Seagate Technology, Western Digital, and the Hard Disc Drive Industry

The hard disk drive (HDD) industry was written off as doomed a few years ago as laptops and PCs switched to faster solid state drive (SSD) storage options. Recently, the industry has been revived by a torrent of spending on data centers that utilize HDDs en masse.

The industry is a duopoly occupied by Seagate and Western Digital who command around 85% of the market. Both stocks look cheap and Seagate is repurchasing its shares hand over fist while Western Digital grapples with a newly launched activist campaign from the most feared of activist firms – Elliot Management. Basically, no shortage of drama and intrigue for nerdy investors in a formerly boring sector!

Digital Storage Industry Background

Data can be stored in a few ways with HDD and SSD (or flash) being the main options. Hard disk drives are just what they sound like, disks that spin around and digitally encode data. If you have an older computer and you hear it “whir”, that’s probably the disk drive spinning. Solid state drives are a method of storage that uses integrated circuits to store data via moving electrons around instead of physically writing the data to a disk.

There are puts and takes for each method of storage, but overall SSDs are higher performing – faster, more reliable, and less apt to damage – than HDDs. The big advantage for HDDs has been, and remains, a much lower cost.

Source: Avast.com

Up until the mid-2010’s HDDs were the method of choice for storage. As prices for SSDs came down they overtook HDDs for most applications. Gaming or downloading movies is way faster on a laptop with an SSD than an HDD and the cost difference isn’t dramatic for a $1,200 device. In data centers, on the other hand, the name of the game is maximizing storage data per dollar spent. Because HDDs are somewhere around 2.5x less expensive per TB of data stored, they’ve found a home in the buildout of data centers led by cloud computing giants. Thanks to the tailwind of data center spending in the U.S. and a brief uptick in spending on work from home related items during the pandemic, the industry has returned to growth.

Source: Western Digital 2022 Investor Day

Storage solutions are a commodity business so industry structure is important. The HDD industry is a duopoly with two apparently rational players. Seagate commands close to half of the market and is a pure play HDD company (90%+ of revenue) while Western Digital produces both HDD and SSD products (about 50% of revenues from each) thanks to its $17B acquisition of SanDisk in 2015. Much more on that later.

Source: Elliot Management Letter to Western Digital Board

The SSD industry is more fragmented with no pure-play companies.

Fundamentals

As Seagate is the only business solely focused on producing HDDs, it is most instructive to study their financial performance for an indication of the attractiveness of the industry. For a “dying” industry, the economics have been excellent.

As is often the case in rational oligopolistic industries, returns on capital are superb. Since 2010, returns on capital have averaged 27%, with only one year (2016) averaging less than 21%. Returns on equity have consistently exceeded 100%. Why the high returns?

Enviable returns on capital are usually fleeting because competition will enter a market with high returns and compete those returns down to a more normal level. Seagate benefits from a few factors.

First, because of the longer term uncertainty for HDD demand, new competitors haven’t entered the space. In fact, the lone other major player, Samsung, sold its HDD division to Seagate in 2010 to focus on other segments. Second, Seagate and Western have immense relative scale advantages compared to any potential entrants. Both companies have been around for 50+ years and have amassed a major production cost advantage thanks to economies of scale. Finally, both businesses have remained relatively rational in terms of pricing strategies and other competitive dynamics.

Bruce Greenwald writes about a shorthand way to estimate barriers to entry for an industry to help assess whether or not potential competitive advantages exist. He uses market share and returns on capital. If market share is stable among the big players and returns on capital are consistently abnormally high (think 20%+), there is a good chance high barriers to entry exist. The HDD industry checks both boxes.

With no new entrants likely thanks to the above factors, as long as HDDs are around it looks like Seagate and Western Digital are going to dominate. So far, the businesses looks like a slam dunk, but of course it’s never that easy. The question is, how long will HDDs be around?

