Pershing Square U.S. and Pershing Square Inc. Dual Listings

Ackman is at it again.

Whether it was experimenting with unique SPAC structures in 2020, becoming deeply involved in geopolitics (particularly on twitter) in 2024, taking over Howard Hughes to turn into his version of Berkshire Hathaway, or attempting to raise a new large closed end fund, it’s proven hard for Bill Ackman to sit still and just focus on his portfolio. This week he announced a very unique idea to revive a previously failed U.S.-listed closed end fund.

On March 10th Ackman outlined a plan to complete a dual IPO for Pershing Square U.S. (his long-sought closed end fund) and Pershing Square Inc. (the management company for all of his funds). Ackman has had perhaps the most influence of any investor on the characteristics we look for in businesses - though how we apply them is often vastly different than how Pershing Square applies them - so I can’t help but dig in whenever he comes out with a new offering.

Ackman has long dreamed of raising a huge sum of permanent capital in one shot; hence his plans to start a closed-end fund listed in the U.S. To say it’s hard to raise a publicly traded closed end fund nowadays is an understatement. Publicly listed closed end funds nowadays almost always trade at a discount to their underlying NAV. This is a big problem when trying to seed raise capital. With the rise of ETFs and open end fund structures, no one wants to lock up capital at one price only to see it trade at a discount days later and have no recourse to redeem their shares at par. For those that aren’t up to speed on the background, I can’t summarize the lead-in to this situation better than Matt Levine’s Bill Ackman Wants Your Money Again article from earlier this week:

“In 2024, Bill Ackman came to the stock market with a proposition: You could give him $50, and he would invest about $49 of it in some stocks for you. (The other $1 would go to underwriting fees.[1]) This is called a “closed-end fund,” and Ackman’s is called Pershing Square USA Ltd., or “PSUS.”

How much is that proposition worth? How much should you pay for $49 worth of stocks selected for you by Bill Ackman? Some possible answers include:

$49, because $49 worth of stocks is worth $49;

less than $49, because Ackman will charge you fees for picking the stocks, which will reduce the value of your stake over time[2]; or

more than $49, because Bill Ackman is good at picking stocks and will pick ones that go up more than the average stock.[3]

Ackman obviously argued for “more than $49,” because he is quite confident in his ability to pick the stocks that go up. Others disagreed. Closed-end funds often trade at a discount to net asset value (i.e., less than $49), so it would not be unreasonable to worry that Ackman’s would also trade at a discount. In fact Ackman already has a closed-end fund in Europe, called Pershing Square Holdings Ltd., and it trades at a discount, so.

This is a big problem when it comes to raising money. If Bill Ackman comes to you and says “give me $50 to buy $49 worth of stocks,” and you think that proposition is worth $52, you give him the $50 and everything is great. But if you think that proposition is worth $47, there’s a problem. You can’t give him $47 to buy $49 worth of stocks: Where would he get the other $2? (He could just buy $46 of stocks for you, but that’s not worth $47 — that’s worth like $43. Etc.) Ackman can only raise new money from people who think that his fund is worth more than net asset value; he can only get this started by selling shares at a premium.

Anyway this didn’t work. Ackman set out to raise something like $25 billion for Pershing Square USA, cut that back to $2.5 billion, and ultimately raised $0. Oops.”

The Pershing Square team went back to the drawing after 2024’s flopped fundraise and came up with a new idea. Instead of asking investors to invest in a closed end fund at NAV and explaining all the reasons why their fund won’t trade at a large discount to NAV like the other closed end funds, Ackman is going to give investors who invest in Pershing Square U.S. (PSUS, the closed end fund) shares in his management company, Pershing Square Inc (PSI). I have to admit, this is pretty creative and I can’t wait to see how it unfolds.

Here’s how it will work; for every 100 shares that IPO investors invest in PSUS they will receive 20 shares in PSI. The larger the fundraise for PSUS, the more management fees that will go to PSI and the more benefit the IPO investors will receive, making the deal somewhat reflexive.

Pershing Square Inc. is a fantastic business for its owners. Look no further than Ackman’s comp from last year; he made $142.8 million and his lieutenant, 40-year-old Ryan Israel, made $44 million. The management company is an asset-lite business that has rapidly compounded it’s earnings power over the last several years thanks to solid returns from the flagship fund.

