Luxury Retailers and LVMH

Luxury businesses fascinate me because they do not follow the traditional rules of economics. In many luxury companies typical rules of business are flipped on their heads; higher prices beget more demand, product flaws are endearing to enthusiasts, and supply is rigorously controlled to ensure it can never meet demand. These are not tactics you learn in business school.

Additionally, some of the most successful luxury retailers are among the world’s oldest companies. Louis Vuitton traces its roots back to the 1800s, Rolex is more than 110 years old, and Hermes was founded in the 1830s. Finally, high degrees of insider and family ownership and long-term thinking tend to permeate these companies, which is often a huge plus for shareholders.

Motivated by the book The Luxury Strategy which I recently read, here I’ll take a look at some of the characteristics of luxury businesses I find interesting as well as a brief look at LVMH specifically. The longevity, pricing power, and high returns of the world’s most exceptional luxury companies make them an interest study, even for a person like me who can hardly tell the difference between a Rolex and a Timex.

Do you have a “stranded” 401(k) from a past job that is neglected and unmanaged? Eagle Point offer separately managed accounts to retail investors, and 401(k) rollovers are often a good fit for our long-term approach. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Luxury Overview

Luxury goods make up a $300B+ market worldwide, with main categories including jewelry/watches, leather goods, and fashion & fragrances. Generally the target consumers are high net worth and ultra-high net worth individuals and some of the key regions are Europe (specifically France/UK/Italy), the U.S., Japan, and China.

In The Luxury Strategy author Jean-Noël Kapfere clearly delineates between a luxury (which can be very subjective) and a luxury strategy. The book is about companies that have successfully (and unsuccessfully) implemented a luxury strategy – which doesn’t necessarily entail selling true luxury goods. For starters, he offers a helpful definition of luxury.

Kapfere explains the six criteria that define luxury:

A very qualitative, hedonistic experience or product made to last;

Offered at a price that far exceeds what their mere functional value would command;

Tied to a heritage, unique know-how and culture attached to the brand;

Available in purposefully restricted and controlled distribution;

Offered with personalized accompanying services;

Representing a social marker, making the owner or beneficiary feel special, with a sense of privilege.

Enviably strong brands and tremendous pricing power tend to accompany the above characteristics.

