Facebook's Network Shows No Signs Of Cracking

Good investments often hinge on one key question. That question is like a fulcrum the stock teeters over. As opinion wavers, so does the stock. This volatility is value investors' opportunity.

Facebook's stock is down nearly 40% from its all-time high. The market is clearly grappling with uncertainty. You can't go far without hearing about a new Facebook scandal or rage over its privacy policy.

There have been so many that the Tech Republic put together a handy timeline to catch you up on them.

It's easy to lose sight of the signal amidst so much noise. I'm not here to dismiss these scandals or play down their significance. Instead, I'm here to argue that for long-term investors, the most important question to ask is whether Facebook's network will remain intact.

My opinion is that it certainly will and that Facebook is an attractive investment at today's price.

The Great Salad Oil Swindle

In Dear Chairman, Jeff Gramm writes:

In June 1960, an anonymous tipster called American Express to expose a massive fraud at Allied Crude Vegetable Oil Refining Corporation. At the time, Allied was the largest customer of American Express's field warehousing subsidiary, which was in the unenviable position of having guaranteed millions of dollars' worth of Allied's soybean oil inventory.

The tipster, whom American Express employees called "the Voice," said he worked the night shift at Allied's facility in Bayonne, New Jersey. He challenged American Express employees to inspect Tank No. 6006, one of the largest tanks on the property. He explained that there was a narrow metal chamber filled with oil positioned directly under the measuring hatch. Everything else in the tank was seawater.

Allied Crude Vegetable Oil was supposed to have 1.8 billion pounds of oil as collateral against loans, but only had 110 million pounds. American Express' (NYSE:AXP) stock dropped 40% and lost $125 million in market value (source). The market didn't think American Express could make good on the loans and expected it to go out of business.

In The Snowball, Alice Schroeder writes:

"So every trust department in the United States panicked," recalls Buffett. "I remember the Continental Bank held over 5 percent of the company, and all of a sudden not only do they see that the trust accounts were going to have stock worth zero, but they could get assessed. The stock just poured out, of course, and the market got slightly inefficient for a short period of time."

While investors focused on the scandal and panicked, Warren Buffett looked for the signal amidst the noise. He knew American Express was a wonderful business: it earned high returns on its capital and could reinvest large amounts at equally high rates. American Express was the prototypical "compounding machine."

Although the press was crucifying American Express, Buffett noticed that people didn't stop using their cards at restaurants or in stores. Many expected consumers to abandon their American Express charge cards. But this wasn't happening.

Buffett's key insight was that so long as consumers continued to have faith in their charge cards, the company would survive. American Express would take a one-time financial blow to settle its outstanding claims, but this would shortly become a blip on the radar once AXP resumed compounding.

Buffett put 40% of his investment partnership in American Express at $35 per share. American Express eventually settled with the salad oil claimants for $32 million and three years later the stock stood at $70 per share (source).

Facebook

American Express made mistakes and so did Facebook. Its user data was compromised, and investors fear users will walk away from the platform. But this isn't happening.

Like American Express, Facebook is a "compounding machine." It earns high returns on its capital, benefits from operating leverage, and can reinvest at high rates. Facebook also has deep pockets - a cash and securities position of over $41 billion ($14 per share). To borrow a phrase from Charlie Munger, the company is "drowning in cash."

I can't pinpoint what the consequences of Facebook's scandals will be. FB may pay fines, it may pay higher taxes, and it will be subject to more regulations. But Facebook's business model is so powerful and so effective that as long as its network remains intact, the stock will continue to compound.

Evaluating Facebook's Network

A network effect occurs when a product or service gains value as more people use it. Facebook fits this definition perfectly.

The more of your real world friends and family have Facebook accounts, the more valuable it is for you to join the network. This increases value for your friends in a positive feedback loop.