Receiving shares in a fantastic business is always worth considering, the question is at what price are investors receiving these “bonus” shares in PSI, and will that make up the difference in value if and when PSUS trades at a discount to NAV? As usual, the intricacies of this Ackman deal are numerous and it’s not light on complexity. Before exploring the math behind the deal, let’s look at the rationale and structure.

IPO Rationale

In a letter to investors, Ackman explained that the best investments:

“are simple, predictable, and free-cash-flow-generative. They have impenetrable ‘moats’ or large barriers to entry protecting them from disruption, a growing risk in a world in the midst of massive technological change. They are often asset-light, and generate recurring and rapidly growing, inflation-protected, free cash flows that do not need to be reinvested in the business for the company to grow. They do not need large amounts of leverage to generate high returns on capital. And they have limited exposure to extrinsic threats outside of the control of the company… In this combined offering, along with your investment in Pershing Square USA, Ltd. (PSUS), we are providing you with an interest in Pershing Square Inc. (PSI), an alternative asset management firm that we believe meets all of the above criteria.”

He goes on to outline why it makes sense to offer shares in his business:

“PSI will become a publicly listed company concurrently with the PSUS IPO, and will trade on the New York Stock Exchange along with PSUS. By providing an extra incentive to invest in the PSUS IPO, the distribution of PSI shares to PSUS IPO investors should help us to execute a large-scale, successful PSUS IPO. A highly successful, large-scale PSUS IPO will make PSI more valuable by materially increasing PSI’s fee-paying assets under management (AUM), revenues, and cash flows. The larger the PSUS IPO, the more valuable the bonus shares of PSI you will receive.”

Basically, Pershing Square is offering shares in its lucrative management business in hopes that the shares of PSI more than offset the discount that PSUS might trade at after it IPOs and to induce investors to put as much capital as possible into PSUS because their PSI shares will benefit from the increased AUM at PSUS. Later we’ll look at what valuation PSI needs to achieve vs. what discount PSUS could trade at for this deal to make sense.

Pershing Square Inc.

Ackman believes PSI should achieve a premium valuation in the public markets. Pershing Square does enjoy a durable competitive advantage thanks to its largely permanent capital structure. Roughly 96% of Pershing’s capital is non-redeemable, the majority of which is housed in Pershing Square Holdings, a European listed closed end funds (that happens to trade at a large discount to NAV).

Competing against investment firms that offer daily, monthly, or quarterly liquidity is a major advantage for long-term investors as the investment managers do not need to acquiesce to short term performance mandates and can instead invest with an eye on optimizing long-term returns. I fully agree with Ackman that this represents a real advantage over time.

In addition, the permanent capital nature of Pershing Square in theory means they do not need to dedicate undue resources to fundraising – except apparently this one time when raising PSUS. Most alternative asset managers like KKR, Apollo, Brookfield, etc. manage long-term capital but it is usually held in fund structures that have finite life cycles and the capital ultimately needs to be returned to investors. This means that growth for these businesses depends in large part on the managers ability to continually raise capital in order to grow their fee-bearing AUM. They have, however, had no problems to date raising capital at an ever-increasing rate.

In his investor letter Ackman writes:

“If PSI never launches a new fund nor raises a dollar of new capital but continues to generate strong investment returns, PSI’s revenues, cash flows, and intrinsic value will grow at a rapid rate. The substantial majority of the cash flow that PSI generates can be returned to shareholders as our business model requires limited capital for reinvestment. PSI is one of the rare businesses that can grow at a high rate while returning the substantial majority of its capital to shareholders.”

While I agree that PSIs permanent capital is highly desirable and enables to them grow without raising new capital, there are puts and takes to PSI’s model.

On the positive side, PSI charges a management fee on an asset base that generally goes up as they earn investment returns (assuming they do a good job, which they largely have). This is great. They also earn performance fees on mark-to-market performance, which is common for public investors and is also great. Alternative asset managers usually don’t earn performance fees until assets are actually sold, making carried interest inherently lumpy and difficult to value for public markets investors.

On the flip side, other alternative managers mostly play in the private markets and charge management fees on a more stable equity value. PSI’s management fees can easily decline 20-30% in a year (right now Ackmans flagship fund is down ~15% this year, and management fees are down commensurately). Alternative asset managers don’t have this problem; it’s almost inconceivable to imagine KKR or Brookfield’s management fees compressing at all, let alone dramatically.