Risks

Unfortunately, I don’t have any unique insights in terms of how long HDDs will be in high demand for data center buildouts while also playing a part in legacy applications. By all accounts, cloud and data center spending has a long runway, especially outside the U.S. where the industry is more nascent.

HDDs are clearly superior from a cost perspective which is the primary factor keeping the technology relevant. That advantage may not last forever though. Seagate predicts HDDs will have a cost advantage over SSDs well into the 2030s. I have no idea if that’s correct and considering the source, any long-range predictions should be viewed with a healthy dose of skepticism. Still, given what is actually occurring – consistent and growing spending on HDDs – it seems unlikely that demand suddenly crashes. Certainly for the next several years, at a minimum, demand seems likely to persist.

Nonetheless, hints of a cliff risk are present and investors have to grapple with whether or not the price of the stocks compensates for a potential judgement day for HDDs sometime in the next decade or two. Also, new technology could arise in the coming years at a more compelling price point than either SSDs or HDDs and inflict major harm on the industry. I don’t understand the technology well enough to opine on the likelihood of that happening, but it doesn’t seem impossible.

Capital Allocation

While the HDD market turning around over the past several years has been great for both Seagate and Western Digital, capital allocation has been dramatically different at the two businesses. Subsequently, returns to shareholders have diverged.

Despite the same exposure to the same end market, over the past five years, Seagate’s stock has returned over 80% (not including dividends), notably better than the S&P, while Western Digital has lost about 40% of its value. Over the last ten years Seagate is up 170% and Western Digital is up about 50%. What gives?

Seagate has long had a simple capital allocation policy; use any excess cash not needed in the business to repurchase shares. Shares outstanding have dropped 6% annually, or 60% in total, since 2006. With the business perpetually valued at less than 10x earnings, this has been an excellent use of excess capital and a major tailwind for per share returns. The company has also been laser focused on executing in the area in which it’s the leader; hard disk drives. They own half the market and earn very attractive returns on capital in this niche, all of which has worked out well for shareholders.

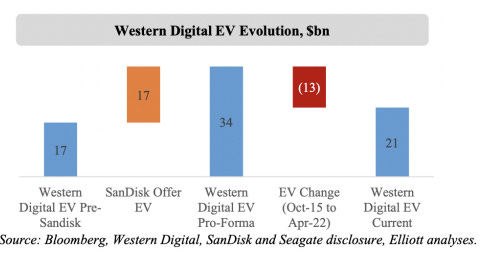

Contrast this with Western Digital which, fearing a long-term HDD demand decline, spent $17B to acquire SSD producer SanDisk in 2015. The move made sense to diversify against tail risk for the business, but in practice has not worked out for shareholders, at least so far. So far it appears the company would have nearly been better off lighting that $17B on fire, let alone returning it to shareholders like Seagate has done. To date, the SanDisk acquisition has destroyed about $13B of Enterprise Value. Ouch.

The company touted synergies with its existing HDD business, which never came to pass. This is no surprise given that the two products use totally different production processes and offer little cross selling opportunities, not to mention the dismal track record of large acquisitions across every industry. Customers buying HDDs don’t care if they’re buying SSDs from the same company or someone else. The SSD space is much more competitive and as a result returns on capital are far lower than in HDDs. It should come as no surprise that Elliot Management has taken note of the striking difference in results between Seagate and Western Digital.

