Moody’s, Autodesk, and Standards-Based Moats

Moody’s and Standard & Poor’s (SP) shouldered significant blame in the aftermath of the Great Financial Crisis. Critics accused these bond rating behemoths of acquiescing to Wall Street’s financial innovation and slapping triple-A ratings on complex debt instruments that turned out to be worthless. Worse, they were accused of cozying up to customers (companies issuing debt) and creating conflicts of interest by rating issuer’s debt favorably in order to win more business.

Congress was so incensed with the credit rating agencies they summoned Buffett, who still owns about 11% of Moody’s, in for an interview to unpack more about the business and its role in the financial meltdown of 2008.

Whether or not they were actually to blame, Moody’s perceived conflicts of interest were being pointed to as a major cause of the worst economic collapse since the great depression and it appeared reasonable to question whether or not the business was viable going forward. After all, rating bonds is largely an undifferentiated service (i.e. a commodity) so a new, unbiased, rating agency could unseat Moody’s and S&P from their dominant positions, right?

Moody’s stock bottomed out at about $16 per share in 2009, down about 75% from 2006 highs, and it looked justifiable at the time.

Well, Moody’s earnings are up about 7-fold since 2007 and the stock has gone up more than 20-fold since cratering in early 2009. Today, Moody’s is universally considered one of the best businesses in the world.

When such an onslaught of criticism and pessimism has virtually no impact on a company’s long-term prospects, it’s probably worth trying to understand why.

Regardless of what the companies might tell you, credit rating agencies offer largely undifferentiated services, possess no special technology, are not run by business geniuses, and have no particular human capital advantages. Yet they’ve delivered enviable investment returns over long periods. At the heart of Moody’s resilience is what I refer to as a “standards-based moat”.

I’ve been thinking about this dynamic a lot lately and below I’ll take a look at Moody’s and Autodesk, both of which benefit from this tremendous competitive advantage.

Moody’s

Moody’s was founded in 1909 to produce manuals of statistics for bonds as well as bond ratings. The company was purchased by Dun & Bradstreet in 1962 and spun out in 2000.

The core ratings business, referred to as “Moody’s Investor Services” (MIS), does around $4B of global revenue with outstanding 60% operating margins. MIS represents around 60% of Moody’s revenue and 80% of operating income.

MIS Revenue – 2021 10K

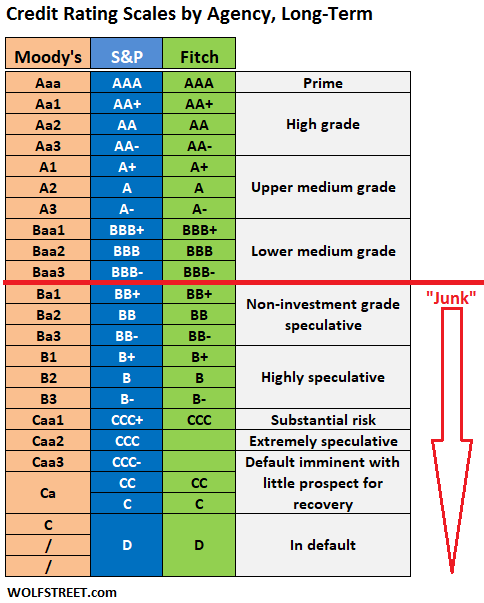

Moody’s receives a small percentage of a bond issuance as a fee for providing a rating. Moody’s rates debt based on the financial quality of the issuer and their likelihood to successfully service the debt. The ratings scale for Moody’s, S&P and Fitch (a much smaller ratings agency) looks something like this:

Source: Wolfstreet.com

A bond’s rating is important because it not only indicates the riskiness of the bond but it impacts the pricing for the issuer (the more risky the bond the higher the interest rate) as well as who is allowed to invest in the debt, among other things.

Why do credit rating agencies exist in the first place – why can’t bond investors make their own assessment of these risks?

Importance of Standard Measurements

When asked why he still owned shares in Moody’s during Buffett’s 2010 interview with the “Financial Crisis Inquiry Commission”, he explained:

“I thought they had an extraordinary business and, you know, they still have an extraordinary business…there are very few businesses that had the competitive position that Moody’s and Standard and Poor’s had, they both had the same position essentially. Very few businesses like that in the world. It’s a natural duopoly to some extent, now that may get changed, but it has historically been a natural duopoly where anybody coming in and offering to cut their price in half had no chance of success. And there are not many businesses where somebody could come in to cut the price in half. And if somebody doesn’t think about shifting, but that’s the nature of the ratings business and it’s a naturally obtained one. I mean, it’s assisted by the fact that the two of them became the standard for regulators and all of that. So it’s been assisted by the governmental actions over time.”

Clearly Buffett understood how imbedded Moody’s and S&P were into the financial infrastructure of America. If a business is unlikely to be impacted despite a competitor offering the same service for half the price, you know you’ve found something special.

