Lowe's and a Valuation Framework

We’ve been following Lowe’s for years, and Matt first wrote some thoughts on the stock in 2020. Now seems like a good time for an update.

Lowe’s is a simple, high-quality business in the midst of a multi-year transition that may leave it as an even higher quality business in the years ahead.

Though the business earns high returns on capital and has generated attractive shareholder returns, Lowe’s has long trailed its main competitor, Home Depot (itself a fantastic business) in a variety of key business measures. Marvin Ellison, a former Home Depot Executive, took over as CEO in 2018 to narrow the gap. So far, he’s making great progress. Around the same time Ellison joined, Pershing Square took a large position in Lowe’s, and it is currently Ackman’s largest position outside of Universal Music Group.

Overview

Lowe’s doesn’t need much of an introduction. It’s the second largest home improvement retailer (behind Home Depot) in the world. It was founded a little over a hundred years ago and currently operates over 1,700 home improvement stores.

While Lowe’s and Home Depot are by far the most scaled and dominant players, the massive home improvement market in the U.S. remains highly fragmented. Lowe’s estimates the home improvement market in the U.S. is around $1 trillion, split roughly 50/50 between DIY and “Pro” customers. Currently 75% of Lowe’s business is for DIY-ers, and the business has been focused on driving rapid growth in the Pro segment to align the business more closely with the industry’s 50/50 split.

Industry Divers

We like industries whose underlying drivers are easy to understand. The home improvement market is driven by trends in the U.S. housing stock, consumer finances, and longer term demographics. All appear to be working in Lowe’s favor to varying degrees.

U.S. Housing Stock fundamentals include:

Home price appreciation, which has been unusually strong since the pandemic began, and has only began normalizing in recent months. This is, over long time periods, a tailwind.

Age of the housing stock. The older the stock, the more non-discretionary home improvement projects. Right now 50% of the houses in the country are over 41 years old.

Supply of homes. The U.S. has underbuilt homes since the GFC. Presently there is likely a 1.5-2.0m undersupply of homes.

Consumer Finances

Disposable income and home equity are the key drivers of spend on home improvement projects. Coming out of the pandemic consumers still have $1.5T of excess savings.

More importantly, home equity levels are at an all-time high, with $330K of average home owners’ equity (this is closely tied to home price appreciation).

Demographic trends

Millennials are just beginning to enter the homeowner market, and are poised to become a major driver in new homes and home improvement spend in the years ahead.

Baby boomers are aging in place. This dynamic has a multi-fold impact on Lowe’s business; it drives up the average age of homes and housing prices (because it limits supply of houses that go on the market) both of which are positive for home improvement retailers.

Remote work trends while lessening, seem unlikely to revert to pre-pandemic levels. Office occupancy is still just 50% of pre-pandemic levels, and remote work stimulates demand for home renovation projects.

One might think that Lowe’s business is overly cyclical and follows the boom/bust cycles of home builders. This is not supported by evidence.

During the Q1 earnings call Ellison discussed the above drivers while highlighting the fact that 2/3rds of Lowe’s business is non-discretionary.

“When we take a look at what our demand drivers are for home improvement -- and just to be specific, these are historical demand drivers that have held up over time. They still remain supportive. And things like disposable personal income, which I mentioned, is roughly $1.5 trillion in savings above pre-pandemic levels. the average equity in U.S. homes, roughly $330,000 on average, the age of homes, and a reminder, 2/3 of everything we sell is non-discretionary. And there are other tailwinds, millennial household formation trend, baby boomers aging in place and more widespread sustainable remote work, so all of these things give us some confidence that the backdrop remains supportive.”

As any homeowner can attest to, when something in your home breaks that you need, you fix it. If the humidifier is leaking on your furnace you don’t let the water accumulate on your floor. You run to the store (or call a handyman to run to the store) – usually Lowe’s or Home Depot – and get a new connection.

Competitive Position

Like many of the businesses we follow, Lowe’s benefits from major scale advantages compared to the much smaller players that make up most of the rest of the industry.

