Eurofins Scientific: Resilient Compounder

October 2022 marked 25 years since the IPO of Eurofins Scientific, a global leader in laboratory testing. During those 25 years only three companies across the globe have generated higher returns for shareholders; Apple, Amazon, and Monster Beverage.

Since going public Eurofins has compounded shareholder capital at 26% annually, or over 33,000% in total, resulting in a more than a 400-bagger. These returns are after a roughly 50% decline in Eurofins stock from its recent all-time high in late 2021.

Of the companies listed above, all global leaders in shareholder returns, most are well known; except Eurofins. It’s probably time more investors become familiar with the business.

Overview

Eurofins is headquartered in Luxemburg, listed in Europe, and run by founder Gilles Martin, who owns over 30% of the business. Martin started the company with one lab and four employees in 1987. Today Eurofins employs over 60,000 people, operates over 900 laboratories around the world and performs more than 450 million analytical tests per year.

Eurofins provides testing services for four main areas: Food, Clinical, Environmental and Consumer Products, and Pharmaceuticals. All of Eurofins main testing areas are enjoying secular growth and have limited exposure to the broad business cycle. Broadly speaking, society is increasingly interested in testing our food, products, and environment, and Eurofins will be there to perform the tests.

Pharmaceuticals

Eurofins supports testing throughout the life cycle of drug development. They perform things like modeling and screening, potency, and assay tests during the discovery phase; toxicology and stability testing during the preclinical phase; and API and microbiological testing during the approval and commercial phase. They work with virtually all of the global leaders in pharmaceutical development across a myriad of different types of drugs at varying stages of development. You can think of this segment as a beneficiary of the incredible levels of investment across the pharma industry.

Food

Eurofins offers the world’s broadest array of food testing capabilities. Examples include testing for purity, composition, pesticides, allergens, GMOs, and pathogens; among hundreds of others food characteristics.

They work with all constituents in the food supply chain who need testing from farm to fork. In addition to testing, Eurofins helps manufacturers and processors implement high quality food safety measures in their facilities.

Environmental

Ensuring clean and safe environmental standards is a growing concern for countries around the world, and Eurofins is there to provide those tests. Typical environmental tests include testing water for contaminants (surface, waste, groundwater, drinking water, etc.), testing the air for pollutants (emissions, indoor air quality, soil gas testing), testing for waste and contaminants in a range of products (consumer products, soil) and pandemic and epidemiology testing (such as predicting the spread of COVID via waste water sampling).

Clinical Diagnostics

The main areas in this bucket are tests for women’s health before, during and after pregnancy; transplantation and donor screening; oncology diagnostics and treatment; and infectious disease real-time testing (such COVID or flu PCR tests).

Industry Characteristics

Analytical testing is a great business in general, and Eurofins in particular is the best of the bunch.

High Customer Switching Costs

Analytical testing is a very sticky business. Across all segments, the cost of failure (an incorrect test result) is high, and therefore trust in a testing provider is paramount. As the #1 or #2 provider in each major testing category, Eurofins has earned a reputation as a trusted and go-to testing partner, and customers have little reason to look for an alternative.

The cost of a test is very low in relation to the end product’s value, especially when it comes to high-value pharmaceuticals. Customers have no reason to shop a testing provider to save a few pennies; it’s not going to move the needle for them and it will introduce unwanted risk into their process. So, they stick with what’s working.

Perhaps most importantly, Eurofins has integrated its bespoke Laboratory Information Management Systems (LIMS) into its customer’s IT systems, further embedding their customer relationships. Eurofins’ LIMS system will automatically push test results and other data directly to their customer’s ERP system which creates an entrenched position within the supply chain. Connecting their LIMS system to the customers’ IT systems allows for optimized test ordering, data sharing, and product releases across its customer base. It also makes it a huge pain in the ass to switch testing providers.

Thanks to the high cost of failure, price-to-value nature of analytical testing, and integrated IT systems, Eurofins enjoys sticky and high retention customer relationships.

Recurring and Recession Resistant Demand

The life sciences-related testing market generally enjoys growing, resilient, recurring, and non-cyclical demand. As Eurofins explains in its 2022 Annual report:

“Even in times of crises or recessions, testing services typically remain in demand as the need to ensure that food and water is safe, pharmaceutical products are effective, and the environment is protected remains resolute. This is evidenced by our track record of positive organic growth even through the financial crisis of 2007-2009 and during the COVID-19 pandemic.”

