Fair Isaac

In 1956 Bill Fair and Earl Isaac hypothesized that a computer algorithm could make better loan underwriting decisions than a handshake and a person’s word. The pair had met at the Stanford Research Institute where they used computers to improve military decision making.

In the mid 1950s, the duo left Stanford and borrowed Standard Oil of California’s computer during off peak hours. They aimed to develop an algorithm that could produce scores that predict human behavior.

Fair and Isaac pitched their algorithm to 50 lenders in 1958, but only one bought it. Slowly, but steadily, Fair Isaac won more clients. Finally in 1975 Bill Fair felt like the company had enough traction to continue living.

Back then, Fair Isaac calculated custom scores for each of its clients. In 1979, they began working on a project to produce standardized scores using the national credit bureaus data (Experian, Equifax, and TransUnion) .

Ten years later, the project was complete. Equifax debuted the first standardized credit score in 1989. By 1991 all three national credit bureaus used them. After Fannie Mae and Freddie Mac endorsed FICO scores in the mid 1990s, they became the gold standard for underwriting decisions.

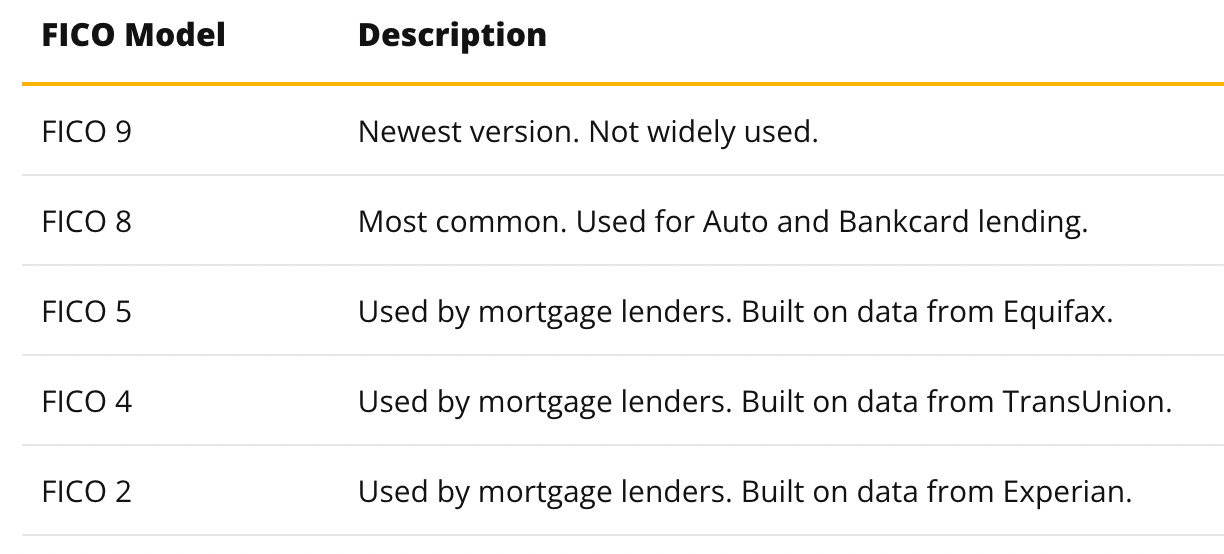

Today FICO scores have 90% market share and continue to be integral to consumer lending decisions. Fair Isaac hasn’t stopped innovating since 1989. There are nine generations of models on the market and several tailored to a specific type of lending.

Scores

Fair Isaac’s Scores segment is one of the great businesses of the world. Scores consists of little more than an algorithm and functions like a royalty on consumer lending.

B2B

Consumers often confuse Fair Isaac with the credit bureaus. The credit bureaus collect data and license Fair Isaac’s algorithm to turn the data into a credit score. The credit bureaus sell the bundled data and score to lenders like J.P. Morgan and Bank of America. The top ten banks consume the vast majority of scores.

Every time a lender needs to make an underwriting decision, they pay Fair Isaac a royalty (via the credit bureaus) for calculating a score. This is Fair Isaac’s B2B (business to business) scores business.