Lowe’s main scale advantages revolve around inventory availability, pricing, and technology offerings.

When something critical breaks in your home, or you or a contractor need something immediately to finish a project, it’s essential that the item is in stock at a nearby home improvement store. Importantly, you don’t wait for Amazon to deliver the part. You need it now, and it’s likely Lowe’s has it in stock. Much like AutoZone’s business, immediate parts availability usually trumps lowest price. Massive retailers like Lowe’s can stock a far greater variety of inventory than smaller competitors.

Price is still far from trivial, and Lowe’s is able to offer competitive pricing while maintaining margins thanks to major bargaining power with suppliers.

Finally, Lowe’s has invested billions of dollars into becoming an omnichannel retailer and has greatly improved the front and back end technology at the business. Now consumers can easily order products online, schedule in-store pickup, or do things like browse the app to find which aisle a certain type of screw is located.

These little differences in inventory availability, pricing, and technology amount to major competitive advantages over mom and pop or smaller competitors, and has resulted in share gains for Lowe’s.

A good example of a large scale project that smaller companies cannot execute is Lowe’s recent supply chain transformation from a store delivery model to market delivery model. Enabled by technology and well executed by management, it has improved customer experience through enhanced product visibility and availability as well as freed up valuable space within Lowe’s stores. Supply Chain VP Donald Frieson gave an overview of the initiative during last years’ investor day:

“One critical step in our evolution is moving away from a store delivery model, which was terribly inefficient. With our old store-centric system, essentially each store served as its own distribution center for big and bulky products. We were holding appliances in our back rooms and storage containers behind our stores and using our store trucks to deliver them to customers.

That meant customers could only purchase the inventory from that single store. They didn't have visibility into the available inventory we had to offer and neither did our associates. And because our store-based trucks didn't have delivery or routing software, customers didn't have visibility into the delivery process. They didn't know when their appliances would arrive. So to say this was a poor customer experience would be an absolute understatement.

Our new delivery model, the market delivery model, is at the center of our supply chain transformation, enabling us to further consolidate our industry-leading position in appliances and positioning us for profitable growth in other big and bulky categories like grills, riding lawn mowers, stock cabinets and vanities. Let's take a look at the benefits of our new market delivery model for big and bulky product through the eyes of a customer.

We have 8 geographic regions up and running on this new model, and we're on track to complete the full rollout by the end of 2023. As we rolled out market delivery, we're freeing up space in our back rooms, which were originally built to support the store delivery model. These oversized backrooms are 10,000 square feet on average, and they give us a distinct competitive advantage because they're much larger than our closest competitors' limited backroom space.”

Lowe’s scale differentiation and the fragmented nature of the home improvement market have allowed the business to grow reliably without getting into irrational pricing wars with Home Depot.

Pro Customer Opportunity

Historically Lowe’s business has been underpenetrated with “Pro” customers such as contractors, property managers and other professional builders. Management has put a major emphasis on growing the Pro business with a target of driving revenue growth at twice the market rate.

Here again Lowe’s scale advantages factor heavily into their success with Pro customers. Lowe’s aims to lure Pro customers away from smaller competitors by offering one stop shopping, a technology-enabled omnichannel offering, a compelling rewards program, and things like job site delivery.

Management has closed Pro product gaps and made doing business with these customers much easier over the past several years, and the results have shown. Since 2019, Pro segment revenue mix has grown from 19% to 25% and overall Pro revenue growth has been 76%. The company has seen significantly improved Pro customer satisfaction service scores as well.

This effort is still in the early innings and management has an opportunity to drive outsized growth in the Pro segment for years to come. While Pro customers represent about half of the home improvement market currently only 25% of Lowe’s revenue is derived from the Pro segment.

Growth Algorithm and Business Returns

Lowe’s has grown its topline revenue at about 7% annually for the past decade. While not earth shattering, there aren’t many businesses that can grow profitably at rates like this for ten year periods or more. Perhaps surprisingly, virtually none of that growth has come from building new stores. Store count has been essentially flat for more than a decade.