Ironically (but not surprisingly), despite owning more than 10% of Moody’s, Buffett never uses their ratings. When asked about that during his interview with congress the exchange went like this:

Interviewer: Now, Mr. Buffett, you’ve been reported as saying that you don’t use ratings.

Warren Buffett: That’s right.

Interviewer: But the world does.

Warren Buffett: That’s right. But we pay for ratings which I don’t like. (laughs)

Interviewer: My question is one of more policy and philosophy and that is, would the American economy be better off in the long run if credit ratings were not so embedded in our regulations and if market participants relied less on credit ratings?

Warren Buffett: Well, I think it might be better off if everybody that invested significant sums of money did their own analysis but that is not the way the world works. And regulators have a terrible problem in setting capital requirements all of that sort of thing without some kind of standards that they look to even if those are far from perfect standards. I can’t really judge it perfectly from the regulators’ standpoint.

Interviewer: Would you support the removal of references to credit ratings from regulations?

Warren Buffett: That’s a tough question. I mean, you get into, you get into, you know, how you regulate insurance companies and banks. And we are very significantly in the insurance business and we are told that we can only own triple B and above and different--there are all kinds of different rules in different states and even different countries. And those may serve as a crude tool to determine proper capital or to prevent buccaneers of one sort from going out and speculating in the case of banks with money that’s obtained through a government guarantee. So that is not an easy question.

This brief excerpt distills why Moody’s is so hard to replace. Regulators need to ensure that banks, insurance companies, pension plans, retail investors, and others have a way to safeguard against the risks they’re taking when investing in debt. There needs to be a ratings system - even if it’s far from perfect – that allows the government to assess risk levels and set capital requirements for major financial institutions that are integral to the economy and population in general. Importantly, the ratings system needs to be consistent to allow for apples-to-apples comparisons.

Ideally, we could trust banks, insurance companies, and pension plans to responsibly invest their customer’s cash balances in prudent ways. Obviously, that’s not how the capitalist world works. If left to perform their own “ratings”, some critical financial institutions would inevitably take undue risks causing some to fail and inflict mass collateral damage on the financial system and society.

Moody’s and S&P effectively represent a toll road on the issuance of debt. Year-to-year debt issuances will bob around but companies will always continue to issue and refinance debt. Inflation and economic growth mean the nominal value of debt will increase and Moody’s gets a skim off the top of that growth without needing to employ any real incremental capital.

In addition to having a royalty on debt issuances, Moody’s and S&P have developed into an unusual duopoly. Unlike other duopoly/oligopolies - like AutoZone and O’Reilly where a mechanic either works with one or the other - using one of the major bond rating agencies isn’t an either/or, it’s an and. Virtually all bonds are rated by both Moody’s and S&P. The reason is the low cost of receiving a rating relative to the principal of the bonds that the issuer will receive.

So, we’re left with a major reliance on an imperfect system with Moody’s and S&P at center stage. By luck, skill, or an accident of history, they are the standards that are deeply rooted within the immense world of fixed income and there’s virtually no way to tear them out.

Sure, if a company came up with a perfect way to predict default outcomes among debt issuers, maybe it may become the new standard. But as long as humans are involved, there is never going to be a perfect ratings system, or even one that’s much better than what we’ve got, so there is no reason to switch from a system that underpins our financial plumbing for little benefit. The beauty of switching costs.

This standards-based moat in the ratings segment has conferred incredible pricing power for Moody’s and enabled them to spawn another profitable growth segment.

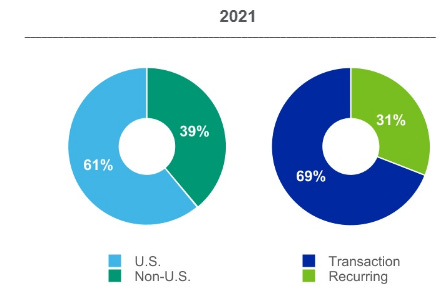

Moody’s Analytics

Since the financial crisis Moody’s has emphasized growing its analytics business. The MA segment is almost entirely subscription-based recurring revenue. Its products focus around risk management such as credit risk analysis, economic forecasting, ESG analysis, regulatory compliance, and other risk solutions.

MA Revenue – 2021 10K

Moody’s leverages its immense data set from the entrenched MIS segment to spin up analytics offerings to its swath of ratings customers. The analytics segment grows both organically and inorganically. Like many businesses that benefit from high switching costs, Moody’s can purchase smaller software companies and immediately grow their distribution reach to an existing ~15,000 customers.

Source: 2021 10K

While not as profitable as the ratings segment, Moody’s Analytics still enjoys great economics with 30% operating margins and sustained mid-teens annual growth.

Thanks to the combination of a deeply embedded ratings business and a rapidly growing and sticky SaaS segment, Moody’s is poised to continue growing at double-digit clip for years to come.

Autodesk

Autodesk is a leading provider of design software for architects and engineers. The company specializes in 3D design and engineering software and also offers media products.

