Independent Thinking (An Excerpt From Our Recent Letter)

The following is an excerpt from our spring 2025 investor letter. Premium subscribers will receive a full copy of our investor letter, including a description of every position we own and why we own it, in 45 days (May 15, 2025).

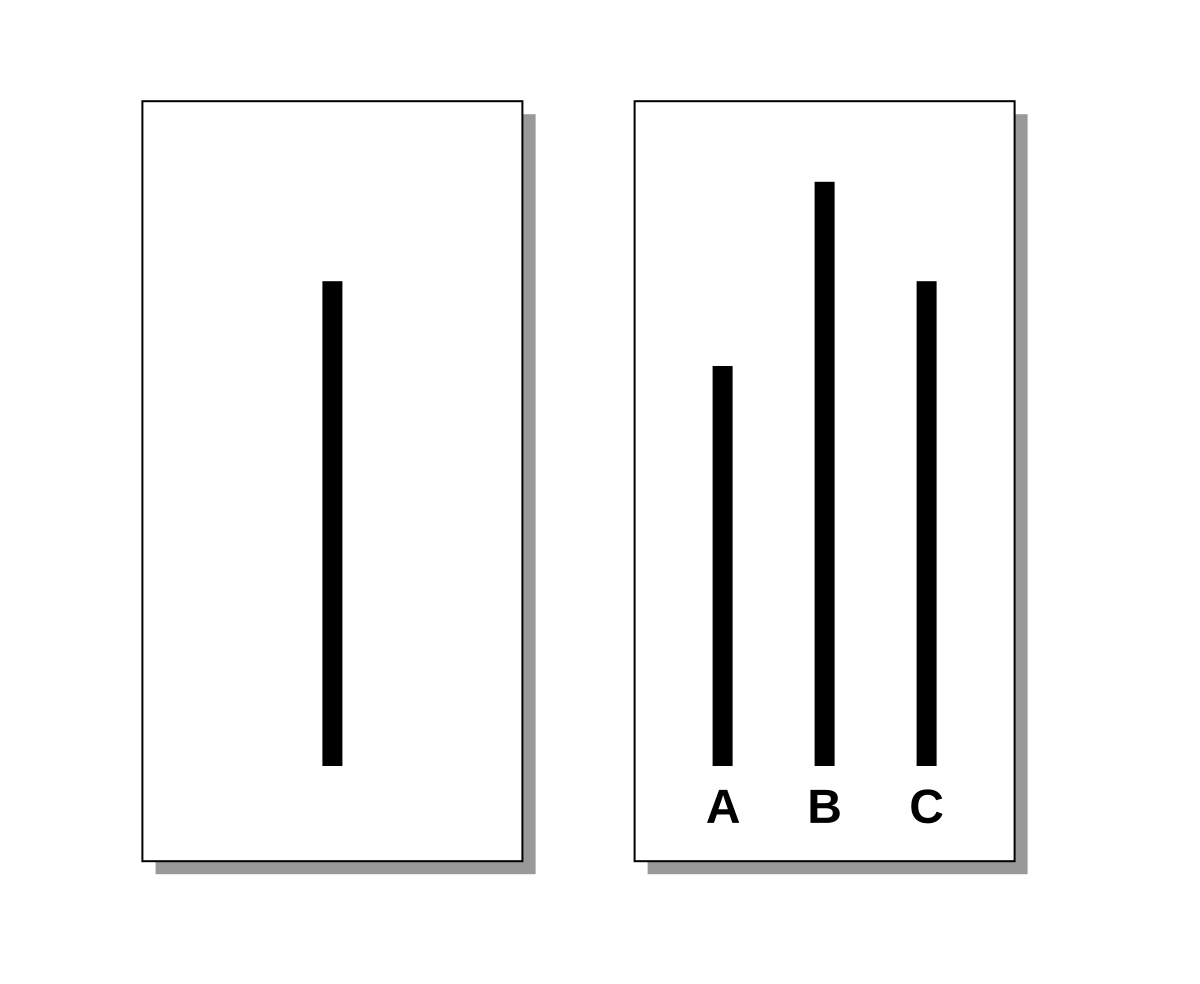

In the 1950s, Solomon E. Asch of Swarthmore College conducted an unusual psychology experiment. He gave students two cards. One had a reference line. The other had three comparison lines. Students were asked to match the length of the reference line to one of the comparison lines. One of the comparison lines was a perfect match. The other two were off by more than 50%. Students could move the cards side by side to measure.

In the control group, students matched the lines in private. Their error rate was 0.7%. Virtually everyone got it right, every time.

The experimental group completed the task in groups of eight. The students took turns reporting their answer out loud in front of the group. The catch was that seven of the students were confederates planted to deliberately say the wrong answer. The lone independent student, always sitting in the fifth chair, was the real subject of the experiment.