There is also an ongoing trend of outsourcing testing to 3rd party laboratories like Eurofins so companies can better focus on their core competencies and reduce operating costs.

Through thick and thin the business has grown at above-GDP rates organically, a trend that shows no signs of slowing.

Eurofins Competitive Position

Eurofins not only enjoys the benefits from a favorable industry, but has proven itself to be the best within the industry for a number of reasons, most of them relating to scale advantages.

Management emphasizes Eurofins focus on its “hub and spoke” strategy, which constitutes a major competitive advantage over smaller peers. The company has invested heavily over the past 10 years in building and acquiring laboratories all over the world to feed its hub and spoke model. The “hubs” serve as high throughput centers of excellence that specialize in high volume tests. Eurofins often acquires standalone or smaller lab networks in targeted geographies, closes them down and consolidates their testing in a hub to generate scale efficiencies. The customers benefit via faster testing turnaround times thanks to the specialization of the hubs and Eurofins benefits from economies of scale. The spokes perform the lower volume tests customized for companies in that area, again serving the customers for their specific needs.

Here is an example of a case study of how Eurofins hub and spoke model generates benefits.

In this example Eurofins consolidated 7 smaller sites into one large testing center and improved sales per square meter by 100% and sales per person by 26%. Replicated countless times around the world, the benefits add up.

Eurofins scale also allows it serve as a one-stop-shop for many of its large customers who, like Eurofins, have locations all over the world. Rather than dealing with a bunch of small local testing outfits, large multinational companies can utilize Eurofins as its testing partner for all of its sites.

Finally, the cost of developing sophisticated tests and building massive laboratories with expensive equipment is far from trivial, and Eurofins has a massive head start. While the industry is still fragmented, Eurofins has built a formidable testing empire with hard to replicate assets, a combination that’s likely to leave competitors increasingly in the dust.

In addition to its scale benefits Eurofins has a unique culture that is similar to many of the great companies we follow. Specifically, founder Gilles Martin has instilled a highly entrepreneurial and decentralized culture that permeates all levels of the organization. I can’t summarize it much better than the company’s annual report, which explains:

“Eurofins’ decentralised structure of entrepreneur-led companies promotes closer relationships with, and more individualised services for, clients, while fostering business agility and scientific innovation. Instead of a centralised laboratory group, we are, by design, a network of empowered entrepreneurs each leading their company with a large degree of autonomy.”

Much like Berkshire, Heico, Alimentation Couch-Tard, Constellation Software, and so many other great businesses, Eurofins emphasizes the importance of making decisions at the lowest possible level. It’s this entrepreneurial spirit that fosters innovation and rapid test development in response to localized needs. Never was this more important than during the constantly evolving pandemic, and Eurofins continuously responded by bringing new and improved COVID tests to market.

In addition to the decentralized nature of the company, Gilles runs the business with a conservative balance sheet (just 1.6x leverage ratio) and maintains significant skin in the game via a 30%+ ownership position.

Fundamentals

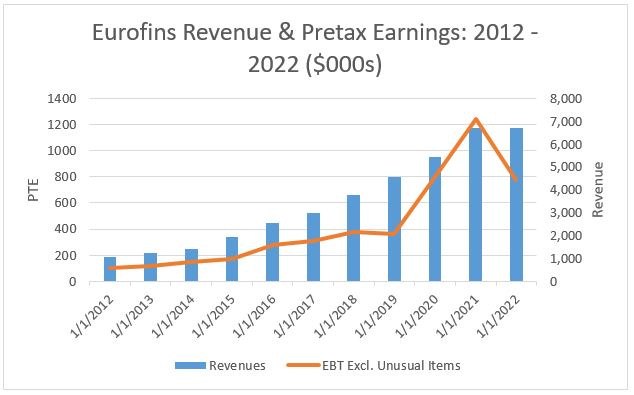

Eurofins has grown a tremendous amount over the years. The company has doubled sales on average every five years since 2005 and earnings per share have grown 42-fold between 2005 and 2021. Over the past ten years operating cash flow and free cash flow have compounded at more than 20% per year.