The last point Ackman highlights is PSI’s operating efficiency. Because the firm manages a concentrated public portfolio they do not need scores of employees. Unlike private alternative managers who wholly own and operate businesses – which takes tremendous manpower – PSI enjoys one of the highest ratios of fee paying assets to investment professionals in the industry.

This high assets-to-employees ratio allows PSI to recruit and retain very high quality talent because they can pay a boatload. This is undoubtedly another advantage PSI should enjoy for years to come.

There are puts and takes to both models, and at the end of the day they are both exceptional business models, so it probably isn’t worth splitting hairs. PSI is a great business as are the other alternative asset managers.

Structure

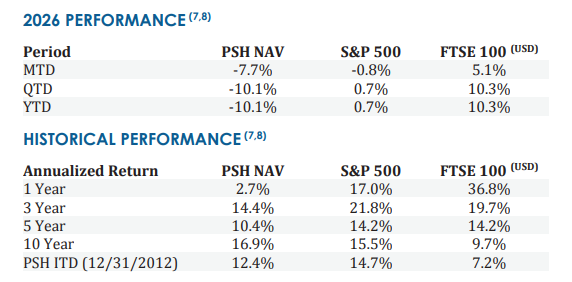

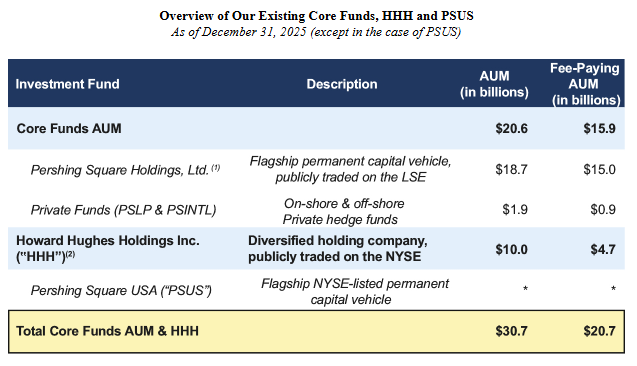

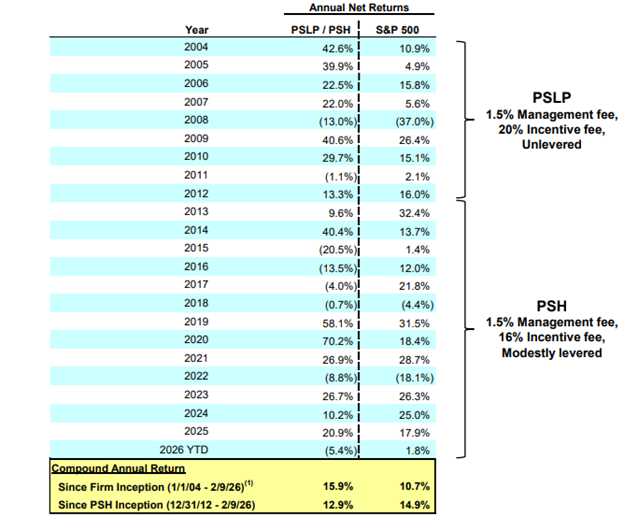

Pershing Square Inc. earns fees a few different ways, all of which will impact shareholders once the stock IPOs. In 2025 about 30% of the revenue was from fixed management fees. Most of this is from the 1.5% fixed fee they charge on Pershing Square Holdings (PSH). PSH is a closed end fund that trades in Europe and manages about $17 billion.

The fund has generated solid returns with a 16.9% annual NAV return over the past 10 years and 12.4% since inception (12/31/2012). Ackman went through a brutal stretch from 2015 – 2018 when his large investment in Valeant tanked at the same time his short position in Herbalife went way against him. He righted the ship and has done well since then and has an excellent long-term track record, though the fund is down substantially this year.

Two other small private funds make up another couple billion of AUM and earn fixed fees.

The real upside to Ackman and team comes through performance fees. They earn a 16% performance allocation from their existing funds. The kicker is there is no hurdle rate, just a high-water mark, so 16% of all gains above the fund’s previous high watermark go to PSI. Performance fees made up 55% and 70% of PSI’s revenue in 2024 and 2025, respectively. PSUS will not charge a performance fee and will only have a 2% fixed management fee due to regulations in the U.S.

There are a few weird aspects of how these fees will be split with shareholders post-IPO.