B2C

Fair Isaac also has a B2C (business to consumer) business. Consumers can access their FICO scores via Experian or myFICO.com. The B2C business is relatively new compared to the B2B business. B2C helps increase consumer awareness of FICO scores and further cements FICO as the gold standard of underwriting. Underwriting is most transparent when both parties understand how they’ll be scored.

Pricing Power

Last year Fair Isaac’s Scores segment produced $650 million of revenue and about 10 billion scores. This implies that the average score only costs about 6.5 cents.

6.5 cents is nothing to someone who is considering lending hundreds of thousand of dollars. A FICO score’s low price relative to its value means Fair Isaac has a substantial amount of untapped pricing power. A bank considering lending $300,000 for a mortgage isn’t going to think twice at spending 6.5 cents to get FICO score so long as the score has any predictive value.

Fair Isaac kept the price of their scores static for nearly twenty five years. In 2018 the company renegotiated their contracts with the credit bureaus to allow them to raise prices. Since then they have raised prices, fueling 24% Scores revenue growth in 2021, 25% in 2020, 25% in 2019, and 29% in 2018 — a 26% CAGR.

FICO scores are basically a monopoly and Fair Isaac needs to tread somewhat carefully with its price hikes. Raising prices too fast will only invite unwanted regulatory scrutiny.

Fair Isaac also faces a concentrated customer base. The company deals with the credit bureaus, who act as its distributors. Fair Isaac’s end customers are big banks who are sophisticated enough to know when they’re being taken advantage of. Fair Isaac sells these same banks software, and can’t raise prices too much without getting damaging their software sales.

One obvious question is, why did Fair Isaac suddenly decide to start raising prices in 2018? Undoubtedly the new contract with the credit bureaus catalyzed the price increases. But why hadn’t Fair Isaac renegotiated earlier?

My best guess is that they wanted to invest more aggressively into their software business but didn’t want to lower their over growth or margins. So, they exercised pricing to cover heavier investment elsewhere.

Competition

Fair Isaac is in an unusual competitive position in that its primary competitors are its distributors — the credit bureaus.

The credit bureaus own the credit histories that feed into Fair Isaac’s algorithm. In 2006 the three credit bureaus banded together to create an alternative to the FICO score named VantageScore.

It’s hard to blame them - they own the data and end-user relationships. Why continue paying Fair Isaac a royalty when they could earn it themselves? Though the royalty is small, it’s virtually pure profit. Fair Isaac’s score’s segment has 80%+ margins, according to the company.

Fair Isaac sued the credit bureaus in 2007 but dropped the case in 2011 after rulings favored VantageScore. Nevertheless, VantageScore has not hurt Fair Isaac’s score franchise. FICO scores remain the gold standard and continue to have 90% market share. Why?

FICO scores aren’t expensive enough to encourage a lender to switch.

Lenders have calibrated their systems to FICO scores and won’t risk recalibrating to VantageScore to save a penny or two.

Consumers are familiar with FICO scores. Switching would be like getting Americans to start using the metric system or quoting temperature in Celsius.

Most lenders will use both VantageScore and FICO. For a few pennies, why not? Lenders always use all of their available data, both in-house and from the credit bureaus.

3In August, the Wall Street Journal suggested that lenders are moving away from FICO scores. As proof, the author cites that Synchrony Financial, the largest issuer of store credit card issuer, has completely moved away from using FICO scores. The author also suggested that JP Morgan and Bank of America have de-emphasized FICO scores in their underwriting.

Fair Isaac countered that Synchrony had been working to remove their dependence on FICO scores for five years, that it wasn’t a surprise, and was a one-off event. Fair Isaac isn’t aware of any other large lenders moving away from FICO like they were with Synchrony.

Further, Fair Isaac hasn’t seen any evidence that lenders are consuming fewer FICO scores in aggregate. Fair Isaac gets paid the same whether a lender relies completely on a FICO score to underwrite, or uses it alongside VantageScore. Similarly, Moody’s and S&P both make good money in bond ratings because bond investors want both ratings. Neither rating is expensive enough to force investors to chose one.

So long as FICO scores carry some value, they’ll continue being used. Synchrony demonstrated that moving away from FICO and recalibrating is a multi-year process that few will be excited to undertake. Still, Synchrony also proved that life after FICO is possible, and it is something Fair Isaac should watch.