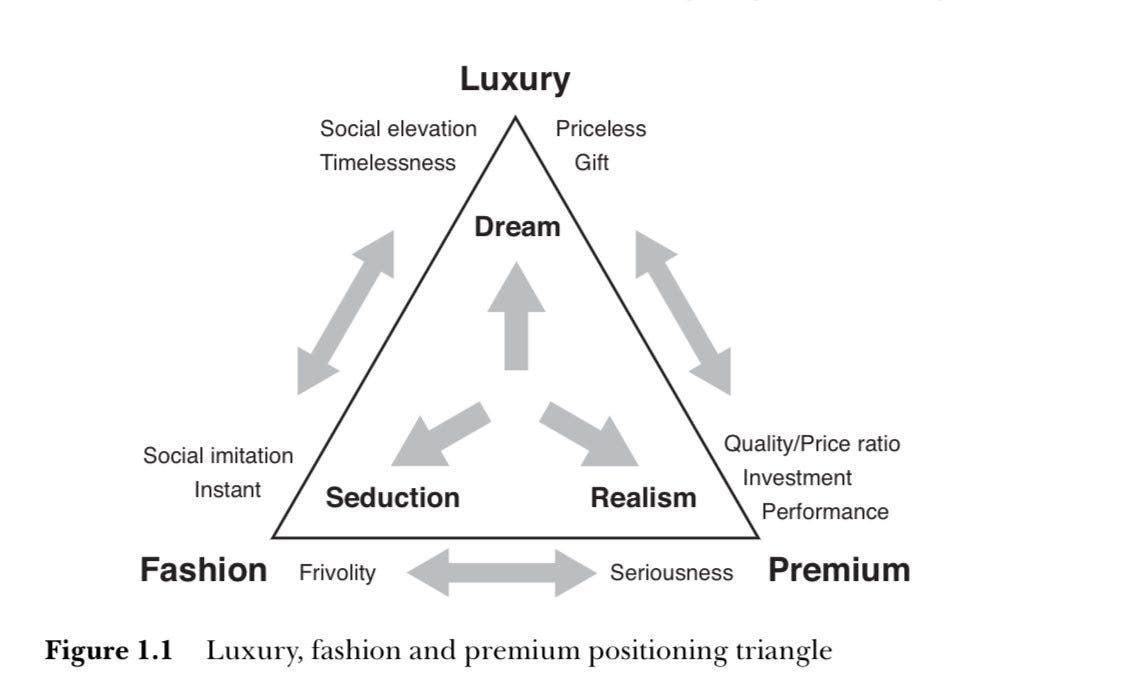

He also delineates between true luxury companies and imitators that claim to pursue a luxury strategy but instead are running a fashion or premium model.

There’s nothing wrong with the premium or fashion markets, plenty of companies make good money and earn good returns in those areas. The problem arises when a company thinks it’s something it’s not. Ford attempted to enter the luxury car market in 1989 when it purchased Jaguar for $2.5B and again when it bought Land Rover in 2000 for $2.7B. Ford bungled the luxury strategy, attempted to deploy traditional business tactics to the brands, and destroyed tremendous shareholder value in the process. Ultimately it sold the brands in 2008 for about a third of what it paid.

One of my favorite parts of The Luxury Strategy is a chapter called “the anti-laws of marketing”. In it are 24 tactics employed by luxury companies that fly in the face of traditional retailing for fast moving consumer goods (FMGCs). The full collection of anti-marketing rules are:

Forget about ‘positioning’, luxury is not comparative

Does your product have enough flaws?

Do not pander to your customers’ wishes

Keep non-enthusiasts out

Do not respond to rising demand

Dominate the client

Make it difficult for clients to buy

Protect clients from non-clients, the big from the small

The role of advertising is not to sell

Communicate to those you are not targeting

The presumed price should always seem higher than the actual price

Luxury sets the price, price does not set the luxury

Raise your prices as time goes on in order to increase demand

Keep raising the average price of the product range

Do not sell

Keep stars out of your advertising

Cultivate closeness to the arts for initiates

Do not relocate your factories

Do not hire consultants

Do not test

Do not look for consensus

Do not look after group synergies

Do not look for cost reductions

Just sell marginally on the internet

I’m not going to talk about all 24 of these, you can read the book if you’re interested in a deeper dive, but I do think a few interesting themes emerge when looked at collectively. The ability to avoid competition, rigorously control supply and pricing, and create brand mystic are some of the most important aspects that successful luxury businesses appear to have mastered.

Lack of Competition/Comparability

Luxury companies have taken the saying “niches get riches” to heart. They do not seek to sell to the masses, and in doing so remove themselves from the typical heated competition of traditional retailers. Hermes’ famed Birkin bags sell for $20K or more – for a hand bag! – on the premise that there is no substitute, and therefore no competition. Birkin bags are made with the finest quality leather on earth and takes a trained artisan 18 hours to produce. More than that, the exclusivity and difficulty in buying a Birkin hand bag makes the company an “n of 1”.

When you do not seek to differentiate yourself from competition, because there really is no competition, you can essentially set whatever price you want, and that’s what Hermes does. The same lack of substitutability is present in other luxury companies from some of LVMH’s brands to Ferrari to Rolex.

When a company can sell a bag for $20K, let alone the absurd $150K Louis Vuitton “Urban Satchel” bag, there is obviously more to it than just using really nice leather. That’s where supply control and scarcity come into play.

Supply Control and Pricing Power

Maniacal control over supply is a recurring theme among luxury businesses.

Ferrari caps production each year at around 7,000 vehicles. Models are generally pre-sold for the next year and most buyers have to wait almost a year from the time they order their car until it arrives. Clearly, if Ferrari were interested in maximizing one-year financial results, they could just produce more cars because the demand is there. Instead, they’re playing the long game. Limiting supply fosters a sense of rarity and exclusivity causing owners to value their car even more once it finally arrives. It also drives prices up.

