Domino's Pizza Group: Asset-Light Royalty Business for 10x Earnings

Most people that follow the stock market know that Domino’s is an excellent business. I wrote about Domino’s last year so I won’t rehash the entire story, but the highlights include:

Domino’s enjoys major scale and relative market share advantages in its markets;

The business is recession-resistant with a long growth runway;

The company has a vertically integrated supply chain segment that provides cost and delivery advantages to a captive and growing franchisee base;

Franchisors are asset-light royalty businesses where nearly 100% of free cash flow can be returned to shareholders via dividends and share repurchases;

Management has been exceptional employing a clustering strategy and maintaining a rigorous focus on a simple menu and an emphasis on small stores that provide delivery and carry-out only;

Capital allocation has created tremendous value as the stability of the business model has allowed management to employ a levered buyback approach.

Domino’s is one of only a few successful global pizza chains, and Domino’s Pizza Group (DPG) is the master franchise for Domino’s UK-based franchisees.

Domino’s is a business we’ve long admired and wanted to own, but we have never been presented with a price that afforded us with enough of a margin of safety.

Domino’s Pizza Group is a high quality and simple business that enjoys many of the same benefits as Domino’s. The company is a dominant, growing, asset-light royalty business in a recession-proof industry with newly implement value-creating capital allocation framework. For a variety of reasons which I’ll go into, DPG can now be purchased for a much more attractive price than the U.S. parent company.

Business Model and Relationship to Domino’s

It’s very common for franchisors to pursue a master franchise arrangement for international growth initiatives. A master franchise grants exclusive rights to recruit other franchisees for a certain geography. Starting in the early 1990s Domino’s (the franchisor) gave Domino’s Pizza Group the right to recruit and manage the franchisee base in certain European markets.

The relationship between the constituents is, roughly:

Domino’s grants the rights for DPG to open franchisee locations in the UK and Ireland;

DPG recruits franchisees to open locations all over the country and markets the Domino’s brand, invests in digital capabilities and sources ingredients for franchisees;

Franchisees sell a lot of pizza;

DPG gets a royalty on the pizza sales;

DPG sends Domino’s a small royalty on pizza sales in their territory and keeps the rest of the royalties for itself;

DPG returns loads of cash to shareholders;

Go back to step 2.

There’s a lot to like about this model.

Value Drivers and Competitive Position

This is not a complex business. There are only a few key drivers for owners to keep an eye on. The prosperity of a franchisor is a direct function of the health of its franchisees. If the economics don’t work for the franchisees there is no hope of success for the franchisor. Fortunately for DPG, the average franchisee earns $245K in EBITDA and 20%+ margins from each location. Domino’s is known for attractive economics and the UK market is surprisingly even more profitable than U.S. franchise locations, which themselves generate excellent returns.

Offering attractive returns to franchisees makes recruiting and maintaining locations easy and drives the returns for the master franchise. DPG’s business is a function of system wide sales, or the total revenue of all franchisee locations. System wide sales is a function of same-store sales growth (SSSG) and growth in new locations.

Over the past five years DPG’s core UK market has averaged same-store sales growth of 7%, but that includes two years of lock-down fueled demand. Pre-pandemic, the UK locations were growing closer to 4.5%, which is a more normalized and still very healthy growth rate.

DPG currently has about 1,230 locations and is opening 45+ locations annually. Accordingly, unit growth should average 3-4% per year for the next several years.

Because DPG’s business is asset-light the business earns great returns on capital (roughly 100% on tangible capital) and should enjoy expanding margins. There just aren’t a lot of variable costs for a franchisor; franchisees contribute to an advertising fund, put up the capital for their restaurants, and pay all operating expenses. Accordingly, franchisors often enjoy significant operating leverage over time and gush free cash flow.

In addition to an attractive underlying business model, DPG is dominant in the UK market. Incredibly, DPG franchises enjoy a 48% market share in the pizza market, up from 42% a year ago. The business has a 6.6% overall share of the delivery (or “takeaway”) market.

Source: H1 2022 Investor Update

Additionally, the company is very digital with 90% of sales generated through digital channels and has a massive advantage in app users compared to competitors.

Finally, the pizza business is very resilient and not reliant on making any correct macroeconomic predictions. People eat pizza during good times and bad, and owners of DPG do not need to bother themselves keeping up with the latest CPI print, the price of oil, monthly jobs reports, or any other nonsense that drives short term stock price fluctuations.