Source: 2021 Investor Presentation

Autodesk’s most popular offerings include Revit, a building information modeling (BIM) software, AutoCAD drafting software, and many others.

Autodesk’s products are almost all offered through a subscription model and as such the company enjoys the economics of other high quality software companies. Autodesk produces excellent returns on capital, 110%+ net revenue retention, and 97% recurring revenues. Cash flow per share has compounded at 35% over the past 5 years since the transition from a license-based to subscription-based model. David Kim of Scuttleblurb (highly recommend subscribing to his work) wrote an excellent two-part piece on the architecture and design software landscape, including Autodesk, for those interested in a deep dive.

Like with Moody’s, Autodesk’s advantage can be best understood by looking at the business after a period of extreme pessimism. Instead of upsetting regulators, Autodesk recently faced blowback from major customers.

2020 Customer Letter to CEO

In 2020 seventeen prominent architecture and engineering firms penned an open letter to Autodesk’s CEO outlining a laundry list of complaints against the business. The crux of the complaints were that Autodesk consistently raised prices with little product innovation coming with the higher prices. The customers accused Autodesk of being non-responsive to feedback from its users for years. Autodesk basically agreed that they hadn’t been as innovative as they should be and outlined steps they would take to try to remedy the situation. The reality is, however, they could have continued to do nothing and customers would continue to use the software.

Why was Autodesk able to get away with consistently raising prices and shunning new features when customers could seemingly easily switch to another design software of equal or better functionality and price?

Revit’s Moat

As outlined in an article from The Architect Magazine, Autodesk’s Revit software has a virtual monopoly among architecture and design firms. Like Moody’s, the dominant position doesn’t come from superior technology or processes. Rather, its position comes from a standards-based moat.

Revit became very popular in the early 2000s as Architects adopted BIM software. Autodesk purchased Revit in 2002 and quickly become the de facto software used across the industry.

As soon as Revit gained the pole position it became a prerequisite for architecture and engineering students to learn in school. Its proprietary file format (.rvt) became the standard way that architects shared files with customers and construction firms, spawning a network effect and driving further adoption of Revit’s software.

Fast forward to today and nearly every prominent architecture firm in the U.S. and many countries around the world use Revit. Autodesk declines to disclose market share statistics and denies it has a monopoly in Revit, which I take as confirmation they indeed do enjoy monopolistic status. It would take a drastically better and lower cost design software to unravel the web of interconnectedness between architects, engineers, design firms, customers, professors, and students at the center of which Revit sits. Even then Revit’s position would unlikely become compromised.

The Architect Magazine piece concludes that customers shouldn’t hope for much by writing a letter to Autodesk (emphasis mine):

“With the move to subscription,” Bunszel says, “it’s easier than ever for customers to vote with their feet.” In a sense, she’s right. Theoretically, firms could cancel their subscription with Autodesk at any time and jump to another BIM platform the same way a consumer might cancel Netflix and signup for Hulu. But in my reporting for this piece, I couldn’t find a single large American firm that had ever transitioned off Revit”

It goes on to say:

“That July open letter focuses on the failings of Autodesk, but the root cause is a larger breakdown in the relationship between architects and the software provider. If the letter teaches us anything, it is that Autodesk can neglect Revit for years, change the pricing model, anger customers, and yet still trust that firms will be loyal customers. Users can complain about it, but realistically Autodesk could do nothing and firms will continue paying.”

Like the ratings companies did in the debt markets, Autodesk has leveraged its impregnable position with Revit to drive sustainable growth in other design software applications. Say what you will about Autodesk’s alleged customer neglect in the mid-2010s but it doesn’t look like the business is going anywhere any time soon.

Standards-Based Moat Summary

Standards-based moats are hard to dig, but once in place they’re extremely valuable and the companies are nearly impossible to kill. It’s hard to overemphasize how entrenched Moody’s and Autodesk are in their respective industries. These moats allow companies to take advantage of significant optionality in cross-selling to a captive customer base and often confer other competitive advantages like network effects. For example, Microsoft’s original moat comes from its Windows operating system becoming a standard which caused irreversible network effects to take hold. More functional or lower priced products cannot easily unseat a standards-based moat, allowing businesses that possess this advantage to enjoy enduring periods of above-average growth and pricing power.

A standards-based moat is a subset of switching costs, one of the “Seven Powers” I wrote about a few weeks ago. Investors can successfully take advantage of companies that posses standards-based moats by:

Identifying them early and before their leadership position is appreciated. This can be very challenging and/or risky but it’s possible.

Understanding how enduring these moats can prove to be and the optionality that comes along with them. The optionality and growth duration may not be properly reflected in the stock price.

Taking advantage when sentiment briefly turns against companies that possess standards-based moats like Moody’s in 2008 or after Equifax’s data breach in 2017. This simply requires patience and discipline.

For me, assembling a list of businesses that are the standard in their respective industry and then watching patiently for an attractive price should prove valuable over the long term.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.