Growth at Lowe’s is driven by same-store sales growth, which in turn is a function of the number of transactions per year and the average ticket size per transaction (in other words how often people shop and how much they spend while shopping). Both measures have marched reliably higher over time.

We’ve seen an uptick in average ticket over the past few years thanks to a pickup in inflation, which Lowe’s has largely successfully passed along to consumers. Transactions have ticked down somewhat because of rising prices (and a pandemic-induced surge of home improvement spending) but the net effect has been positive for Lowe’s revenue.

On balance I’d expect Lowe’s to continue driving mid-single-digit same-store sales growth for many years to come. Lowe’s continually invests in its stores to drive this growth. Examples of investments include the above mentioned Pro segment initiatives, and a smattering of other supply chain and technology investments centered on having the right products in the right place at the right time. Investing for growth and growing revenues is great and all, but it’s only valuable if it translates into growth in per share earning power. So how does Lowe’s fair?

Incremental ROIC (I-ROIC)

To us, the easiest way to measure management’s ability to create value is to follow all the cash that comes in and goes out. Over the past ten years the company has taken in about $105B of cash through operating cash flow, debt issuances, and share issuances (which have been trivial). Over the same time period the company has sent out about $88B in cash through debt repayment, share repurchases, and dividend payments, meaning the company retained about $17B. Operating cash flow has grown by $4.5B over the past decade, so the incremental return on retained capital (I-ROIC) is around 27% - pretty damn good.

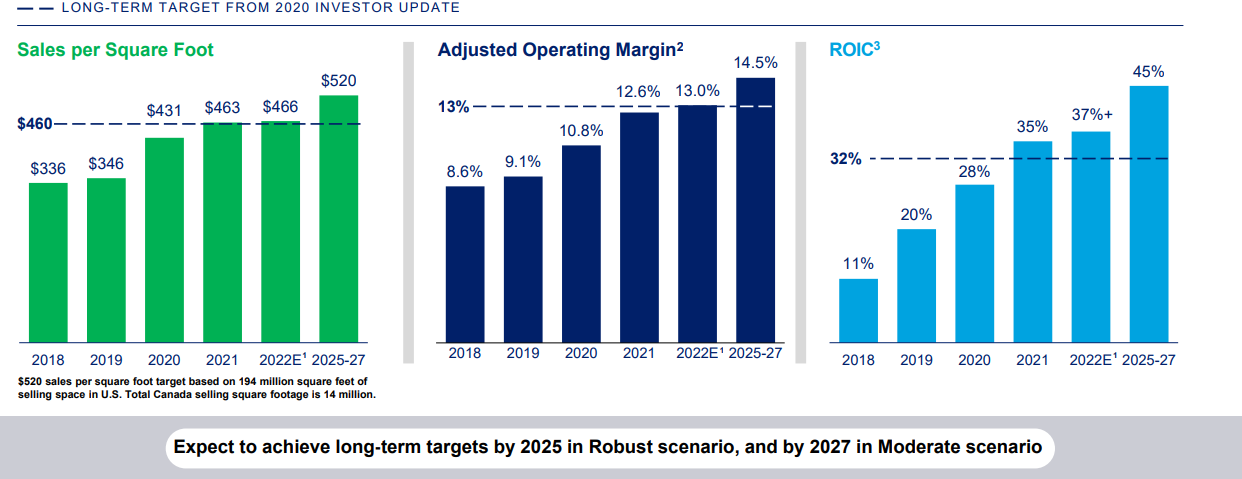

These incremental returns on capital aren’t surprising given the high quality nature of Lowe’s business and its historically attractive, and improving, returns on capital of 40%+.

The $17B retained represents about 25% of the company’s operating cash flow, which is what we would consider the reinvestment rate. A business's intrinsic value should compound at approximately the product of the reinvestment rate and the incremental return on invested capital, meaning Lowe’s compounds at around 7% annually (25% x 27%).

