Interest Rates and Valuations

Some thoughts on the relationship between interest rates and stock valuations, and what investors can do about it.

For years economic forecasters, investors, and the media have been harping on high stock market valuations. Many have continuously clamored for a correction or a crash with the market trading at close to record-high valuation multiples while marching higher seemingly every year. On the other hand, famous investors including Buffett, have said that stocks look cheap if interest rates stay where they are. In 2017 Buffett went so far as to say:

“If I could only pick one statistic to ask you about the future before I gave the answer, I would not ask you about GDP growth, I would not ask you about who was going to be president… a million things I wouldn’t [ask],” he continued. “I would ask you what the interest rate is going to be over the next 20 years on average. The 10 year [Treasury note yield] or whatever you wanted to do.”

Obviously future interest rates are important. They’re also not knowable. That said, it makes no sense to comment on stock valuations without regard to present interest rates. Here I’ll share our thoughts on why interest rates matter so much for valuations, what changing interest rates might mean for stock returns, and how we deal with this important unknown.

In investing, interest rates are important for two main reasons.

From an academic standpoint, a business, or any investment, is worth today the summation of however much free cash flow it will generate over its lifetime discounted at an appropriate rate. In general, current interest rates serve as a benchmark for discounting future cash flows, and the lower the interest rate used to discount the cash stream, the higher the value of that cash stream in today’s dollars. So, when interest rates drop, investors presumably use a lower discount rate in their discounted cash flow analysis of businesses, and subsequently assign higher valuations to stocks. This is especially true for growth stocks where a lion’s share of earnings come in future years.

While this is technically correct, it is a bit esoteric to part-time investors and the broader market. A more practical reason as to why interest rates are so important is because they serve as a starting point for expected risk and return tradeoffs. Consider the below graphic, known as a risk curve or capital market line.

Source: 2020 in Review (Howard Marks)

All assets in financial markets have some level of risk. Different investments that offer different levels of risk and return are weighed against one another. The safest investments, which are largely risk-free, are government bonds, or Treasurys.

The return on Treasurys is so important because it serves as the starting point for risk tolerances, and expected returns, against which other options are weighed. For example, if the yield on a 10 year US bond pays 5% per year with zero risk, no sane investor would by a riskier asset, like a common stock, with an expected return below 5%. In turn, investors will demand more from speculative stocks than safe stocks, more from private equity than from risky stocks, and so on. As you move out on the risk curve, expected returns have to be higher to justify taking on more uncertainty. The extra expected return is referred to as a “risk premium”. The lower the risk premium demanded, the less prudence investors are taking.

When Treasurys offer close to zero return, like nowadays, investors are willing to accept lower returns than in the past on riskier assets, which means paying higher valuations. One might think of this as the whole risk curve shifting down. As always, Howard Marks summarized this relationship well in an October 2020 memo, saying (emphasis his):

“Most decisions in investing are relative decisions. Investors try to find the most attractive opportunity so as to be able to achieve the highest risk-adjusted return. Thus a great deal of the selection process is comparative. “I’m considering buying X. How does its risk/return proposition compare with the one on Y?” That means the lower the return is on Y, the less X has to offer to be the superior investment. And if X is to offer less return, the way it gets that way is through an increase in its price. Thus, assets and asset classes are inherently interconnected. Money moves from one asset class to the next in search of the best bargains, which get bought up until they’re at equilibrium with everything else. Changing the risk-free rate has the potential to reset the returns on everything.”

In 2000 investors could earn around 6% annually from owning 10 year Treasurys. Today the yield on the 10 year is just 1.5%. Clearly the risk curve has “moved down” over the years. So, what does that mean for stock valuations?

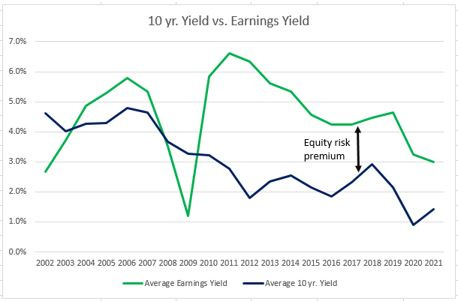

Because it serves as the yardstick for all investments, the most helpful way to view stock market valuations is in conjunction with US Treasurys. The best way to do this is compare the earnings yield in the stock market, or an individual investment, to the yield on the 10 year. Earnings yield is simply the inverse of a P/E ratio. Earnings yields in excess of the 10 year yield can be thought of as the current risk premium investors demand from owning stocks instead of risk-free bonds. Here’s how that trend has looked over the last 20 years.

