Constellation Software: AI's Threats and Opportunities

In 2018 Robert Smith, CEO and founder of Vista Equity Partners, told Forbes:

“Software contracts are better than first-lien debt. You realize a company will not pay the interest payment on their first lien until after they pay their software maintenance or subscription fee. We get paid our money first. Who has the better credit? He can’t run his business without our software.”

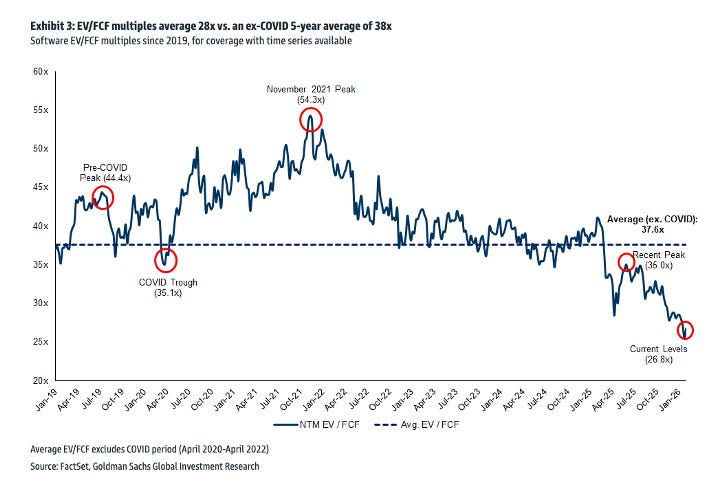

That insight made Smith a deca-billionaire. It also became gospel among investors, propelling software multiples to significant premiums over the broad market. According to Goldman Sachs, software stocks have traded at an average of 37.5x EV/FCF since 2018, largely because of their perception as “better than first-lien debt.”

But as the chart shows, that perception began to crack last summer. Most software stocks are down 50%+, following the classic “hopeless to flawless” swing Howard Marks talks about.

“Most of the time, the market’s short-term behavior stems from irrational swings of investor perception “from hopeless to flawless,” rather than a dispassionate weighing of merit.”

Software’s outlook was never as rosy as a 37.5+ EV/FCF valuation implied. Nor is it likely as dire as current valuations suggest.

The bear thesis on software is that AI will reduce the cost, time, and skill required to make it. Lower barriers to entry and fewer production bottlenecks will cause supply to increase, flood the market, and push prices to zero.

This rhymes with what happened to the media industry. The internet reduced distribution costs to zero while social media and user-generated content pushed the production cost of media to zero. Many traditional media failed, though some, like the New York Times, transitioned. Those that survived don’t have as wide a moats as they once did.

The ease of producing software could change the buy versus build calculus. Previously, only the largest companies could build custom software in-house. The rest bought off the shelf software that bundled features they needed with many they didn’t. AI may lower the cost enough to allow more companies to build custom software and try to extract a competitive advantage from it.

The flip side is that software companies will be able improve their software faster and add custom features for clients at a lower cost. Software companies are in a better position to integrate AI than a company with no special skills in software development building it.

Another risk is that AI agents could automate low level tasks, rendering the software that aided that work obsolete. For example, an AI agent may replace an entry level paralegal, rendering software for paralegals obsolete. Entry-level jobs that enter or manipulate data are the most at risk.

Companies that spend a large percent of sales on low-level knowledge work (basic data entry and manipulation) may have the most to gain from AI agents. Companies like ADP, Paychex, Equifax, Transunion, and Arthur J. Gallagher might be a candidate. Each of these, and companies like them, have lots of people doing manual checks and verifications of claims, benefits, dispute resolution, etc.

Of course, once every company adopts AI agents, the playing field will be level again. Companies will compete on price, giving some of their newfound margin to customers. Eventually, in a competitive market, customers will end up with the bulk of the savings. AI, like software, will be deflationary. Businesses will have had to invest in AI/software merely to remain competitive. In that sense investment in AI/software may be mandatory maintenance capex.

