SS&C Technologies: Baby Out With the Bathwater?

SS&C Technologies: Baby Out With the Bathwater?

Happy Thanksgiving everyone and thanks for reading!

SS&C Technologies is a vertical market software (VMS) business that provides software solutions for a host of mission-critical yet mundane front, middle, and back-end functions across the financial services and healthcare industries.

From the time SS&C IPO’d in 2010 through the end of 2021 earnings compounded at an outstanding 24% annually and the stock compounded at 23% per year. The business is still led by founder Bill Stone and enjoys a number of attractive characteristics and long-term tailwinds. SS&C has typically traded at a premium valuation but, thanks to the tough market for software and growth companies, is down roughly 40% this year and now trades at a substantial discount to its historical valuation.

Additionally, a number of investor I greatly respect including Vitaliy Katsenelson (Investment Management Associates), Francois Rochon (Giverny Capital), and Seth Klarman (Baupost Group) own meaningful positions in SS&C.

Overview

SS&C’s main customers are institutions and funds across the asset management, wealth management, brokerage, retirement, and financial advisory industry. They’re especially tied in with alternative asset managers such as private equity, venture capital, and hedge funds as well as mutual funds. SS&C sells subscriptions for software that automates front office functions such as trading and modeling for funds, middle-office functions such as portfolio management and reporting, and back-office functions such as accounting, transfer agency, compliance, regulatory services, and performance measurement. After its acquisition of Intralinks SS&C is also the leading provider of virtual data rooms used by private equity and other M&A players during transaction due diligence. They also have a small healthcare segment that provides solutions to the pharmacy industry focused on information processing, quality of care, and payment solutions. In most of its product segments SS&C is the leading software provider to the industry.

Here’s a good overview of SS&C’s broad offerings:

Source: 2021 Analyst Day

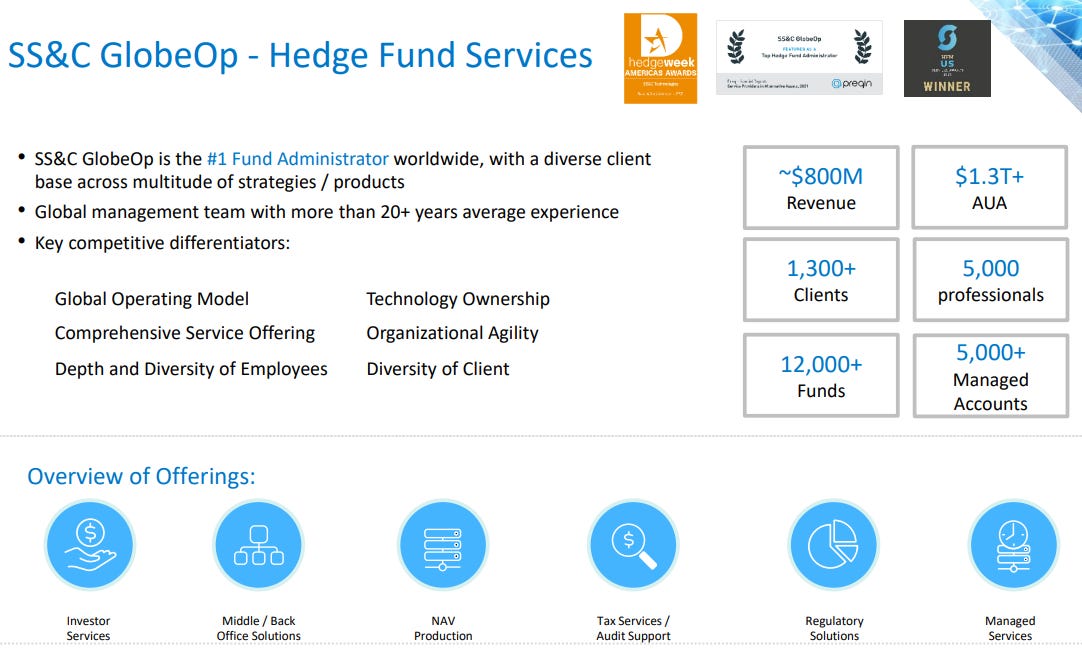

An example of one of SS&C’s main offerings is GlobeOp, the #1 fund administrator for hedge funds across the world. GlobeOp serves over 1,300 clients who manage more than $1.3 trillion dollars and provides software for virtually any business function from investor interface to tax accounting.

