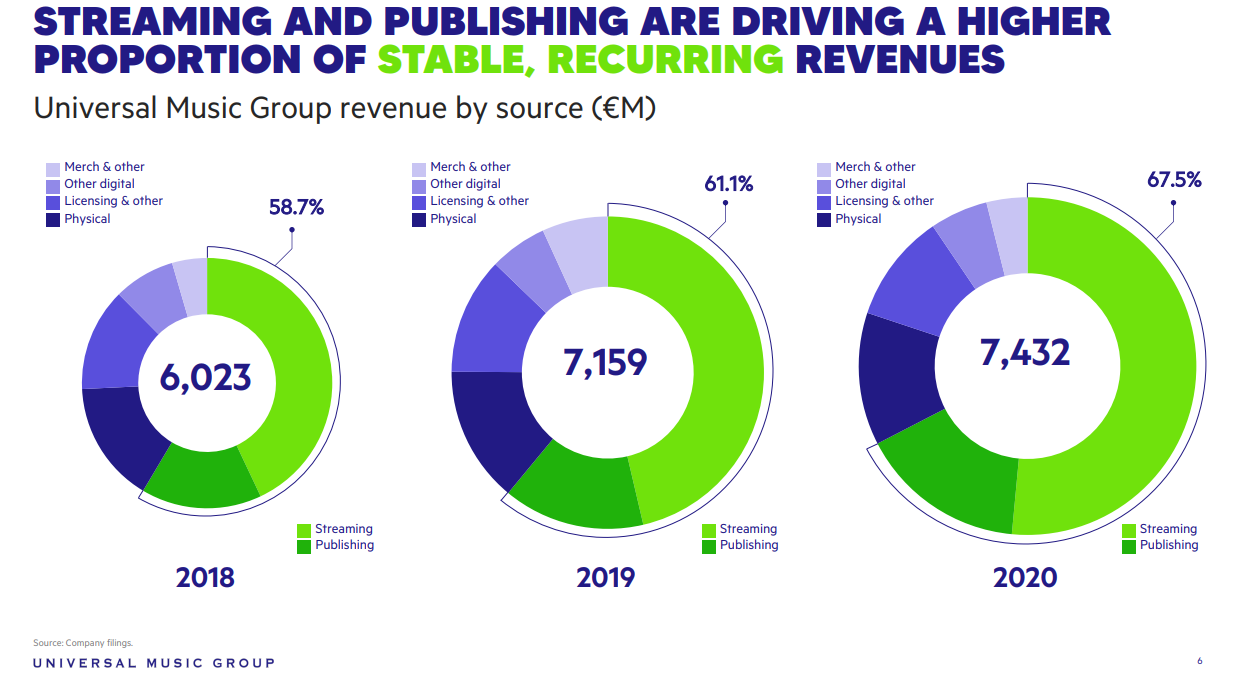

Streaming will continue to be the dominant source of profits for music labels, but they also stand to benefit from the fast-growing “other ” section which includes platforms like Peloton and video games licensing songs from their catalog. Physical sales will continue to contribute a not insignificant portion of revenue over the years, but it will become increasingly less important as streaming continues to take over. This is all good news for the labels. Below is how Universal Music Group’s revenue mix has evolved over the last few years.

Source: Company Filings

UMG, the most dominant and highest quality label, is growing at roughly a 20% clip now, a pace that I expect will continue for many years. The business is largely a toll road on the growth in streaming. As such, earnings will grow in-line with streaming industry revenues plus a little extra thanks to operating leverage given the company’s large fixed cost base.

Until last year there was no way to invest in a pure play music label. That changed when Access Industries took Warner Music Group public in October 2020, though they retain the vast majority of voting rights. French conglomerate Vivendi spun off Universal Music Group about a month ago after a failed attempt to merge with Bill Ackman’s SPAC, though Pershing Square went ahead with a 10% stake in the company through his hedge fund. Sony music is still private.