Source: Author, Factset, Multpl.com

The chart depicts the inverse of the S&P 500 trailing P/E ratio compared to average 10 year US Treasury yields. The risk premium is simply earnings yields minus Treasury yield. As you can see after the financial crisis, investors demanded a big risk premium as fear was rampant amongst capital markets participants. In other words, the market was very cheap.

Author, Factset, Multpl.com

Over the past two decades the median risk premium for the S&P 500 has been around 200 basis points compared to the yield on 10 year Treasurys.

Today, the markets trades for around 30x the last 12 months earnings, or an earnings yield of ~3.3%. This is high in an absolute sense, only surpassed in the early 2000s (and for one year in 2008 when earnings tanked during the financial crisis). Valuations do not look nearly as dramatic, however, when compared to interest rates.

Presently, relative valuations for the S&P sit near the long-term average with an earnings yield of 3.3% and the 10 year yielding 1.5%, or a risk premium of around 1.8%. For simplicities sake and to allow for apples-apples comparisons, I did not adjust for COVID-19 impacts which are still reflected in many companies trailing financials. In all likelihood the trailing PE ratio is somewhat distorted to the high side. On the other hand, many businesses experienced a COVID boom which is unlikely to continue, which would also have to be adjusted for. Nonetheless, the conclusions don’t change much if you look at forward earnings. Over the last 20 years the risk premium on a forward basis has been 300 basis points; almost exactly where the market trades today (forward earnings yield of 4.7% against 1.5% 10 year yield).

In the early 2000s, valuations were higher, and interest rates were dramatically higher. In 2001 the market traded at 35x earnings with interest rates over 5%, or a risk premium of -2.1%. In other words, stocks got so expensive relative to interest rates that the risk premium in the S&P 500 went negative. It’s for this reason that comparing today’s stock market valuations to the early 2000s makes little sense without commenting on interest rates. When looked at through this lens it is reasonable for investors to conclude that stocks don’t look overly expensive with interest rates so low.

Proclaiming that the market doesn’t look as expensive as the early 2000s when factoring in interest rates does not mean investors should be jumping for joy. Importantly:

· What happens if interest rates don’t stay at historically low levels in perpetuity?

· What might that mean for expected returns?

· Is there anything investors can do about it?

While stock valuations given present interest rates are not overly stretched, what really matters is future interest rates, as those will drive future market valuations, which is what investors ultimately care about. Unfortunately, I have no unique insight into what future interest rates will be. Two approaches are helpful for me in dealing with this ambiguity.

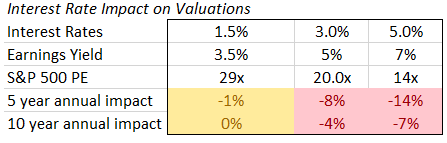

First, it’s important to understand the range of potential outcomes should interest rates rise. I like to think in 5 and 10 year increments. Below is a table that shows an illustrative annual valuation compression impact at a variety of interest rates over five and ten years. It assumes an equity risk premium of 2% in line with the past few decades.

Source: Author

So, if interest rates stay very low, valuations are unlikely to compress much. If they roughly double to 3% over five years, it could provide a near double-digit annual headwind for the market to overcome. The last time the 10 year yield averaged 3% for the year was 2010 - a while ago, but not a lifetime ago. If earnings and dividends produce the historical 6-8% return and interest rates rise to 3%, most or all of the stock market’s return could be wiped out by valuation compression. This is largely why the S&P 500 was flat from 2000 – 2010.