The presence of the confederates increased the error rate from 0.7% to 32%. 75% of the test subjects conformed to the confederates and gave the wrong answer at least once. Only 25% remained independent the whole time.

Asch’s experiments showed people often abandon their own judgments to align with group consensus, even when the group is clearly wrong. Test subjects knew the correct answer but feared social rejection.

In 1962 the TV show Candid Camera tested Asch’s findings in the real world. In the “Face the Rear” episode unsuspecting individuals entered elevators where actors faced the back wall instead of the doors. Host Allen Funt wanted to see if subjects would mimic this nonsensical behavior. Most participants gradually conformed, facing backward despite confusion.

A preference for conformity – what psychologist Robert Cialdini termed “social proof” – is hard-wired into the human genome, and for good reason. Early humans would know fruit was safe if they saw others eating it. Conformity can still help us navigate the modern world. If you see everyone running out of a building, you should follow because there might be a fire.

One place conformity cannot help is financial markets. In “The Psychology of Human Misjudgment” Charlie Munger says that humans are prone to make mistakes when they’re subject to social proof and that the effects are heightened by uncertainty and stress. Financial markets check all of these boxes, making them a perfect breeding ground for misjudgment.

As stock market investors, we often feel like we are sitting in Asch’s fifth chair. Watching others get rich off of cryptocurrencies or the AI boom triggers our instinct to conform and join the crowd. Likewise, fear over tariffs and uncertainty in Washington triggers our instinct to run for cover and hunker down.

Investor Seth Klarman once wrote that “Value investing is at its core the marriage of a contrarian streak and a calculator.”

A contrarian streak is a willingness to go against the prevailing market trends or popular opinion. Investing is not as simple as “always be contrarian.” Investors must be contrarian, and right. Being right is more important than being contrarian. The market is competitive and usually (but not always) efficient. Investors need to pick their spots carefully.

That’s where a calculator comes in handy. Klarman’s calculator is a metaphor for a quantitative and analytical mindset. Emotions, political allegiances, and ego can only hinder investment performance.

One of the lessons the stock market teaches again and again is that it is not what you buy, but what you pay that matters most. Any asset can be an attractive investment if you buy it cheap enough. Any asset, no matter how good or exciting, can be a bad investment if you pay too much.

Our calculator helps to steady our emotions and level our judgement so that we are not swayed by social proof. Our goal is to buy businesses that we think are likely to produce a low to mid teens business return (yield + growth) using conservative assumptions. We want a margin of safety on top of that, in the form of a valuation that we think is more likely to rise than fall. If we analyze our investments correctly (we don’t always) we should continue to earn stock returns (business return + change in valuation) that are mid teens or higher.

This framework best suits simple, predictable, and profitable businesses with modest, but persistent, growth trading at low valuations. Our portfolio is full of these. We like businesses whose futures are likely to resemble their past. They often have low economic sensitivity, minimal exposure to factors outside of their control, a strong enough balance sheet to weather a storm, and the ability to raise prices over time. Coming up with the right numbers to punch into our calculator to value these businesses is relatively straightforward and does not require bold forecasts.

Our framework does not suit companies subject to rapid technological change or companies levered to factors outside of their control, like interest rates or commodity prices. We deliberately avoid highly speculative and uncertain “moonshot” stocks which get all of the attention in a bull market. Technology, by definition, is rapidly changing and hard to predict. Commodity prices aren’t much easier.

Stocks subject to lots of uncertainty are also the most likely to get lots of media attention and become trendy investments. Since their future profits are hard to predict, there’s plenty of room for the bull and bear narratives that pundits, journalists, and TV producers love. Suspense always makes a story more entertaining, and entertainment is their goal.

We’re more interested in profits than entertainment. We like businesses that plod along during the good times and the bad. Our investments may not be sexy, exciting, or trendy, but what they lack in drama, they make up for in earnings. They have strong and strengthening competitive positions and throw off lots of cash. In a strong bull market, they’re unlikely to get much attention or hype and may lag more trendy stocks. They should nevertheless plod along and deliver good returns. In a downturn, it should be much the same.

We call this approach strategic mediocrity. Strategic mediocrity means pursuing merely good results with a focus on consistency and longevity. We’re willing to forego banner years to avoid the blowups that often follow. Our portfolio is unlikely to perform the best, or the worst, in any given year. By racking up merely good results year in and year out, we hope to produce excellent, top-tier long-term results. We believe that we can achieve this if we continue to think independently and choose our investments on the basis of value rather than popularity.

EPC offers separately managed accounts, low minimums, and accepts most account types (including IRAs and 401k rollovers). Qualified Clients can elect a zero management fee structure inspired by the Buffett Partnership. EPC’s clients get complementary access to our premium Substack. To learn more please email info@eaglepointcap.com.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.