Amazingly, Louis Vuitton literally burns unsold inventory of its bags at the end of each year to ensure scarcity. If the unsold inventory ends up in the wrong hands and is, god forbid, discounted, it taints the exclusivity of the brand and hampers future pricing power.

Another aspect of controlling supply is the difficulty in actually buying many luxury items. You can’t just order a Hermes bag online and then wait for it to arrive. You basically have to convince the sales associates at an exclusive Hermes boutique that you are worthy of buying one. From what I understand it helps to commit to spending over $100K in merchandise at the store.

Of course, not all goods offered by luxury companies are absurdly expensive. Many businesses implement a triangle or diamond strategy; whereby most profits are made in the “heart of the range” of products, which are not the most expensive but are also not the entry range products.

Below is an illustration detailing the product strategy for a number of luxury businesses.

I could simplify the luxury strategy into a simple phrase: create false scarcity for things ultra-rich people want to buy.

Brand Mystic

All of the anti-marketing laws work together to create strong brands for luxury businesses, and many of these businesses tend to follow the same few counterintuitive approaches to brand building.

First, luxury businesses do not advertise to sell. What this means is that, unlike traditional retailers, they do not run advertisements with the goal of getting whoever is watching to run out and order their product. They advertise to build and enhance the dream of one day engaging with their products. Also, they aim to advertise not only to prospective clients but to the mass of people that will never be able to purchase their products. Much of the allure of owning luxury products rests on the fact that the products “elevate” the owners socially. This can only be achieved if the brands are recognized around the world by those that own them and those that don’t.

Second, luxury businesses keep production local and have an artisan element to product design. Time and again businesses that once fell into the luxury category slowly degraded their brand by moving production to low-cost areas and found it impossible to recover.

Third, and most difficult to recreate, is time. Most of the top luxury brands have been around for centuries, and any competitor looking to start a luxury brand has decades and decades of brand building to overcome, which is impossible for most businesses to accomplish over a reasonable timeframe. When I’m looking at businesses I like to think about if I had $50 billion, could I create a legitimate competitor to the business I’m studying? There are certain companies, like Coca-Cola, Apple, Tiffany’s, Louis Vuitton, Hermes, Disney, etc. that no amount of money could allow me to recreate a storied brand that has taken decades or centuries to build. When you’ve found that, you’ve likely found a good business and many luxury companies meet pass the test in spades.

Finally, another interesting aspect of these businesses is the closely held nature of the ownership structure. I won’t go as far as to say it is an absolute requirement, but virtually all of the luxury companies discussed have a majority/control family ownership structure. These companies operate on decades-long time horizons, and my sense is that if an outside CEO were put in charge, the urge would be too great to maximize short-term profits. It’s very difficult to do things like destroy inventory and limit production unless you have significant skin in the game and a long time horizon, characteristics most CEOs do not possess.

To summarize: traditional business school strategy will teach you to make it easy on customers, give them the lowest price possible, and differentiate yourself from the inevitable onslaught of competitors. Luxury companies basically do the opposite of all of those things, and earn outstanding returns on capital in the process. Fascinating stuff if you ask me!

LVMH

Unfortunately for investors, due to the closely held nature of most luxury businesses, most of them are not public. LVMH is one exception and has been incredibly successful as a public company.

For a period of time last year when Tesla’s stock was tanking LVMH’s Bernard Arnault overtook Elon Musk as the world's richest person. Arnault founded LVMH – Louis Vuitton Moet Hennessy – in 1987 and through a series of acquisitions and strong organic growth has built LVMH into the world’s largest luxury retailer and delivered outstanding returns for shareholders. Since 2005 the stock has compounded at more than 14% per year and almost 1,100% in total, before dividends.