Business Transformation

DPG has been going through a period of transition for the past few years which is now largely complete. While the core UK and Ireland business has been strong, DPG historically managed some franchisees in Iceland, Switzerland, and Germany. The non-UK locations were not managed as effectively by legacy management and created a drag on profits and growth. These markets masked the strength and quality of the UK market and proved to be unprofitable distractions.

Over the last few years the company has sold off nearly all of its international businesses except for Germany and is laser-focused on its core market. DPG has a “put option” to sell the Germany operation to an Australia-based master franchise and it is likely to exercise that option in the next year or two.

The board of directors has completely turned over since 2019 and is now comprised of a number of industry veterans with skin in the game. Many of the directors have purchased considerable ownership stakes in the business: Usman Nabi of Browning West owns $100M, or 10% of the company, Colin Halpern owns $3.5M and interim-CEO Elias Diaz Sese owns more than $1.5M.

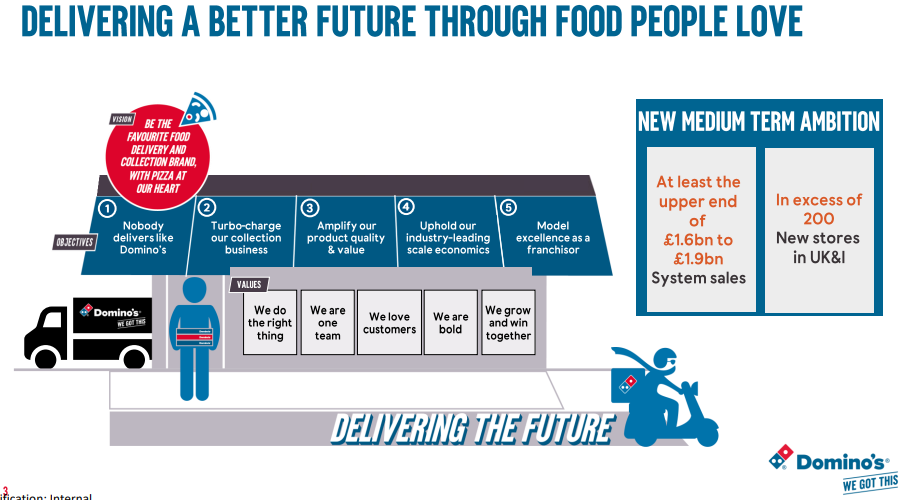

Last year DPG released a “resolution with franchisees” that marks a new era of collaboration and growth in its core market. With 99% approval from franchisees, DPG will make a $20M investment in digitalization and app improvements, implement a refreshed store incentive system, and lead increased marketing initiatives and promotional campaigns, among other things. In turn, franchisees have committed to a number of initiatives to drive system-wide sales growth including an enhanced schedule of store openings, participation in national promotions focused on both delivery and take-out, and an agreement to prioritize and test various technology upgrades such as GPS tracking and new store formats.

Source: December 2021 Investor Presentation

In conjunction with the refreshed franchisee strategy the new board implemented a much more rigorous focus on capital allocation. This is a major shift for the business and should drive excellent returns for shareholders. More on this below.

It’s hard to call the repositioning of the business a “turnaround” considering the company was delivering very healthy results even prior to the last few years. However, disposing of underperforming markets and refocusing on franchisee partnerships in the UK amidst a refreshed leadership team is a significant positive. If this is a turnaround then it’s my kind of turnaround.

In addition to these refocusing efforts, there has been considerable noise over the last few quarters making year-to-year comparisons temporarily hard to interpret.

Recent Events

Recently reported results do not accurately reflect the underlying reality of Domino’s Pizza Group’s business for a few reasons.

During the first half of the year DPG reported a system wide sales decline of around 5%, which would be rare for the business. Digging deeper reveals that the decline in revenue is due to the reintroduction of the value-added tax (VAT) for restaurants in the UK. During COVID the UK government largely eliminated the VAT for restaurants (decreased the VAT from 20% to 5%) in order to provide financial relief to an industry decimated by COVID. The extra revenue that franchisees realized due to not paying the VAT ultimately partially flowed through to DPG in the form of abnormally high royalties. With COVID waning the UK gradually phased the VAT back in causing a one-time decline in reported revenue. If not for the impact of the VAT issue system-wide sales would have grown 3.4%.