Eurofins is not a capital-light compounder and has not benefited from outsized industry growth. Rather, their growth is the result of a tremendous level of reinvestment into the business and attractive incremental returns on that investment.

Over the past decade Eurofins has reinvested roughly 140% of its operating cash flow, or $9B, into organic and inorganic growth initiatives. Of the $9B of retained capital, about $4.5B has been in the form of equity (via retained earnings) while the balance has come from debt issuance. This $4.5B of incremental equity has resulted in $1B of growth in operating cash flows for a 20%+ return on equity retained.

When Eurofins builds a new lab it typically takes 2-4 years for the site to mature, at which point it delivers high returns on capital. The company targets 16% pre-tax returns on capital when evaluating any growth opportunity.

My guess is that if and when Eurofins slows the pace of reinvestment, returns on capital will continue to rise as they harvest the seeds they’ve planted over the years and the sites mature without commensurate investments in new locations.

Reinvesting more than 100% of earnings at even low double-digit returns on capital (debt & equity) and north of 20% on equity results in extremely high value creation for equity holders, and it appears the company has plenty of room to continue replicating this process.

Forward Returns and Valuation

As with many businesses that were impacted positively or negatively by COVID, Eurofins is experiencing noise in its results. After having grown in a near straight line for decades, Eurofins profits declined in 2022 compared to 2021. This was not due to deterioration in its core business but rather from highly inflated levels of profitability due to high margin and high volume COVID testing in 2020 and 2021. Last year Eurofins replaced all of the revenue it lost from decreased COVID testing but it earned less money thanks to continued heavy investments in growing its network as well as normalized margins thanks to lower COVID testing and operating cost inflation.

With COVID in the rear view mirror, Eurofins appears poised to resume its historical growth algorithm.

Organic growth should average 5-6% per year (they do a great job breaking out organic/core business growth for investors) and with how fragmented the testing industry remains I think high levels of M&A remain likely. The company acquired 59 businesses (small labs or lab networks) just last year. All of the company’s major segments are experiencing secular growth as demand for testing increases with increased levels of regulation, wealth, and innovation around the world.

If Eurofins continues to soak up 100%+ of its earnings (less than the 140% of the last 10 years) between organic and inorganic growth initiatives intrinsic value should continue to compound at a mid-to-high teens rate for the foreseeable future and produce enviable returns for shareholders – as long as the price paid for the stock is reasonable.

Speaking of price, the stock appears a lot more reasonable now than it has at any point in the recent past. While not bargain-cheap, at 19x trailing earnings the stock is no longer priced for perfection. In fact, the company only trades at a slight premium to the S&P 500. In the years leading up to COVID, the stock consistently traded at 2-3x the current valuation given the growth the company consistently delivered.

I won’t ruin all the fun and you can pick your own fair multiple for the business. I will say, even ignoring M&A, the 5-6% core growth, if it can be sustained, is worth 21-26x using a 10% discount rate.

Investors appear perturbed that a) the COVID boom is over (which we knew would happen) and b) that earnings will revert back to pre-COVID levels, and the current stock price will prove expensive. That ignores the underlying growth in the core business over the same time period. With the COVID boom rolling off of the recent financials, I don’t think reported earnings would be much different than where they are today if COVID had never happened.

Management recently rolled out longer range financial targets, and the goals look well within reach.

While Current prices dictate that investors do need some growth to materialize to earn attractive returns, and I’d prefer a little more pessimism to be baked into the price, the company is targeting ~20% growth in free cash flow through 2027 and has a history of delivering. If they can even come close to hitting these targets (as they have in the past) today’s prices may look like a bargain.

Given the company’s predictable, recurring, and non-cyclical end market demand, enviable industry and competitive position, and high-performance culture, Eurofins appears to represent a far above average business at a fair price.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. You can also find more information on our website. We recommend starting with our Fundamentals. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

The amount of goodwill on the balance sheet is what threw me off.

Do they plan on reducing the share of goodwill over time?

Have you guys looked at the short case on that one?

https://www.shadowfall.com/wp-content/uploads/2019/01/Eurofins_ShadowFall_Research_Report_FINAL_16_Oct_2011.pdf