7% compounding is not bad but nothing to write home about. But it’s not the absolute compounding rate that matters for investors, it’s the per share compounding rate. We love businesses that can grow at attractive rates while still returning an outsized portion of earnings to shareholders through repurchases and dividends. Lowe’s fits the bill well.

Because Lowe’s only needs to retain 25% of profits it can return the rest to shareholders. Management has elected to emphasize share repurchases as the preferred way of returning capital. Since 2012 Lowe’s has spent about 90% of its operating cash flow on repurchasing stock and shares outstanding have declined by a little less than 6% per year. This has created a tremendous tailwind for per-share returns and is a big reason why Lowe’s stock is up nearly 400% over the past ten years.

If the future resembles the past the business could continue to compound at an attractive low-to-mid-teens per share annual rate for many years. This is driven by 7-10% base compounding (management expects margins to continue expanding, adding a few percentage points of return annually to the ~7% mentioned above) plus 6-7% shareholder yield.

Investors will only realize a satisfactory return on this low/mid-teens business compounding if the price paid a) enables an attractive shareholder yield and b) returns aren’t likely to be wiped out by a valuation multiple contraction. After all, investing is about balancing a three legged stool.

So what is Lowe’s worth?

Valuation

Now seems like as good of time as any for a quick detour on valuation.

**Warning: the next few paragraphs are going to be very dull, so for all the normal people not interested in a conceptual discussion on valuation, please skip right to the end**

As most investors are aware, a company is worth the sum of the cash it will kick off over its lifetime discounted back to present day at an appropriate rate. While true in theory, in practice I’ve never built a detailed DCF to value a company. Discounted cash flows tend to be unrealistically detailed and overly reliant on unknown inputs. Basically garbage in garbage out with a heavy dose of unknown extrinsic factors.

Another popular “valuation” technique is to pick a bunch of competitors, see what type of valuation they trade for, and slap that earnings multiple on the business in question. Still another popular method in determining if a company is undervalued is to look at what valuation multiple it has traded for over an extended period of time, and call that a fair multiple, and wait for the valuation to go below its historical average. These relative valuation approaches can be more driven by temporary macro-factors like interest rates or general investor exuberance than anything related to the company in question.

I’d regard these approaches as crude at best and nonsensical at worst.

To us, a reasonable alternative way to consider the fair value of a company is to back into a shareholder yield that produces an “average” return over time. Said differently, the concept of fair value for a stock is roughly the inverse of what “yield” the stock needs to offer to produce a market return.

For example, assuming equity investors expect to earn 9-10% per year in the stock market (in keeping with long-run averages), then a business that will produce 0% long-term growth needs to pay shareholders a 9-10% cash return (i.e. all of the return will come via yield) to justify its price. This means a “no-growth” stock like this should probably trade for about 10x earnings, or a 10% earnings yield, assuming those earnings can be returned via dividends or buybacks. A business that is not growing AND has to retain earnings is not worth very much at all.

To apply this framework to stocks growing faster than, say, 10%-15%, you’d have to take into account how the multiple will contract as growth slows (trees never grow to the sky). I’m not smart enough to understand the normalized earnings power of businesses like that so I usually don’t try.

Turning back to Lowe’s, let’s say after the next several years the margin expansion opportunity is realized and there is no more opportunity there. Further, same-store sales slow down to 4-5%, representing the company’s long-term growth or compounding rate. Under this scenario, investors should logically demand a ~5% yield to reach our aforementioned 10% annual returns. A 5% yield equates to around a 20x “fair multiple” for Lowe’s (again, assuming the above fundamentals come to fruition, which they may not). This happens to correspond closely to Lowe’s historical 19x median valuation multiple. This strikes me as a reasonable valuation for Lowe’s given its prospects.

I’m not arguing this approach to valuation is perfect, or advocating to totally ignore other techniques. This is not a precise valuation tool (which is why business school professors would cringe reading this), but valuation is not a precise science anyways. To us, it’s about not screwing things up and making sure you have a margin of safety. Backing in to an appropriate yield is at least built from company-specific first principles, designed to keep us out of trouble, and better than the silly relative valuation game so often played in the investing world.