FICO XD

FICO scores may be the gold standard, but they’re not perfect. There are roughly 50 to 60 million Americans who do not possess a scorable credit history. Without a FICO score, these people can’t access credit to build a scorable credit history. It’s a chicken-or-the-egg problem.

With 90% market share, FICO has every incentive to increase demand for scores by expanding the scorable population. FICO XD, or “Extra Data”, uses alternative payment data from telecoms, mobile phones, and utilities to produce a FICO score.

Fair Isaac has found that once previously unscorable people have a FICO XD score, they gain access to credit and rapidly progress to where they can have a traditional FICO score. FICO XD is an ideal on-ramp to the financial system for those without meaningful credit histories.

VantageScore claims that it can score several million more people than FICO can. However, both algorithms rely on the same underlying data. The difference is where each algorithm draws the line between signal and noise on data quality. FICO is more conservative, while VantageScore takes greater liberties.

Cyclicality

Fair Isaac’s Scores revenue is affected by volume, which waxes and wanes with the strength of the U.S. economy. Periods of faster growth present lenders with more underwriting questions they use FICO scores to answer. Since Fair Isaac already has 90% market share and the market isn’t growing much, volumes are steady but cyclical. The B2C business could prove less cyclical as consumers may keep a closer eye on their FICO score during tougher times, but that’s yet to be seen. The B2C business didn’t exist during 2008-2009.

Software

Although most people associate Fair Isaac with credit scores, the company thinks of itself as an analytics company. In their own words:

We are good at predicting consumer behavior based on data and then taking that, turning it into decisions, which we then incorporate into workflows for companies that want to optimize their interactions with consumers.

Source: Barclays Global Technology, Media and Telecommunications Conference, 2018-12-5

Fair Isaac’s software business has five franchises that follow the lifecycle of a financial services customer:

Customer Acquisition Marketing

Originations

Customer Management

Credit Card Fraud Detection

Collections and Recoveries

Fair Isaac’s strongest franchises are in customer management and fraud detection, where the company is #1.

Transition To The Cloud

Fair Isaac has been selling software to banks since the late 1970s. Historically, it was on-premises software for things like lending, originations, collections, and customer management. Around 2012 Fair Isaac decided to move their software to the cloud.

As they started transitioning to the cloud, they decided to take the project a step further and build a decision-making platform for optimizing business’s interactions with consumers.

According to Fair Isaac, what makes it a platform is that its decision-making software has a unified codebase and common tools that can be run on-premise or on the cloud (e.g. on top of AWS).

Fair Isaac wants to bring its five software franchises into a platform so that:

A big enterprise customer can buy our platform once, do the plumbing for the data once and then having brought all the data in, that it wants to be able to operate on apply wide range of analytics and then put it into operations.

Source: Fair Isaac Corp at Barclays Financial Services Conference 2021-9-13

Right now, most of the APIs are built by Fair Isaac’s engineers for the company’s enterprise customers. Over the next 2-3 years, Fair Isaac expects to start seeing its customers and independent third parties start building their own APIs on top of Fair Isaac’s platform.

Fair Isaac has deliberately transitioned slowly to the cloud. Today the transition is about 60% complete with three of the company’s five software franchises transitioned.

Margins

If Fair Isaac’s Scores segment is like a royalty on American lending, then its Software segment is more like a start-up. While the software segment account for 50% of revenues, it only produces 10% of Fair Isaac’s operating income.

Fair Isaac has been diverting profits from Scores and reinvesting them in Software for several years. Heavy reinvestment through the income statement has depressed Fair Isaac’s margins. These investments are mostly optional, however, and done in pursuit of growth. Theoretically, Fair Isaac could cease reinvesting and coast on the strength of its Scores business for years to come. That’s why Fair Isaac’s CEO said:

To any shareholder or prospective shareholder who asked me that question, I turned around and I say, "What would you like our margins to be? Because we can do that."

Source: Barclays Global Technology, Media and Telecommunications Conference (2018-12)

Software companies tend to have high upfront fixed costs that produce operating leverage down the road if they’re successful. Since Fair Isaac is investing in its software business through the income statement, not the balance sheet, the Software segment’s operating margins are a good indicator of its health.