Once PSI goes public, the performance fees from PSH will be split between shareholders and employees. The performance fees from the first 5% net returns will belong to shareholders – these are referred to as “Preferred Performance Fees”. Let’s say the fund returns 10%; common equity holders will receive 16% of the first 5% of returns. If the starting asset base for performance fees is $15B then the Preferred Performance Fee would be $15B x 5% x 16% = $120 million.

Anything above this threshold will go to employees and be called “Subordinated Performance Fees”. This is pretty weird. Ackman is doing this for a few reasons.

First, the public markets tend to discount performance fees when valuing investment managers. As we’ve written about, Brookfield’s carried interest is likely to be sizeable and very important to shareholders, but the market hardly incorporates any carried interest into BN’s valuation because it’s lumpy and hard to predict. Ackman’s goal is that analysts will more easily be able to value the preferred performance fee stream because most years it’s likely to be earned given the fund just needs to return 5%. So, instead of discounting this fee stream Ackman is hoping the market ascribes a higher multiple to these fees.

Next, he explains that PSI needs to keep plenty of upside to entice his team to stay at the firm. He argues that by keeping the upside beyond a 5% return he won’t have to issue equity to employees and public shareholders won’t be diluted. I mean, I get it, but it sure seems like employees are keeping a lot of the upside for a public company.

The final weird element to PSI is the relationship to Howard Hughes (HHH). To make a long story short, Pershing Square took majority control of HHH last year and has turned it into another perpetual capital fee-paying vehicle. Ackman intends to try to turn HHH into his mini Berkshire and has already agreed to acquire an insurance business. Howard Hughes pays PSI an annual $15 million management fee along with an annual percentage of the market cap compared to a baseline; another highly favorable fee arrangement for PSI.

Once PSUS goes public PSI will have another long-term $100 million+ high margin fee stream without adding any material incremental expenses.

Valuation / Prospective Returns

There are two questions that really matter for IPO investors; what is the “bonus” stake in PSI worth and at how big of a discount to NAV will PSUS trade? Obviously I don’t know the answers to these questions but we can make some educated guesses.

As to the first question; Pershing Square sold 10% of PSI in 2024 in a private transaction that valued the firm at about $10B. Is this realistic?

Asset managers are usually valued either on a percentage of AUM or, more traditionally, as a multiple of distributable earnings (I prefer this method). Either way you look at it, $10B was a handsome valuation.

The firm had about $17B of AUM (“core AUM” including Pershing Square Holdings the two private funds), so at the time PSI was valued at roughly 60% of AUM. At first glance this looks stratospheric, but it’s not as egregious when you look under the hood. Alternative asset managers like Blackstone, KKR, Apollo, and BN are valued at 10-15% of AUM. This isn’t the most useful metric because of PSI’s insanely high margins and high AUM-to-employees. Price to distributable earnings is a far more relevant metric.

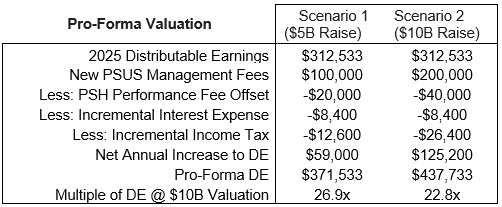

On a distributable earnings basis, Brookfield and KKR trade around 15x and Blackstone is slightly more expensive at 19x distributable earnings. A $10B 2024 valuation for PSI equates to about 32x trailing distributable earnings for PSI, about double most comps. But this isn’t the number we really care about because it doesn’t incorporate the new fee stream from the launch of PSUS (the whole reason PSI is IPO’ing in the first place!).

On a pro-forma basis, the valuation is more reasonable. PSUS is targeting a $5-$10B initial fund raise at the IPO (a few billion has already been committed via a private placement), which they refer to as “scenario 1” and “scenario 2” in the S-1 filing. If we add in incremental fees from PSUS and account for other weird things like an offset agreement with Pershing Square Holdings, a $10B valuation for PSI would equate to a 23-27x multiple of DE; still high but maybe not absurd? A premium to the other public alternative asset managers is perhaps justifiable because of the permanent capital nature, long growth runway of PSI, and all the other reasons discussed above.