It’s also worth noting that as software automates more jobs, software companies may be able to charge more. They’ll be targeting a company’s labor budget, not their IT budget. A shift towards outcome based pricing may be a painful transition, like the transition from traditional licenses to SaaS, but ultimately beneficial. “Take-rate” businesses, like Visa, are among my favorite because they capture inflationary pricing and increasing volume automatically.

Alex Niehenke, a partner at Scale Venture Partners, recently wrote:

“With AI, companies can automate tasks traditionally performed by human experts, capturing a greater share of their customers’ value chains.

For example, instead of merely offering software to manage claims, an insurance-focused platform could automate claim approvals or fraud detection.

This change in delivery of value allows the vertical software vendor to price based on value rather than relative to employee salary, and the net result is profound.

We have seen examples of where the vertical AI vendor is capturing 25% or 50% or more of an employee salary. This would suggest vertical markets will be five to ten times larger through the introduction of artificial intelligence.”

AI will allow more software to be written faster. Software will get better and do things it previously couldn’t. In 2011 Marc Andreessen said “software is eating the world.” AI will enable software to eat more of the world, not less. That’s good for software companies.

Another bear thesis is that as software incorporates more AI features, like LLMs, it will introduce a cost of goods sold (COGS) component that software never had to deal with. Software has high fixed upfront costs but little to no variable costs. This allows it to scale with significant operating leverage.

The fear of the variable cost of LLMs is misguided. Today LLMs cost $1-3 per million tokens. A light user might use 50,000 tokens per month. A heavy user might use one million. A software company integrating AI into its software can likely eat a $1 to 3 per user per month cost, or easily pass it on, with a mark-up, for the added features.

Jevons Paradox

It’s theorized that AI will make workers more productive, so companies won’t need as many seat licenses for the software they keep. This has always been the promise of technology, but it has never panned out.

In his 1930 essay “Economic Possibilities for our Grandchildren,” economist John Maynard Keynes predicted that new technologies would mean that his grandchildren’s generation (roughly 2030) would only work three hours per day (15 hours per week).

In the 1950s the introduction of dishwashers, washing machines, and vacuum cleaners in the 1950s was marketed as the “liberation of the housewife.” Ads promised that these machines would grant mothers hours of relaxation or “bridge club” time.

In 1956 Vice President Richard Nixon predicted a four-day workweek in the “not-too-distant future.” Bloomberg wrote:

In 1965, a U.S. Senate subcommittee predicted that as a result of increasing labor productivity from automation and “cybernation” -- in other words, the computer revolution -- Americans would be working only about 20 hours a week by the year 2000, while taking seven weeks or more of vacation a year.

Jevon’s Paradox explains why we’re not working less. Originally applied to coal, it says that as technology makes a resource more efficient to use, we don’t use less of it, we use more because the cost of using it has dropped.

In her book More Work for Mother sociologist Ruth Schwartz Cowan explains that appliances didn’t reduce the number of hours spent on housework. Appliances raised the standards for cleanliness. Before washing machines, people washed their shirts once a week and linens once a month. After washing machines, they washed their clothes after every wear. The machine was faster, but demand increased commensurately. As a result housewives in the 1950s and 60s spent roughly the same amount of time on domestic labor as their grandmothers did in the 1910s, they just produced cleaner homes.

If Jevon’s Paradox holds, which it tends to when demand is elastic (sensitive to price), then as the cost of software decreases, demand is likely to increase commensurately. Software will eat the world faster. It is not so simple to assume that better software will lead to fewer seat licenses. Software will be expected to do more, and more people will use it.

Predicting how AI will affect software is speculative and difficult precisely because the world is a complex adaptive system. If you change the price, speed, or efficiency of software, everything else changes in response to adjust to it. Some software businesses will certainly go the way of newspapers, and others, born in an AI-native world, will thrive.

Types Of Software Businesses

Software businesses are not a monolith. Each business will be affected differently. Some for the better, others for the worse. Here are a few ways of thinking about the different types of software businesses.