Source: 2022 Needham Growth Conference

Another major business line is Global Investor and Distribution Services (GIDS) which provides information processing and servicing for mutual funds and large financial institutions. Again SS&C owns the top position in the US and UK in this market.

Source: 2022 Needham Growth Conference

The common theme in each segment is a scaled #1 market position and deeply imbedded, long-standing client relationships.

The way I think about SS&C is that they aim to automate, or otherwise make easier, any part of the job that is non-core to the overall value proposition. Their software lets portfolio managers spend more time and money on research and portfolio management and less on reconciliation, reporting, and fund accounting.

The company has built this formidable array of offerings via significant inorganic growth since its founding in 1986. Since 1995 the company has acquired 59 businesses of widely varying sizes.

Business Model Characteristics

SS&C offers many of the things I look for in a business, such as:

High quality and predictable revenue streams thanks to high customer switching costs;

Pricing power;

Significant free cash flow generation due to low fixed capital requirements;

High and increasing returns on tangible equity;

Owner-oriented and high-quality management with skin in the game;

Clearly stated and rational capital allocation policies (although the serial acquisition aspect is the hardest part to get comfortable with for me, more on that later).

Revenue Quality

SS&C’s software solutions benefit from high switching costs; one of my favorite moats and one that is very common in the VMS industry.

Once a financial institution migrates to SS&C’s software, it’s unlikely to lose that customer simply because it’s a pain in the ass to switch back-office software that has a high cost of failure. SS&C’s software works well as they’ve spent decades building expertise in their circle of competence, and unless an offering comes along that is far superior to SS&C’s, it’s not worth the risk of switching. In the financial services world, once an institution has selected a software that touches anything related to things like compliance, client-reporting, or back-end accounting there is very little reason to look at alternate solutions given the importance of these functions and the issues that could arise should a new solution incur problems.

Additionally, SS&C is the world’s largest mutual fund transfer agent. A transfer agent is an institution that maintains financial records, tracks account balances, records transactions, cancels and issues certificates and handles a variety of other services relating to investor’s account balances and certificates of security ownership. To put it simply, this is stuff that cannot be screwed up and SS&C has a leading position and expertise in not screwing it up, meaning their top position is unlikely to change. This is the theme across segments.

Significant switching costs are evidenced by high revenue retention rates. The company aims for 95%+ revenue retention and consistently delivers at or above that level. Sticky customers also confer the coveted pricing power.

SS&C is increasingly pushing price to offset wage and other inflation. As CEO Bill Stone put it on the most recent earnings call:

“I think we've had a program to get some price increases, and that's worked pretty well. And I think it's -- the price increases are more substantial than they have been over the last probably even 5 years as, obviously, inflation has gone up and people recognize that they want to keep the same team. We have very talented people, and they want to keep the same team.

So the conversation, while no one likes to have their prices increased, they understand that to keep these talented people and continue to deliver service at a very high level, there's going to be some price increases. And we've had, I would say, pretty good success with that.”

Further, they’re not only including CPI escalators as standard practice in new contracts, but also implementing escalators in existing contracts. President and COO Rahul Kanwar explained:

“we are obviously making that a standard in new customer contracts. But as part of the conversation with current customers that did not have escalators in their contract, we're both agreeing to updated price levels at the present and also sort of having this regimen of CPI or something indexed to a cost of living type adjustment built into the contract. And that also has -- to Bill's point, nobody really wants to talk about these things, but they understand where we're coming from. And so that's gone reasonably well. And it does make for, as you point out, a more automatic and consistent process going forward.”

It is no small feat to go back to an existing customer contract and amend it to include price increases, and it’s a testament to SS&C’s competitive position and price vs. value proposition.