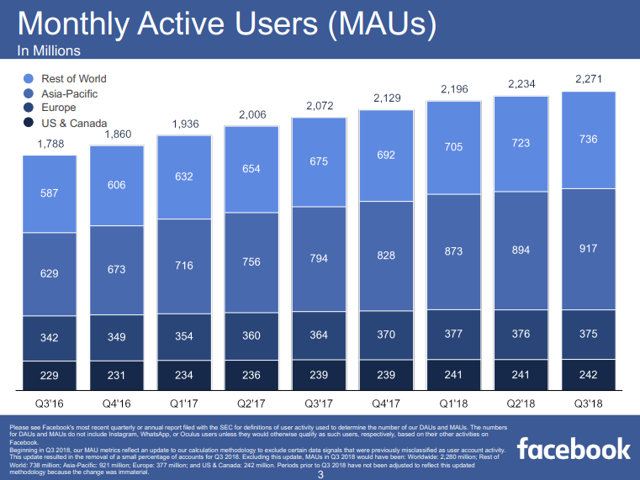

A simple barometer of Facebook's health is the size of its user base. Facebook uses Monthly Active Users (MAUs) as a proxy for this.

Source: Facebook's 2018-Q3 Earnings Slides

MAUs across the world were up 1.7% last quarter and 9.6% over the last year. Europe was the only geography to show a decline, which was a modest 0.5% since its 2018 Q1 peak.

Facebook attracts users who want to interact with other users, and advertisers who pay for the privilege to interact with users. The more interaction Facebook has on its platform, the more attractive advertisers find it. Facebook uses the ratio of Daily Active Users (DAUs) to MAUs as a proxy for user engagement.

Source: Facebook's 2018-Q3 Earnings Slides

User engagement has been steady for the last eight quarters at 66% while DAUs have continued to increase worldwide. Europe is again the lone exception, showing a 1.4% decline in DAUs over the past two quarters.

What's Going On In Europe?

In Q2, Europe's General Data Protection Regulation (GDPR) went into effect. GDPR requires users to explicitly opt-in to continue using Facebook and explains the loss of some users.

Zuckerberg commented on the Q2 earnings call:

GDPR was an important moment for our industry. We did see a decline in monthly actives in Europe - down by about 1 million people as a result. At the same time, it was encouraging to see the vast majority of people affirm that they want us to use context - including from websites they visit - to make their ads more relevant and improve their overall product experience.

That the vast majority of users explicitly opted in to Facebook is a strong vote of confidence in the network's value.

A recent study aimed to examine exactly how much people value Facebook. Since the service is free, putting a dollar value on the service is difficult. The researchers used real auctions to determine the price at which someone would be willing to deactivate their Facebook account for one year. The results revealed users would want more than $1,000 to give up Facebook for a year. This speaks to the stickiness and value of Facebook's network.

The dip in European DAUs is not without precedent, either. Facebook saw its DAUs dip once before in North America. They were quickly recovered the next quarter. Some saw this as the beginning of a decline, and extrapolated the trend out. Instead, mean-reversion took over and restored the users.

Jason Zweig has argued that mean-reversion, not extrapolation, is the most powerful force in finance:

"From financial history and from my own experience, I long ago concluded that regression to the mean is the most powerful law in financial physics: Periods of above-average performance are inevitably followed by below-average returns, and bad times inevitably set the stage for surprisingly good performance."

The point is that Facebook's user base does fluctuate, and it's nothing to panic over. The vast majority of Facebook's users explicitly opted into the service, which is a strong vote of confidence in the network's value.

There is no quantitative reason to believe Facebook is failing to maintain and attract users.

Multi-tenanting

Multi-tenanting is well described by Li Jin and D'Arcy Coolican of Andreessen Horowitz in their article 16 Ways to Measure Network Effects:

We've often observed that if a company is able to replicate a network, it can also layer on functionality that can obviate the need for another product. Even if it doesn't wipe out the target company, such multi-tenanting can reduce usage and compress margins for all competitors. A marketplace for dog walkers and pet owners, for example, has the opportunity to move into pet health or food or other adjacent products, given it has built a network of pet owners from the core business. Facebook developed ephemeral Stories and added this feature into their various apps, including Instagram, in turn stymying the growth of Snapchat.

In a nutshell, when the users of two networks overlap, the larger can replicate the smaller and offer its users one-stop shopping.

Facebook is the largest social network in the world (source) and therefore has the most potential to benefit from this.