LVMH owns over 75 prestigious brands including luxury leather goods maker Louis Vuitton, premium champagne producer Moet & Chandon, Hennessy, Tiffany & Co., Christian Dior, and TAG Huer. All of these brands have been acquired since the late 1980s, though many of them have roots going back to the 1700s. Below you can see the smattering of luxury sectors in which LVMH participates.

I’m generally skeptical of businesses whose growth and value proposition is based on serial acquisitions. There are exceptions and LVMH appears to fall into that category largely thanks to the company’s structure and adherence to a true luxury strategy.

Consistent with many of the other company’s mentioned, LVMH is controlled by Bernard Arnault whose group controls 47% of the stock and 63% of the voting rights. The control position allows Arnault to run LVMH with a decades-long view and do things like destroy unsold inventory at the end of the year. That Arnault has been able to maintain this long-term vision successfully with LVMH as a public company is all the more impressive.

Over the past decade LVMH has retained about 2/3rds of operating cash flow and reinvested the cash at solid ~17% incremental returns, meaning the business has compounded intrinsic value by a low double-digit percentage per year. Much of the retained cash has gone to acquisitions, with the 2021 $16B acquisition of Tiffany’s being the most notable recent purchase. Shareholder yield should be 2-3% annually, suggesting the potential for low-teens per share compounding if the future looks like the past.

The stock trades for around 21x earnings, not cheap but a modest discount for its historical median 25x+ and in the vicinity of the market average. A business with pricing power, solid returns on capital, above-average growth, and sound capital allocation is worth more than average. How much more is up to the individual investor. A re-rating to the historical valuation range would add to the low-teens business returns, assuming the company can continue to replicate its playbook.

LVMH’s forward returns will be dependent on management continuing to be disciplined about holding true to the above luxury strategy playbook and finding other luxury brands to bring into the fold. Shareholders of luxury businesses would be smart to watch that management is adhering to the luxury playbook and doesn’t drift over time.

It may seem like a weird time to be reading about and studying luxury businesses. Who would be interested in evaluating a company that makes absurdly high priced products in an environment where inflation and interest rates have rocketed higher, excess savings are being depleted, and stock and bond markets are in the midst of a multi-year rough patch? If clouds begin to gather around the luxury market for a few quarters, the current valuations could quickly (and perhaps briefly) erode, providing interesting prices for long-term investors. Usually when the near-term becomes the most uncertain is when prices finally become attractive; perhaps these conditions will unfold for some of these businesses soon.

There are a few other luxury or potentially luxury retailers whose stocks are down dramatically and starting to look interesting.

Some believe that the good run for luxury businesses has come to an end. That may prove correct for a number of quarters, but those investing with a 5-10+ year timeline shouldn’t be deterred by a bumpy few months (or years) for their holdings. After the GFC, top luxury businesses saw their customers come roaring back, and all of these brands have been through dozens of economic crises over the decades. True luxury brands are remarkably resilient.

If you believe rich people will always want to find ways to splurge and show off their wealth, you can bet that luxury businesses will be there to provide them with ways to spend their money in ever-increasing sums.

Do you have a “stranded” 401(k) from a past job that is neglected and unmanaged? Eagle Point offer separately managed accounts to retail investors, and 401(k) rollovers are often a good fit for our long-term approach. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

Great write up, the follow up book 'Kapferer on Luxury' is also worth a read.

It's becoming increasingly hard to find true luxury listed co's. While many have elements, they are diluting the luxury with premium or fashion brand/product. LVMH has Louis Vuitton and others, but it also has businesses like Sephora - hardly luxury. Kering has Gucci, but then has it's new glasses business, hardly luxury.

I don't count either of these holding co's as true luxury anymore, though at the right valuation they'll obviously still be appealing.

Realistically for companies that truly adhere to the quite strict 'luxury' criteria, at present I find only a few companies; Hermes (if we forgive them their foray into makeup and skincare), Ferrari (if you ignore the licensing division), The Italian Sea Group and probably Richemont. Of these, only TISG and CFR currently have reasonable (arguably cheap) value multiples, but hoping the others will come down if the world collapses next year.

Excellent article on a fascinating industry and a leading company in the sector. Thank you.