Odds & Ends: Investing like a Formula 1 driver, bear markets, stocks vs. real estate, and the problem with innovation.

Look A Little Further Down The Road

An F1 driver racing at over 200 miles per hour needs lightning fast reflexes to win, let alone survive. The best drivers have a 360 degree awareness at all times and can react at what seem like instantaneous speeds.

How do they do this? F1 drivers are probably blessed with above-average reflexes, but the human body has limits. What really distinguishes the best drivers from us mere mortals is that they focus their attention much further down the road.

At the apex of their current turn, a F1 driver’s attention is already on the next turn This gives them a few extra milliseconds to prepare.

F1 drivers can do this because they are such deeply competent drivers that the physical act of turning the wheel and shifting gears happens automatically. It requires no conscious effort. Their conscious brain is free to look a little further down the road and prepare for what’s coming next.

The best investors do the same. Popular wisdom holds that the market looks out about six months. That seems about right. For instance, last November the market started to fear a Fed hiking cycle. Sure enough, the Fed did hike rates five months later in March.

Unconventional results require unconventional methods. Investors seeking above-average returns need to look a little further down the road than everyone else. In practice this requires two steps.

First, own businesses that you understand and that are resilient to a variety of macro economic regimes. We prefer businesses like cockroaches — very hardy and almost impossible to kill. A business that can’t withstand a little inflation or higher interest rates is not worth owning.

Resilient businesses require less quarter-to-quarter upkeep, which frees the conscious mind to look further down the road. A balance sheet drowning in cash doesn’t require a liquidity analysis every quarter.

Once an investor is in this position — owning simple businesses that they understand drowning in cash — they have the luxury of looking a few years down the road. These investors can engage in “time arbitrage.”

Time arbitrage involves buying businesses whose six to twelve month outlook is poor but whose long-term outlook is positive and balance sheets are strong enough to bridge the two. Since the market will focus on negative 6-12 month outlook, these businesses often trade at a discount to their long-term, normalized earnings.

Bear Markets

Now that the S&P 500 is more than 20% off of its highs, we are officially in a bear market. There’s nothing special about a 20% draw down though. I’ve never understood why a 20% draw down gets more fanfare than a 19% drawdown.

Bear markets are healthy and inevitable. Every long-term investor goes through at least one and likely many. The economy is always headed towards a recession, we just don’t know when it will arrive.

Bear markets become less stressful when you prepare for them during bull markets. It’s childish to think you’ll be able to sell your fashionable-yet-unprofitable stocks at the top before the music stops. Instead, only own businesses resilient enough to weather a storm. When you own resilient businesses with strong cash flows at reasonable prices, you don’t need to predict when the next correction will occur. Don’t predict. Do prepare.

As Peter Lynch says:

Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.

Recessions make the best businesses stronger because tough times cause their weaker competitors to fold. Though profits might temporarily dip, their competitive position improves.

Recessions create volatility, and volatility creates opportunities. As Morgan Housel points out:

Every past decline looks like an opportunity, every future decline looks like a risk.

Nothing that the U.S. faces is unprecedented. We’ve faced inflation, supply chain snarls, war, and pandemics. We got through those and we’ll get through these. It may take a little time and look a little messy, but that’s just how democracies and capitalism work. They are the best we’ve got.

So take the long view and look at this decline as an opportunity, not a risk.

Stocks vs. Real Estate

Investment is most intelligent when it is most business-like.

— Ben Graham, The Intelligent Investor

Mr. Money Mustache (aka Pete Adeney) wrote an excellent piece this week compares and contrasts investing in real estate and stocks. If you are unfamiliar with Mr. Money Mustache, start with his profile in the New Yorker and interview with Tim Ferriss.

Adeney’s conclusion mirrors what Dan and I wrote in our Spring 2021 Letter — investing in rental properties and stocks are two versions of the same thing. Both are investments in real, productive assets whose value derives from their future cash flows.

Since rental properties are illiquid, they don’t have fancy price charts to distract investors away from their cash flows. And real estate transactions typically involve banks, lawyers, and insurers who provide some adult supervision and enough friction to slow down knee-jerk reactions. All of this means that investors tend to naturally approach real estate in a business-like manner.

Unfortunately, that attitude rarely carries over to stocks. Stock market investors tend to focus on price rather business ownership. Adeney writes, “When you hear people talk about the “200 day moving average” or “support level” or “death cross pattern”, you can safely assume they suffer from this condition.” These investors focus on an outcome (rising prices) without considering what makes a stock valuable (earnings).