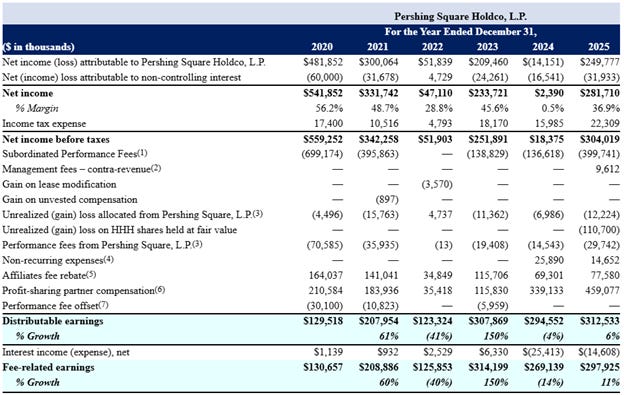

That’s all well and good, but what we care about even more is what could PSI be worth a few years from now? Here is how DE has compounded over the past five years (adjusted for the new comp structure with the Preferred/Subordinated performance fee split):

Distributable earnings have grown at a 19% compound annual rate since 2020 which closely tracks the firms CAGR in AUM which has been a whopping 24% per year since 2020. Core AUM has compounded at about 14% per year with the balance of the increase coming from consolidating HHH which now counts as AUM for Pershing Square.

If PSI can keep growing distributable earnings at a mid-to-high teens rate for the foreseeable future, a 20x+ multiple for the stock will prove reasonable. Put another way; business returns for PSI at 20x distributable earnings and 15% growth are 20% (5% yield + 15% growth).

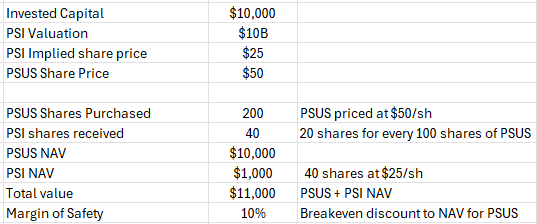

Finally let’s look at the combined offering; investing in the PSUS IPO and getting shares in PSI. If the $10B PSI valuation sticks, that puts the share price at $25 (they have 400 million shares outstanding). An investor that invests $10K into the IPO will receive 200 shares in the fund (PSUS) and 40 shares in PSI. Total NAV of the two combined holdings will be $11,000, meaning as long as PSUS trades at less than a 10% discount to NAV, you’re in the money.

What about the forward returns? That requires assessing how you think Ackman’s portfolio will do. If you take his super long-term returns as a proxy for forward returns, which I think is reasonable, the portfolio, and therefore AUM and fees, could compound at 15-16% per year.

If he achieves similar returns over the next decade, PSI’s intrinsic value will compound at 15%+ per year as will the investment in PSUS.

The bad news is that earnings are likely going to be depressed this year because PSH is down quite a bit to start the year. However, given the concentrated nature of the portfolio, things can turn around quickly. On the other hand, it also means that growth could be super-charged for those that buy into PSUS at potentially depressed prices (I have some doubts about how his recent investments will work out, but we’ll see).

I’m fascinated to find out a) what valuation the market assigns to PSI and b) what discount PSUS trades for.

I think the bonus shares in PSI, the reduced fee burden, Ackmans celebrity status, and the U.S.-based listing make it unlikely that PSUS trades at more than a 10% discount to NAV, other than maybe temporarily. If he comes out of the gates hot, there is an outside shot that PSUS could even temporarily trade for a premium to NAV, though I think it’s unlikely.

The dual listing IPO is a unique structure and makes for a fascinating study. The combined offering doesn’t strike me as an obvious fat pitch, though it seems there’s a reasonable chance IPO investors will do well. I’ll be most interested to follow PSI over time. During a tough market or an occasional blunder from the Pershing Square investment team the management company’s valuation could temporarily become dislocated from reality and prevent an excellent investment opportunity in a capital-light compounder.

Further reading

Bill Ackman Details Plan to Take Hedge-Fund Firm, New Fund Public Simultaneously

Ackman’s Compensation and Other News We Learned From Pershing Square’s Filings

Bill Ackman Has a Stroke of Genius. Buy His New Fund and Get Shares of His Pershing Square IPO

Bill Ackman Wants Your Money Again

Do you have a “stranded” 401(k) from a past job that is neglected and unmanaged? Eagle Point offer separately managed accounts to retail investors, and 401(k) rollovers are often a good fit for our long-term approach. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.