This growth is particularly impressive given 2021 was filled with periodic lockdowns in the UK which resulted in super-charged sales for the pizza industry. UK same-store sales growth was an outstanding 11% in 2020 and 2021 thanks to COVID, and growing at all on the back of those results is impressive.

The business also passes through ingredient cost increases every six months and the recent price increases have yet to flow through reported results, temporarily depressing margins for the supply chain segment.

All of the short term noise aside, investors should keep their eyes on what matters: franchisee health, underlying and long-term system wide sales trends, and capital allocation.

Forward Returns and Valuation

Historically core markets have grown same-store sales 3-4% annually and the business is committing to 45+ new stores per year which should add another 3-4% to annual growth. Accordingly, I’d expect system wide sales to increase at a high single digit rate on average over the next 5+ years. With the less profitable international segments now largely disposed of, I expect margins to march higher as well. As a preview of what could be possible, Domino’s (U.S.) has driven operating margins from 18% to 30% over the past ten years thanks to the operating leverage of its royalty business.

In 2021 the board outlined a renewed focus on capital allocation where virtually 100% of free cash flow should come back to shareholders each year. I estimate DPG’s normalized earnings power of around $100M (all my numbers are in GBP) and DPG’s market cap is currently roughly $960M, meaning the stock is currently priced at a 10%+ earnings yield.

DPG pays a 4.4% dividend yield and shareholders are likely to receive the rest of free cash flow through buybacks for another 4-6% annually. The business is conservatively capitalized with less than 2x leverage so it wouldn’t surprise me to see >100% of free cash flow returned to shareholders annually for a while.

Source: H1 Investor Update

It takes no heroic assumptions to pencil in mid-teens per share compounding by way of 6-8% sales growth + 4.4% dividend + 4-6% buyback yield for the foreseeable future. Even if growth plans faceplant it’s hard to see this being a disaster from present prices given the 10% free cash flow yield.

It’s not common for a business of this quality to sell for around 10x normalized earnings. Thanks to the recent business transformation, noisy current period financials, and a small, under-followed foreign stock, DPG is currently priced well below our assessment of intrinsic value. Also, the stock is traded on the London Stock Exchange and the recent chaos in the UK financial markets hasn’t done stocks listed in London any favors. Fortunately, UK pension funds falling into a liquidation spiral from dislocations in the Gilt market has no bearing on how much pizza people consume.

We’ve been following the business for awhile and it has historically been priced more appropriately (mid/high teens earnings multiple), consistent with other high quality franchisors. If the stock re-rates to a fair valuation it could add another 10% to the already attractive annual returns outlined above (though the buyback yield would compress somewhat given the valuation would be expanding).

On top of all of that, if DPG exercises its put option on the Germany business it would likely receive another $70-$100M, or close to a full years’ worth of earnings. Management has indicated these proceeds will be returned to shareholders as well, effectively further lowering the price investors pay today for the core business.

Risks/Uncertainties

It strikes me as highly unlikely this business implodes any time soon. The pizza business is not subject to technological disruption, DPG has dominant market share in the UK, and has executed well in recent years. The real risk is that the company majorly screws up the brand (somehow) and sees same-store sales deteriorate for prolonged periods of time. This scenario is not supported by any evidence.

The CEO who led the business through COVID the past two years has taken a job at a larger business in Europe, so there is some uncertainty at the top. However, the business is being led by rock star interim CEO and board member Elias Diaz Sese. Elias is a 3G capital and Restaurant Brand International veteran who most recently led the turnaround of Kraft Heinz UK and before that held a number of leadership roles through QSR’s empire. It does not seem likely the board will botch the CEO hire. Clearly this is a business that can, and has, withstood a little mismanagement.

Summary

Domino’s Pizza Group is a business of which I’d be happy to own 100%. It’s an asset-light, growing royalty business with excellent capital allocation policies. Further, it is a simple, predictable, profitable company with dominant local market share in an industry not subject to disruption or the vagaries of the economy, and is currently selling at a material discount to intrinsic value.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. You can also find more information on our website. We recommend starting with Fundamentals. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

I thought today's market move post 4Q22 earning was a little harsh on the stock

Hi Eagle,

Thank you for the idea, great post. Just a quick question (I am not very familiar with the company), how is the relationship between the UK company and the holding? How easy is to change the terms of the agreement? How often has it happened in the past?

Thanks!