If there’s a silver lining, it is that the irrational behavior of other investors creates volatility that rational investors can capitalize on to earn above-market returns.

Adeney concludes that investors should view real estate and stocks (and all other investments) through the same lens — “What value does the house (or company) deliver to society, and what are its earnings relative to the price you are paying?”

Taken a step further, investors should allocate their capital to their highest return opportunity, regardless of its name. Real estate, private equity, growth stocks, value stocks, and commodities should all be judged by a common yardstick: how much cash are they likely to produce relative to their current price?

Innovation: The Tortoise And The Hare

Goldman Sach’s Non-profitable Tech Index (blue) and the S&P 500 Value Index (red)

Innovation is unequivocally good for society, but it is not always good for investors. This is perhaps the most mis-understood concept in investing.

It is perfectly possible that both:

EV’s and blockchain could radically change our world; and

Investors in EVs and blockchain could, in aggregate, lose a lot of money.

Both can happen at the same time. They are not mutually exclusive. That’s how past innovations played out, at least. Society benefitted at the expense of investors.

Buffett himself says so. Here’s what he said at Sun Valley in 1999:

I thought it would be instructive to go back and look at a couple of industries that transformed this country much earlier in this century: automobiles and aviation.

Take automobiles first: I have here one page, out of 70 in total, of car and truck manufacturers that have operated in this country. At one time, there was a Berkshire car and an Omaha car. Naturally I noticed those. But there was also a telephone book of others. All told, there appear to have been at least 2,000 car makes, in an industry that had an incredible impact on people’s lives.

If you had foreseen in the early days of cars how this industry would develop, you would have said, “Here is the road to riches.”

So what did we progress to by the 1990s? After corporate carnage that never let up, we came down to three U.S. car companies — themselves no lollapaloozas for investors.

So here is an industry that had an enormous impact on America — and also an enormous impact, though not the anticipated one, on investors.

Rivan is a modern example. The company makes really cool all-electric trucks, but that doesn’t mean it has been a good investment. The company’s stock peaked in November 2021 at $172, the height of the meme-stock hype cycle, and has fallen 83% since.

The same thing happened with airplanes. Society benefitted, but investors didn’t.

Now the other great invention of the first half of the century was the airplane. In this period from 1919 to 1939, there were about two hundred companies.

Imagine if you could have seen the future of the airline industry back there at Kitty Hawk. You would have seen a world undreamed of. But assume you had the insight, and you saw all of these people wishing to fly and to visit their relatives or run away from their relatives or whatever you do in an airplane, and you decided this was the place to be.

As of a couple of years ago, there had been zero money made from the aggregate of all stock investments in the airline industry in history. So I submit to you: I really like to think that if I had been down there at Kitty Hawk, I would have been farsighted enough and public-spirited enough to have shot Orville down. I owed it to future capitalists.

It’s wonderful to promote new industries, because they are very promotable. It’s very hard to promote investment in a mundane product. It’s much easier to promote an esoteric product, even particularly one with losses, because there’s no quantitative guideline.

EVs and blockchain are easy to promote because there is no quantitative guideline about how much they are worth. This gives promotors cover to make outlandish statements. For example, Ark Invest published research on Zoom Video Communications on June 8, 2022 that called for a $700 price target in 2026 in their bear scenario. They forecast $2,000 in their bull scenario. That day, Zoom closed at $111 per share, so they anticipate a 69-128% CAGR.

While anything could happen, investors should beware of anything that seems too good to be true. Picking the winners in a technologic revolution is extraordinarily hard.

So what’s an investor to do? Peter Lynch wrote in One Up On Wall Street:

Many people prefer to invest in a high-growth industry, where there’s a lot of sound and fury. Not me. I prefer to invest in a low-growth industry like plastic knives and forks, but only if I can’t find a no-growth industry like funerals. That’s where the biggest winners are developed.

Growth is only one tool a company has to create value. Yield is the other. At a low enough price, any profitable business can become lucrative.

For example, buying a stable, no-growth business for ten times earnings will produce a 10% return. Paying 6.7x will produce a 15% return. Though these opportunities don’t come along often, they do come along if you’re looking for them.