Forward Returns

If Lowe’s can continue reinvesting a portion of its cash flow at attractive rates of return and return the rest to shareholders through repurchases and a modest dividend, the business is likely to generate low/mid-teens annual per-share returns, which is pretty good. The stock trades for around 15x forward earnings, a reasonable (but not drastic) discount to my assessment of fair value.

The modest valuation discount is likely due to the current uncertainties in the housing markets driven by interest rates, as well as the unwind of a COVID period when Lowe’s and other home retailers were over-earning somewhat. Near term uncertainty doesn’t bother me and it often creates an opportunity for those willing to shoulder a year or two of noisy returns before a business resumes its march upwards. Plus, I doubt Lowe’s will prove to be as cyclical as some think given its predisposition to maintenance & repair work and the under-penetrated Pro segment, but time will tell.

If the stock re-rates to its historical (and fair) ~20x multiple over the next five-ish years, investors could add another 5-6% of annual returns to the already solid business returns.

Home improvement retailing is a mundane business. Lowe’s is not some sexy stock that is going to win anyone an award for the most creative investment pitch at the Sohn investment conference. But oftentimes boring is beautiful, and remember; in investing there are no points for difficulty.

Do you have a “stranded” 401k from a past job that is neglected and unmanaged? These accounts are often an excellent fit for Eagle Point Capital’s long-term investment approach. Please contact us to learn more about opening a separately managed account with EPC.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

I love your point regarding “Near term uncertainty doesn’t bother me and it often creates an opportunity for those willing to shoulder a year or two of noisy returns before a business resumes its march upwards.”

I’d say for myself many of my best investments were made where I could purchase ownership in a business at an attractive price and was fine with a couple years of subpar returns due to short-term factors since I could see the long term compounding potential of the business.

The crazy thing to me is the average investor holds a stock for only ten months which undoubtedly should provide a substantial advantage for those of us looking to own (not simply “invest in”) high quality businesses over the long-term.

Outside of earnings multiples I think it’s important to look at net-income to FCF conversion rates. I’m sure you’ve seen it before but there are some businesses I’ve seen that simply retain a lot of earnings without much to show for it. It seems like some lower quality businesses just need to reinvest a lot of their earnings just to stay in the same place let alone grow. It’s quite a weird phenomenon and almost feels like phantom earnings. I’m not sure how much of this is accounting trickery to inflate earnings as well.

I really liked how you analyzed the retained earnings within Lowe’s and then broke down how the capital was allocated and the return on reinvested earnings. I’m definitely going to use that technique in my own analysis in the future.

I’m not sure what the scale of the capital managed by EPC looks like, but I’m curious what your thoughts are regarding leveraging size as an advantage to drive investment outperformance. When I was at the Berkshire Hathaway shareholder meeting last weekend I was thinking a lot about this when looking back at many of their earlier investments like Sees Candy, etc. and the amazingly low valuations they paid for many businesses along with their current size problems making it hard to find uses for excess cash that really move the needle.

It made me think that there might be more poorly valued or priced assets within the lower market capitalization companies so I’ve been focusing more on that area lately versus on analyzing large cap companies like Lowe’s, etc. Intuitively it just feels like there might be more opportunities and less competition there for a smaller investor such as myself and I’d like to leverage every possible advantage at my disposal.

Thanks for the write up Dan!

1. Why do you think that HD has better SG&A as a %Sales? They don't discriminate SG&A in their 10K's.

2. "Turning back to Lowe’s, let’s say after the next several years the margin expansion opportunity is realized and there is no more opportunity there." Which margin do you mean? Gross or EBIT? If it's EBIT, I'd love to know why.

3. To end, it's been hard to find outlets for the retained cash, which makes me think that the real reinvestment rate is more close to 0% than 25%. Do you see the reinvestment outlets and amounts?

Take care!