Currently Facebook is adding Stories, which is similar to Snapchat (NYSE:SNAP). IGTV is taking on YouTube (NASDAQ:GOOG) (NASDAQ:GOOGL), and Facebook Dating will take on Tinder. Snap and Match Group (NASDAQ:MTCH) have a combined market cap of over $17 billion, to ballpark the size of the potential opportunity.

These are low-risk, high-reward bets for Facebook to make. I don't expect them all to be home runs, but do expect them to add value.

The poster child of multi-tenanting is Tencent's (OTCPK:TCEHY) WeChat.

Source: The Economist

In China, WeChat combines a messenger, like WhatsApp, with a social network, ride-sharing platform, payments, and gaming, among others. The graphic above shows how many features WeChat has compared to Facebook and how much it is able to monetize features Facebook has yet to. I'm not predicting that Facebook becomes the American WeChat. I present it to illustrate Facebook's potential.

Investing For The Future

After Buffett bought his stake in American Express, he pushed the company to allocate its capital towards liberally compensating the defrauded parties. The other shareholders opposed him. They looked for a legal loophole to dodge responsibility. This might have saved American Express a couple of bucks in the short run, but who would trust American Express's guarantee the next time?

The long-run value of American Express lay in the trust consumers had in its franchise. American Express could compound capital at such high rates that protecting this brand was worth millions of dollars.

The same can be said of Facebook.

Facebook must do everything it can to maintain its users' trust. Sheryl Sandberg's latest mea culpa shows the company understands this.

Without users' trust, its network and business will unravel. There are no signs of this happening yet, but Facebook cannot afford to take any chances.

Mark Zuckerberg has the most to gain and lose from Facebook. He owns over 400 million shares, or 14% of the company, and holds 78.9% of the voting power (source). Zuckerberg has the largest incentive of all to keep Facebook in tip-top shape. He also has the power to do whatever is necessary to right the ship.

In his Q2 earnings call, Zuckerberg said:

Looking ahead, we will continue to invest heavily in security and privacy because we have a responsibility to keep people safe. But as I've said on past calls, we're investing so much in security that it will significantly impact our profitability. We're starting to see that this quarter. But in addition to this we also have a responsibility to keep building services that bring people closer together in new ways as well. In light of increased investment in security, we could choose to decrease our investment in new product areas, but we're not going to -- because that wouldn't be the right way to serve our community and because we run this company for the long term, not for the next quarter.

The market didn't like this (the stock fell 19% that day), but that's due to short-term thinking. Facebook expects its operating margin will decline to 35% in 2019 because its spending will increase faster than its revenues.

Facebook is spending on AI that will help to combat fake news and bad actors. It's also investing in better security and privacy systems. And it continues to build out data center capacity to stay ahead of demand.

This spending hurts in the short term but strengthens Facebook for the long term. Not only does it build a more trustworthy network, but it also creates a barrier to entry.

Facebook spent $6.7 billion in capital investments in 2017, and will spend even more in 2018 and 2019. Users and regulators now demand these up-front investments in security, and Facebook is lucky that it is in a position to make them. Competitors and upstarts will not be so lucky. How could a start-up, with a smaller revenue base, afford to sink billions into security systems on day one?

GDPR is likely to be the beginning of data regulations, not the end. Regulations are likely to entrench Facebook and Google in a duopoly since no one else will have the resources to comply with the regulations.

Facebook is also taking action to ensure social media has a positive effect on users' mood and self-esteem. In Q2 Zuckerberg said:

And the research there is very clear, that when people are using the Internet and -- including our services -- to interact with other people, that's associated with all the positive elements of well-being that you'd expect -- feeling more connected, feeling less lonely, feeling happier, and long-term measures of health. But when you're simply using the Internet to passively consume content, that isn't necessarily associated with positive improvements to well-being. Both because of the feedback that we were getting and the research, we felt like this was really the right direction to go in.

Facebook is re-prioritizing interaction with friends, family, and groups, at the expense of video and other forms of passive content. This may hurt revenues in the short term, but is likely to make the Facebook community closer, stickier, and more interactive over the long run.

Facebook isn't abandoning video altogether either. It's moving it to new places on the platform where it does not compete directly with interactions. Facebook launched Stories on Instagram, Facebook, and WhatsApp with great success.