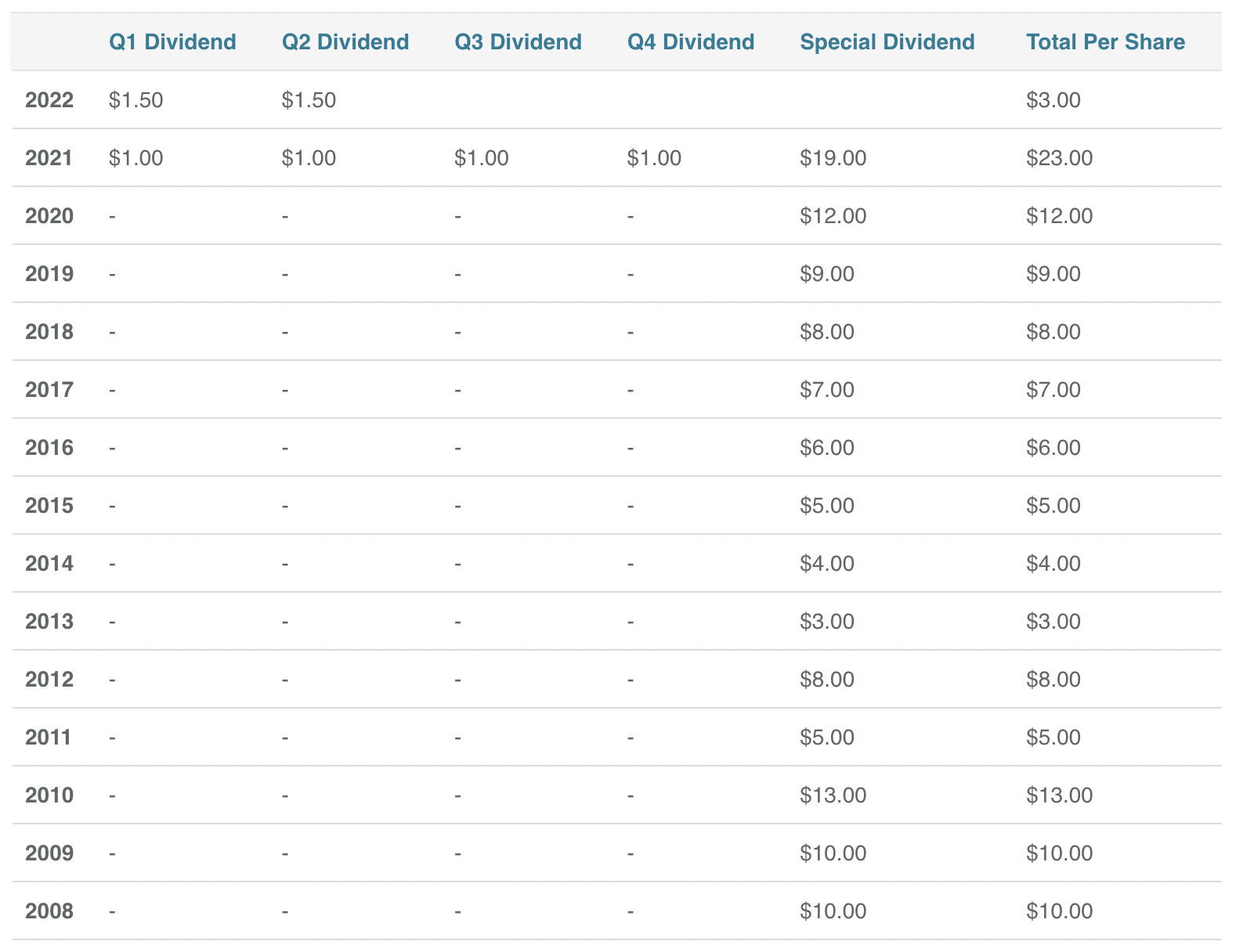

For example, Diamond Hill currently trades at a 15.3% dividend yield. That’s based on $6 per share of regular dividends ($1.50 per quarter) and the expectation of a $19 per share special dividend in December. Last year they paid a $19 special dividend, and they’ve paid a special dividend every year for 14 years.

Year to date through May, Diamond Hill’s AUM is down 8.5%. So they’re holding up much better than the broad market, but earnings may be down a little this year. Fortunately the company has so much extra capital ($164 million or $51 per share) that they can afford to pay a $19 special dividend regardless of current earnings. In addition, Diamond Hill is repurchasing shares, which increase their effective yield.

Even if Diamond Hill doesn’t declare a $19 special dividend, it is very likely to declare one which means Diamond Hill’s yield is high. As Ben Graham said, you don’t need to know a man’s exact weight to know he’s fat.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.