NOTE: The Pro Forma margins allocate Fair Isaac’s unallocated corporate costs pro rata based on revenue.

Fair Isaac runs its Software segment to flat year-over-year margins. They’ve stated that they don’t want their margins to go down, but don’t expect them to inflect upward for five years.

Fair Isaac keeps margins flat despite growing software revenue because they continue to invest in their income statement. They’re constantly on the lookout for new tech to acquire, but typically decide that it’d be cheaper to build it in-house rather than acquire it externally. So, they hire more engineers and increase their R&D spending to build it, which shows up as an expense on the income statement.

The question we ask ourselves is, "Do we like that businesses as much as we like our own?" And over and over and over, the answer is, no, we'd rather buy back our own stock, invest in our own business than go buy that business because the long-term prospects for this business are better than that one.

Source: Barclays Global Technology, Media and Telecommunications Conference (2018-12)

Capital Allocation

Despite heavy investment in the Software segment, Fair Isaac continues to produce substantial free cash flows. The company primarily uses its cash to repurchase its own shares. Over the last fifteen years Fair Isaac has cut its shares outstanding in half.

In their own words:

We think of ourselves as kind of a "go private publicly" organization. We're an LBO for the benefit of our public shareholders. So we've levered up somewhat. We usually run somewhere north of 2 and south of 3x EBITDA leverage. It could be higher than it is today, but we want that to be healthy.

Source: Barclays Global Technology, Media and Telecommunications Conference (2018-12)

Part of me wonders if Fair Isaac would be better off as two separate companies. By spinning off its software business, Fair Isaac could more readily exercise its pricing power. The company wouldn’t need to worry that higher scores pricing would hurt the their software segment.

A spinoff would also help build awareness for the software business and allow it to find its own dedicated investor base. The market price of Palantir and C3 AI suggest there’s no lack of enthusiasm for AI decision-making stocks.

That said, Fair Isaac relies on profits from its scores business to reinvest in its software business. This may be diworsification, but only because Scores is such a good business, not because software is a bad business. Companies like Palantir and C3 AI aren’t profitable yet and depend on the capital markets for financing. Fair Isaac doesn’t have to, it has Scores. In a downturn where external financing dries up, this could be a competitive advantage.

Forward Returns

Fair Isaac’s stock grew ten fold between 2005 and 2020. However, such stellar performance will be hard to replicate over the next fifteen years. While Fair Isaac is a wonderful business, it might me a mediocre investment at today’s price.

The table below deconstructs Fair Isaac’s stock performance. It gained 2.5x from P/E multiple expansion, 2.2x due to share repurchases, and 1.9x due to earnings growth. Multiplying those produces the stocks 10.6x appreciation.

Between 2005 and 2014 Fair Isaac traded for 12 to 25 times earnings. At those prices, the company was able to repurchase a ton of shares. Since then the stock’s P/E multiple has grown to 46x. Such a high multiple reduces the effectiveness of share buybacks. I wouldn’t bet on continued multiple expansion and would actually anticipate some multiple contraction. Multiple contraction will prove a headwind, rather than a tailwind, to the stock over the coming years. Further, the longer Fair Isaac’s multiple stays elevated, the less value its buyback program generates.

Fair Isaac’s stock peaked in late July and has since fallen over 30%. Today it trades for about 30x earnings. I don’t think this price affords enough of a margin of safety to make it an interesting investment.

The scores business is one of the best businesses I’ve ever analyzed, and will probably continue to carry the company for the next five years. In five years, Fair Isaac expects software margins to be higher. In the long term, Fair Isaac thinks its software margins will be dramatically higher. If that pans out, the stock can do well from here. But, the company’s software business doesn’t seem to be deeply in replication mode yet.

Fair Isaac’s scores business reminds me of See’s Candy. They can raise prices faster than inflation, but can’t grow their volumes meaningfully. Profits from Scores will be reinvested in Software, which may or may not pan out, and into buybacks, which produce a 3% yield at 30x earnings.

Value Line estimates that the median stock trades for 19x earnings. I’d be more interested in Fair Isaac if it traded below there. Then I’d know I was getting a clearly above-average business at a below average price. At 30x, the risk of multiple contraction, software margins not materializing, and low yields on buybacks seem too great to ignore.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

Nice writeup. Getting interesting