Untapped Pricing Power

One of the most valuable qualities a business can possess is untapped pricing power. That is, the ability to raise prices faster than costs without sacrificing volume.

Facebook's ad prices are set by an auction process. In The Psychology of Human Misjudgement, Charlie Munger writes:

Well the open-outcry auction is just made to turn the brain into mush: you've got social proof, the other guy is bidding, you get reciprocation tendency, you get deprival super-reaction syndrome, the thing is going away... I mean it just absolutely is designed to manipulate people into idiotic behavior.

Then there is the Warren Buffett rule for open-outcry auctions: don't go.

The outcome is a lollapalooza effect that results in what's known as the winner's curse. According to Wikipedia:

The winner's curse is a phenomenon that may occur in common value auctions, wherein the winner will tend to overpay due to emotional reasons or incomplete information.

The system is designed to get the top price, and prices have been going up. Advertisers are driven by ROI - the more they make from an ad, the more they will spend. Facebook's unique ability to serve well-targeted ads makes its ads valuable to advertisers.

Source: Facebook's 2018-Q3 Earnings Slides

Other than the seasonally strong fourth quarter, Facebook's ARPU shows steady growth over the last year.

The ARPU data above shows a large difference between the value of a user in the US and Canada and the rest of the world. The US and Canada are mature markets for Facebook: penetration, as a percent of the population, is steady at 65%. But ARPU has continued to increase.

I expect ARPU to continue to climb because Facebook continues to benefit from multiple tailwinds.

At the most basic level, the world's population is increasing. Meanwhile, an increasing percent of the world's population is connected to the internet. Today, only 55% of the world's population is on the internet (source).

User penetration (as a percent of the total population) has plateaued in the US and Canada at 65%. The world's population today is 7.7 billion, and it's growing at 1.1% annually (source).

If the rest of the world reached the same 65% penetration rate as the US and Canada, Facebook would add 2.734 billion users. Facebook's ARPU for users outside of the US and Canada is $14.18, meaning these users are worth $38.8 billion annually. Facebook's marginal cost of production is near zero, so this would be mostly profit.

In addition to internet penetration and population growth, FB benefits from an increasing ad market. Ad dollars tend to grow in tandem with GDP, and could conceivably rise slightly faster as small businesses gain access they previously didn't have (source).

As Facebook gains newly connected internet users in emerging markets, it will also gain advertisers in those markets. That is, Facebook is likely to gain market share of the advertising market in emerging markets. This will drive ARPU higher while MAUs also grow.

Together, these forces mean Facebook has many years of above-GDP growth left in it.

The final factor to discuss is Facebook's ad load. I don't expect Facebook to materially alter its ad load on its flagship properties - Facebook Feed, and Instagram. But Facebook has room to monetize Stories (Facebook, Instagram, WhatsApp), as well as WhatsApp and Messenger.

Stories may end up cannibalizing some of the ads previously destined for Feed, but all in all Facebook should be able to increase its number of ads served by monetizing its other properties.

High Return On Incremental Invested Capital

Facebook is not a capital intensive business. The company's major costs are engineers and data centers. Its cost of maintaining these is minimal.

Facebook does spend a lot on growth initiatives. These have proven to be lucrative, and show no sign of exhaustion.

Between 2010 and 2017, FB's total capital invested grew from $2,433 million to $54,242, a change of $51,809. I define total capital invested as shareholders' equity plus debt and capitalized leases minus goodwill and intangible assets.

Over the same period, the company produced cumulative operating cash flows of $62,461 and retained almost all of it.

What was the result of this reinvestment? Facebook's operating cash flow grew $23,518: from $698 million in 2010 to $24,216 in 2017. This means return on investment was 45% (23,518 / 51,809).

Buybacks & Capital Allocation

Facebook is drowning in cash and needs a way to spend it. Historically, the company has invested in itself and made acquisitions (notably Instagram, WhatsApp, and Oculus).

Today Facebook's TTM operating cash flow stands at $28 billion. There's a limit to how many data centers and engineers Facebook needs. It's unlikely to be able to reinvest in itself at the same rate as it has historically.