This is by no means a prediction or an alarm bell, and don’t be fooled by the false precision of a table filled with percentages. As I’ve said, I have no idea where interest rates are going. I certainly don’t foresee the fed raising rates to 5% overnight, but other than that it’s tough to say. Also, the risk premium demanded by investors may change from its current or long-term norm. This exercise is meant to understand a range of outcomes that might be reasonable and should help frame expectations for index investors. What I can say is: interest rates seem more likely to rise than fall and I wouldn’t bet on continued multiple expansion for the S&P 500 to drive outsized returns that have persisted since 2010. At the very least, it’s safe to say that prospective returns are lower than they have been in recent years given this asymmetric risk to the downside. Knowing these potential headwinds, what are we doing?

The best way we know how to contend with an important but unknowable variable, like future interest rates, is to prepare rather than predict. Fortunately, our investment style is suited for situations like this. First and foremost, buying good companies at an attractive absolute, not just relative, valuation, affords us the opportunity to earn solid returns with a margin of safety against declining general valuation levels.

Consider McKesson, which trades for around 8x free cash flow, or an 11% earnings yield (compared to 3% for the S&P). If general valuations compress, there is only so much lower a free cash flow machine like McKesson can logically trade for any extended period. Let’s say McKesson’s valuation drops to 6x free cash flow over five years. The business would be priced at a 16%+ earnings yield and likely growing at mid-single-digits regardless of interest rates. This means the business would be producing a 20%+ annual return, more than offsetting any impact from a valuation de-rating.

A reasonably low starting valuation for a well-positioned and free cash flow generative business puts a floor under further valuation declines because so much of the market cap can be returned to shareholders in cash each year. Better yet, should interest rates stay low, McKesson will have no problem producing solid returns. Not many businesses meet the description above. Fortunately, there are enough to fill a concentrated portfolio. McKesson is one of several examples like this in our portfolio.

In addition to focusing on maintaining valuation discipline, we buy businesses that are growing in a predictable manner thanks to enduring competitive positions. Predictable growth means our businesses do not rely too heavily on any one extrinsic factor – interest rates, commodity prices, employment rates, etc. – to continue growing earnings at an above average clip. As we wrote in our recent investor letter, we prefer businesses in replication mode with a proven and simple growth algorithm. By relying on business return, rather than a valuation re-rating, to earn the bulk of our returns, we sleep well at night knowing we don’t need declining interest rates to provide a tailwind to valuations. Should the valuations of our company’s rise, which we think is likely, it provides a cherry on top of already solid returns.

Finally, we’ll never make a binary bet on an unknowable variable like interest rates. We have our opinions on what we think will happen, but we don’t let them guide our investment decisions. By keeping our heads down and owning simple, predictable, and profitable enterprises at reasonable prices, we relieve ourselves of the burden of watching which way the 10 year yield is moving on a daily basis. We think more investors would be well served by doing the same.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

Hey Dan - great article, you touched on a few extremely interesting points regarding measuring values relatively rather than absolutely, and I think in current market conditions that's extremely important given the higher RFR.

Although using earnings yield would be a fairly quick metric that investors can gauge for a ballpark understanding, for true valuations I'd argue that earnings isn't an effective measure of current market conditions. Earnings can be quite volatile and sector dependent, and can appear high/low given short term market conditions/moods, it ignores risk and isn't a forward looking measure, and doesn't take into account future growth prospects of the S&P.

In terms of traditional valuation, I've found it much more useful to estimate the IRR of the S&P 500 using the discount rate that would be needed to discount future cash flow projections of the S&P back to the current value. This value uses a variety of assumptions regarding growth, but are taken directly from analyst assumptions and published values (dividends/buybacks and earnings projections to measure cash flows, analyst assumptions regarding growth of cash flows, and terminal rate equal to the risk free rate). By discounting these cash flows back to the present and equating it to the current value of the S&P, we can estimate the IRR (as the discount rate), and subtract the RFR from this value to get the implied equity risk premium.

This value should be updated monthly, to account for changes in projected cash flows and earnings/dividends projections, as well as changing interest rates. This method is forward looking and dynamic, and I'd argue that it's a much better measure of implied equity risk premium. Completely understand that this article was very general in a sense of getting a ballpark estimate of current premiums, but just wanted to share my thoughts. Once again, very interesting article and very well written, and love your work.