Of the three major labels, Universal appears to be in the strongest position. They are the largest by far with over 30% market share and are the undisputed market leader. Universal represents 10 out of the top 10 global artists and is led by exceptional managers. That said, all businesses sport excellent returns on equity (well more than 50%) and enjoy the same long growth runway and entrenched position.

Given the company and industry’s competitive position, huge and growing market, and large upside in monetization trends, it would appear that the duration of sustained mid-teens annual growth could stretch out a decade or longer. What’s that worth?

Valuation and Risks

Universal and Warner appear optically expensive on GAAP profits – both trade between 40x and 50x next years’ earnings estimates, or about double the S&P 500. I thought Ackman had an interesting comment on valuation during his June presentation:

“what’s fascinating to me—if you came to me and said, what would you pay to own a third of the world’s music content and an engine or a platform to identify the best artists in the world, where you can keep taking more and more market share over time? What is that business, how would that compare with, you know, Disney, which is one of the world’s great companies? Which would you rather own? What would it be worth in my mind? It seems to me it should be worth something similar. Just, just back of the envelope—well, Disney doesn’t own all the world’s content, but it’s a very, very important player in video content. Well, Universal, the price we paid is one-eighth the price, the current market cap, of Disney.”

I think Ackman is right in saying a recurring and entrenched share of 1/3rd of the music industry is worth a whole lot.

Let’s make up some numbers and say over the next 15 years Universal continues to grow earnings per share at 20% for the first five years, 15% for the next five, and 10% for the last five. It doesn’t take a lot of crazy assumptions to believe in that type of growth. Even if the stocks valuation multiple is cut in half, investors would still likely earn a low-teens annual return. I’d take that any day against what the broader market over the next 15 years. That said, the stocks are still expensive and may not have a huge margin of safety. Fortunately no one is forcing investors to buy at these prices and I’m sure the industry and individual players will run into bumps along the way providing more attractive prices for the stocks.

Risks

The few big risks, other than overpaying for one of the stocks, I can envision are:

- Why don’t DSPs act as music labels and cut out the labels?

- What happens if artists launch their own labels?

- What if regulators put a cap on the royalty cut music labels can take (there is some legislation along these lines in the UK)?

- Future unknown disruptions. No one saw streaming coming 15 years ago, and another seismic shift in the industry may not benefit the labels.

I don’t see any of these as very likely or worrying, given all of the inner workings of the industry discussed above. DSPs can’t reasonably act as music labels because the artists need access across all platforms and not a “walled garden” approach like an Apple or Spotify would presumably follow. It also takes incredible expertise, local knowledge across international markets, and decades of experience to successfully navigate the complex music industry and effectively market and distribute content. It’s not something that one of these DSPs can just decide to do and expect to out-execute a Universal or Warner.

I already covered the threat of an individual artist going out on their own. I don’t see this as realistic on any broad scale because of the benefits of scale and bargaining power that the labels have.

If regulators put a cap on the royalty cut the labels take, they’ll just respond by lowering their investments in new artists because it’s a simple risk/reward calculation for the labels. Their Venture Capital model doesn’t work if they can’t earn the returns required from the winners to compensate for the losers, and they’ll pull back their investment in the space. This would be very bad for aspiring artists and widely unpopular, in my opinion.

The last risk can be true for really any industry. The music industry will continue to migrate digitally, and it’s very hard to envision a scenario where that becomes bad for the labels.

In summary, streaming has changed the game for major music labels like Universal Music Group. These businesses operate as an oligopoly and represent a recurring, high-margin toll on the growing consumption of music and have untapped pricing power (via the DSPs) across a massive addressable market. Thanks to an impregnable competitive position, the duration of that growth may prove to be far longer than the businesses are being given credit for today. Situations like this are how seemingly expensive stocks are seen as obvious bargains when viewed in retrospect a few decades later. I’m not saying that’s what will happen with the music labels, but it wouldn’t surprise me.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.