Finally, most of SS&C’s revenue is sold as a subscription or tied to customers assets under management (AUM) and transaction volumes, meaning revenue and profitability is highly scalable and predictable over long periods of time.

There is a reason investors typically pay such rich multiples of earnings for VMS businesses; long duration and sticky customer revenue is worth a whole lot of money.

Capital Allocation

SS&C is a serial acquirer of complementary software companies to the tune of nearly 60 acquisitions since 1995. Here are the notable acquisitions since 2010:

Source: 2021 10K

The biggest deals, by far, have been GlobeOp, DST, Eze, and Intralinks which ranged from $800M - $5.4B.

So far, Bill Stone and the management team have a solid track record of buying companies within their circle of competence and paying prices that, at least so far, have created significant value for shareholders. Given the size of some of these deals, it has also required a lot of debt, however. Since the company went public in 2010 SS&C has retained ~200% of operating cash flow, most of it going to the above acquisitions at low double-digit incremental returns for ~20% compounding of intrinsic value. It’s early days on the more recent large acquisitions as well, so I expect the lifetime returns on these to be far better than the ~10% I’ve penciled in above as their contributions to operating cash flow growth will only grow over time with very little incremental capital needed.

This approach to inorganic growth is both an opportunity and a risk. The biggest risk with companies that have relied on acquisitions to drive growth is that eventually they a) run out of attractive acquisition opportunities and growth (along with the valuation multiple of the stock) contracts rapidly or b) they overpay for a big acquisition that turns out to be value-destructive for shareholders.

The best guard rails against these pitfalls for a business that makes chunky capital allocation decisions is ensuring that management’s incentives are aligned with shareholders and that they operate with significant skin in the game.

On incentives it’s a bit of a mixed bag. According to the company’s proxy, SS&C’s executive’s annual cash bonus is based off of some sensible targets (recurring revenue, free cash flow) and some that I don’t like (EBITDA, revenue growth). Performance based equity awards have a sensible metric of 3-year average earnings per share growth. I would prefer to see some ROIC metric given how much capital management deploys, but nothing is egregiously wrong with the incentive structure. Skin in the game is a very different story.

The executives at SS&C own boatloads of stock. CEO Bill Stone owns 13.5% of SS&C’s stock, which equates to roughly $1.7B at recent prices. COO Rahul Kanwar owns $83 million worth of stock. CFO Patrick Pedonti owns $24 million. Board member and recently retired employee Normand Boulanger owns $60 million of stock.

In my mind the amount of insider ownership at SS&C swamps the mixed bag of incentives. There’s no way to guarantee a business’s executives will be good stewards of shareholder capital, but there’s no better way to guard against misappropriation of shareholder funds than an aligned management team with their net worth tied up alongside shareholders’. Zuckerberg is doing his best to disprove my point on this recently at Meta, but I digress.

It looks like no big acquisitions are in the plans for the time being. In Q3 management stated that they intend to use 50% of free cash flow for share repurchases and 50% for paying down debt. With the stock trading at what appears to be an attractive valuation, this is a wise approach.

Forward Returns and Valuation

SS&C has delivered tremendous growth in earnings per share over the last decade plus. As noted, a lot of this growth is thanks to a handful of large acquisitions. Smaller tuck-in acquisitions are almost sure to continue, but those are unlikely to move the needle at SS&C’s present size. I have no insight as to if or when SS&C will bag another elephant, so I’ll only evaluate organic growth opportunities from its existing business segments.

Given the client base, SS&C’s business is tied in large part to growth in the alternative asset management space like private equity, venture capital, and hedge funds. SS&C earns revenue based on both assets under management of its clients and number of transactions. Both drivers seem likely to rise over time.

Since the financial crisis institutional investors such as endowments and pension funds have increasingly looked to alternative investments to generate returns in a low interest rate environment. This has been great for SS&C’s business. With rates finally starting to normalize, maybe the rush into alternatives slows or reverses somewhat for a period of time, but I don’t see any signs pointing towards a massive drop off in AUM in the space. Most indicators point towards investments in alternatives actually growing handsomely in the years ahead.