The company is also unlikely to make another major acquisition because of antitrust concerns.

That leaves returning the capital to shareholders by dividends or share repurchases. So far, Facebook actions indicate that it prefers repurchases.

FB has currently authorized $15 billion of repurchases, some of which has already been spent. Given its large net cash and securities position ($41 billion) and its strong free cash flow ($16 billion over the past 12 months), I wouldn't be surprised to see even more repurchases in the future.

Valuation

When I invest, I follow a simple checklist:

1. Untapped pricing power

2. Anti-fragile capital structure

3. Management with skin in the game

4. A price which affords a margin of safety.

So far, I've addressed the first three points. Now, I will address the fourth.

Facebook's trailing 12-month EPS is $6.76, and the stock currently trades at $136 per share. It has about $14 of excess cash and securities that aren't used for operations, which means the business (excluding cash and securities) trades for $122 per share for a P/E ratio of 18.

The S&P 500 currently sports a 20x P/E ratio (source). Even if you believe that Facebook is just an average company, then it looks to be slightly undervalued today.

But FB isn't just an average business, it's a phenomenal business. It has a strong balance sheet, pricing power, ample growth prospects, and the ability to reinvest at high rates of return.

Compared to the S&P 500, Facebook looks cheap: it's an above-average business selling for a below-average price.

Facebook also compares well against its primary competitor, Google. Net of cash, Google's shares trade for 33x earnings. If Facebook were to trade here, it'd be worth $237 per share or 74% more.

There's no telling if Google is priced correctly, however. Maybe Google should be trading for Facebook's multiple and is overvalued currently.

After all, Facebook did guide for its operating margin to contract to about 35%. Facebook's TTM operating margin was 47%. If we assume that Facebook's operating and net margins contract 12 points each, then Facebook would have a 25% net margin.

At a 25% net margin, FB would earn about $4.50 per basic share and have a 27x P/E (excluding cash and securities). This is still cheaper than Google, though a significant premium to the S&P 500.

These valuations are simplistic and look at Facebook as a picture, frozen in the present. But what about the company's future?

Facebook has a lot of levers to pull for growth:

Increasing ARPU, due to increased ad spending (which is due to an increasing market share of all ad dollars, plus an ad market that grows at a GDP-like rate).

Increasing users, primarily from emerging markets.

Monetizing new and existing properties (such as produced by multi-tenanting).

Facebook's growth is extremely valuable because it does not come with commensurate costs. In 2010, its operating margin was 34% on $777 million revenue. In 2017, it was 50% on $40,653 million revenue.

If Facebook continues to grow, it is likely to continue to experience operating leverage. The next few years may buck this trend as Facebook makes "catch-up" investments in privacy and security.

Even if a 35% operating margin (and 25% net margin) was the new normal going forward, FB would "only" need to grow revenues 43% in order to maintain its current EPS. I say "only 43%" only because Facebook has grown revenues at a 75% CAGR since 2010. And it grew revenues 47% from 2016 to 2017. When analysts fret about slowing growth, they are talking about decelerating growth - the second derivative.

Facebook is quite likely to continue growing and at a fast clip by most standards.

The Bottom Line

When Buffett bought American Express, he looked past the news and focused on what mattered most: were people still using their charge cards? If the network remained intact, the company would eventually right itself.

Facebook is in the same situation today. So far, there is no evidence that Facebook is having trouble maintaining or attracting users, and this is what matters most over the long run.

Facebook is a wonderful business, and so long as its network remains strong, it will continue to compound for many years. FB stands to benefit from user growth, market share growth, pricing growth, and operating leverage.

The market isn't pricing Facebook like this is the case though. FB's P/E multiple is 10%, lower than the S&P 500's, which means the market expects Facebook to grow slower than average.

Facebook is laying the foundation for its future by investing increasing amounts today, at the expense of tomorrow's earnings. It is taking initiatives to make its platform safer, more secure, and more interactive.

Sometimes things get worse before they get better. There's never just one cockroach in the kitchen, and Facebook is not out of the woods yet. For investors who can afford to take a long-term view, however, this is precisely the kind of pessimism you want to buy into.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.