Activist Involvement in Western Digital

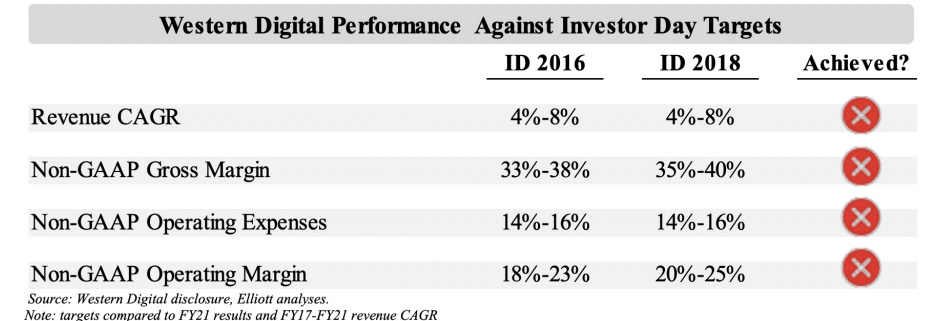

Just last week Elliot released a public letter to Western Digital’s board demanding steps be taken to close the performance gap with Seagate. As shown below, the acquisition whiffed on every goal that Western Digital laid out right after consummating the acquisition.

Source: Elliot Letter to Western Digital Management

Elliot wants to undue the SanDisk acquisition by spinning off the SSD business so each company can operate independently and focus on its respective market. Elliot believes each business will be valued higher by the market and the combined share price should roughly double to reach fair value. It’s hard to argue with the logic. If the HDD business is valued in-line with Seagate and the SSD (or NAND as Elliot labels it) segment valued in line with its peers, the stock would fetch a substantially higher price before considering future growth. Here’s a summary of the valuation. You can see the letter for the gory details, but the assumptions are reasonable.

Source: Elliot Letter to Western Digital Board

Valuation/Outlook

Clearly Elliot sees substantial upside in Western Digital, and it doesn’t take any heroic assumptions to believe they’re right. Seagate, despite being valued higher than Western Digital, looks like a reasonable bet in its own right.

Both Seagate and Western Digital believe that enterprise cloud spending on HDDs should grow handsomely for the next 5+ years. On the most recent earnings call, Seagate stated that mass storage revenue should double over the next five years:

“From my perspective… CY '23 will continue to grow in exabytes, and we're on a trajectory here in 5-plus years to double the revenue out of mass capacity. And our products are staged really well for that. So the discussions -- over the long-term discussions that we're having with everybody, again, everyone going through temporal problems right now in supply chain, but the long-term discussions are quite favorable for us.”

With the legacy PC business in steady decline, overall revenues ought to at least grow mid/high-single-digits for the foreseeable future, if not faster. In this scenario earnings are likely to grow at above 10% annually thanks to operating leverage. If Seagate continues to repurchase 5-6% of shares per year, earnings per share could easily grow at 15% or more for several years. The company also pays a ~3% dividend, further enhancing per share returns. A re-rating in the stock to a still modest 12-13x earnings would provide further upside.

Thanks to the murky long-term future of HDDs, Seagate’s stock is perpetually cheap. At recent prices, Seagate trades for just 8.5x this year’s estimate of free cash flow. Because of this discounted valuation buybacks are highly accretive. Seagate investors should be happy that the shares trade here as long as the business executes. At a minimum, not much success is being priced into the company’s stock at present.

It will be interesting to watch the Western Digital saga unfold with Elliot. If Elliot’s track record is any indication, they are likely to get what they want.

I can see both businesses and their respective stocks doing very well over the coming years, but as always it doesn’t come without risks. Seagate’s stock remains cheap for a reason, as the market worries about terminal risks to HDD demand. It’s a dynamic I have a hard time handicapping, as I’m no expert in storage technology or trends in cloud data center buildouts. I’d certainly lean towards the next 5-10 years looking similar to the last 5 years, driving attractive business returns for Seagate and Western Digital. I can’t help but wonder how quickly demand could fall off should SSD’s (or some other storage technology) overtake HDD’s long-held cost advantage. There’s always the chance that these businesses took the staircase up only to take the elevator down, and it’s something prospective investors need to consider carefully.

The contrast between Seagate and Western Digital provides some valuable lessons. These businesses are virtually identical in terms of the HDD segment. Seagate has executed with focus and thoughtfully returned capital to shareholders, leading to extreme disparity in both its business and stock performance. It is important to remember, even in a duopoly where high returns on capital are available, capital allocation matters greatly.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.