Analytics firm Preqin recently published a biannual report that projects the global market for alternative investments will nearly double by 2027 to over $18 trillion. From 2015-2021 the alternatives market grew at 14.9% and Preqin is forecasting roughly 12% growth over the next five years. While institutions drove much of the growth in recent years, retail investors are likely to contribute meaningfully to the next leg of growth. Asset managers are increasingly providing new ways for retail investors to allocate money to alternatives, which have historically been reserved for institutions or ultra-high net worth individuals. Institutions are unlikely to pare back investments in the space as alternatives have carved out a resilient allocation in institutional investment managers portfolios.

Additionally, transaction volumes appear likely to continue rising as interest in financial markets seems to only grow over time. Every financial transaction needs to be recorded and many of SS&C’s offerings are tied to these volumes.

Bill Stone discussed the resiliency of SS&C’s revenue on the Q3 call:

“if you look at our historical range on fund administration growth, it's somewhere between 4% and 8%, 9%. And so when we have tough markets like this, we expect to be at the lower end of that range, but I wouldn't expect us to get negative unless there was a dramatic change in macroeconomic outlook.”

While many other businesses who essentially earn a royalty on AUM in public markets (like T. Rowe Price) necessarily have to endure periods of declining AUM when stock markets fall, SS&C’s exposure to the alternative asset space means its revenue is incredibly resilient. 2022 is an excellent demonstration of this as funds under administration should grow around 4 or 5% even though public markets are down nearly 20%.

SS&C also has meaningful opportunities to cross sell technology solutions to a sticky existing customer base. The company points out in the 10K that “many of our current clients use our products for a relatively small portion of their total funds and investment vehicles under management, which provides us with a significant opportunity to sell additional solutions to our existing clients and drive future revenue growth at a lower cost”. Like many SaaS businesses, there is a long runway for growth here.

Let’s say conservatively SS&C only grows revenues organically between 5-6% annually over the next five years. The business targets at least 50 bps of margin expansion annually thanks to the low capital intensity of the software business model. So, overall profits should grow around 6-7%. With 50% of capital being used to repurchase shares at recent prices per share free cash flow growth should be at least 10-12%. The company also pays a 1.6% dividend taking annual expected business returns into the low-teens. What are investors paying for this expected return? A lot less than usual.

SS&C has historically traded around 18x earnings. It appears the baby has been thrown out with the bathwater in 2022 and SS&C now trades at a hair under 11x earnings (or free cash flow, including stock comp). It trades at just 6.5x Value Line’s estimate of free cash over the next 3-5 years.

SS&C is certainly an above-average business which has warranted its historical above-average multiple. If, over the next five years, SS&C re-rates back to its historical (and fair, in my opinion) 18x multiple it would add another ~10% per year to the stock returns, taking total annual returns to the low-20s. Not bad.

Bill Stone agrees the stock looks undervalued at present. When responding to capital allocation priorities, clearly he plans to keep buying in shares:

“we view our stock as undervalued, you get kind of a -- anything you do is pretty positive. But interest rates at 5.5% compared to stock price at $50, the stock price at $50 is quite a bit financially better.”

Summary

SS&C checks a lot of boxes. The business enjoys a highly profitable, predictable revenue stream from an entrenched customer base thanks to its leading market position and mission critical services. The business is capital light with pricing power and a long growth runway. The stock is trading at an undemanding valuation due to a misunderstanding of the business model and overall negative sentiment towards software and growth stocks. Finally, management operates the business with shareholders in mind because they are significant owners of the stock and are taking advantage of the recent drop in valuation to reward continuing shareholders with opportunistic share repurchases.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. You can also find more information on our website. We recommend starting with Fundamentals. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

Great post.

I am curious to know why you ignored the debt in the valuation. EV/FCF is around 20. I'd argue that it's slightly overvalued for something growing at 5-6%.

No doubt about the moat but would you buy the whole business for $20 billion (including debt) in exchange for recurring FCF of $1 billion growing at 5-6%?