Buffett's Two Favorite Chapters

Buffett has consistently said that Chapters 8 and 20 in Ben Graham’s “The Intelligent Investor” have served as the foundation of his investment approach since the 1950s. In a 2013 interview with Forbes Buffett said:

“Chapters 8 and 20 have been the bedrock of my investing activities for more than 60 years. I suggest that all investors read those chapters and reread them every time the market has been especially strong or weak.”

Pretty strong endorsement. These chapters are probably worth reviewing at least once per year for any serious investor, and are especially helpful in times like the present when the market has been particularly strong and particularly volatile. It’s unlikely you’ll uncover anything revolutionary when rereading these chapters, but reinforcing the basics is as important (if not more so) than spinning up brilliant insights. I recently reread these chapters and below are some thoughts and applications to today.

Graham originally penned these chapters in 1949. The types of stocks he bought were far different than the stocks we buy, and far different from what types of investments are available or generally work well today. But the ideas in his book are still 100% applicable to a sound investment process 70 years after they were written. I suspect they’ll age just as well over the next 70 years.

Chapter 8: The Investor and Market Fluctuations

The two themes of chapter 8 are:

1) The market (or Mr. Market as Graham says) is often manic depressive and therefore daily price quotations frequently swing far more wildly than changes in intrinsic business value. And;

2) Mr. Market is there to serve you, not to instruct you. All investment decisions should be made on the basis of value, not price. Put more simply: think for yourself.

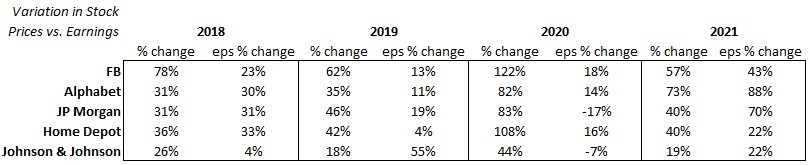

While it may be widely accepted that prices swing in excessive of intrinsic value, I always find it amazing the magnitude and consistency of these swings, even in the world’s largest companies. Below is a table of a handful of the largest companies by market cap in the S&P 500 (all are in the top 15). I’ve listed the annual variation in stock price compared to the change in reported earnings per share for that year. There is no selection bias here, I just picked some of the largest companies in the market with little relation between them aside from the obvious dependence on internet ads of Google and Facebook. The stocks here are far from the most volatile stocks in the market and are among the most widely covered and therefore presumably best understood.

Source: Author, ValueLine

Some of these swings are almost laughable. JP Morgan’s stock swung 83% in 2020 thanks to the pandemic while earnings dipped less than 20% (and are now at record highs!). Facebook’s stock is incredibly volatile year in and year out compared to earnings, with volatility usually centered around the negative news cycle directed at the company. Overall these stocks averaged a 54% share price variation compared to an average 25% change in earnings.

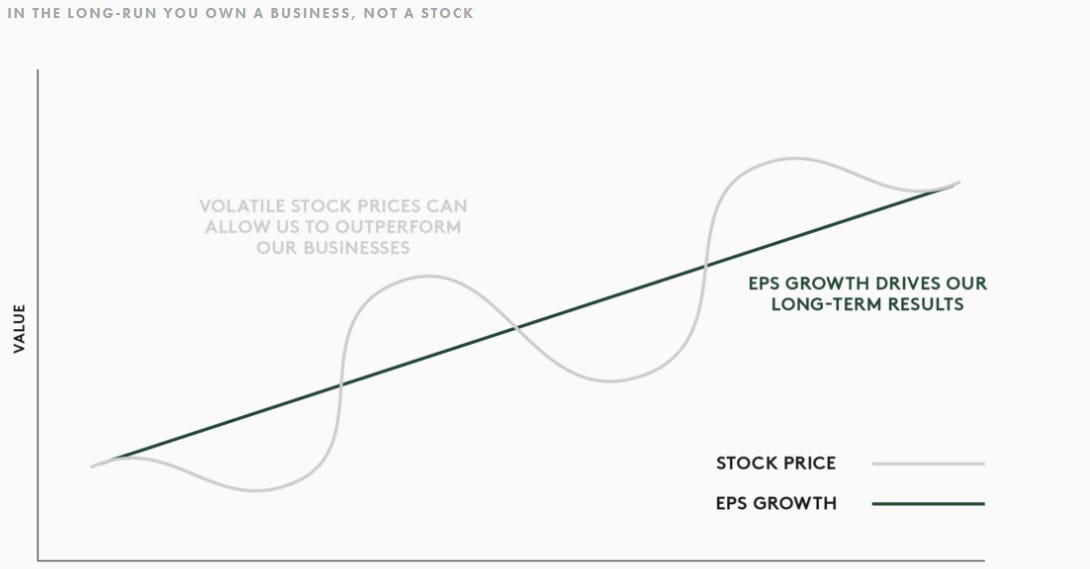

One of my favorite figures to keep in mind comes from Ruane Cunniff’s website. Over the long-run what matters is where business value is going, not where short term stock prices are going. Stock prices zig and zag around the overall trajectory of business value, often to extreme degrees.

Source: Ruane Cunniff

Graham reminds us to focus on the underlying business behind a stock, as its earning power is what counts over the long pull. He writes:

“As long as the earning power of his holdings remains satisfactory, he can give as little attention as he pleases to the vagaries of the stock market. More than that, at times he can use these vagaries to play the master game of buying low and selling high”

One of my favorite quotes from the entire book outlines an attitude far too few investors embody.

“The true investor scarcely ever is forced to sell his shares, and at all other times he is free to disregard the current price quotation…Thus the investor who permits himself to be stampeded or unduly worried by unjustified market declines in his holdings is perversely transforming his basic advantage into a basic disadvantage. That man would be better off if his stocks had no market quotation at all, for he would then be spared the mental anguish caused him by other persons’ mistakes of judgement.”

I try my best not to frequently check stock prices as it reinforces very unhealthy habits towards short-termism. I advise our investors to do the same.

Buffett frequently references Graham’s chapter 8. He described his attitude towards Mr. Market particularly well in his 1987 letter to Berkshire shareholders, writing:

“Mr. Market has another endearing characteristic: He doesn’t mind being ignored. If his quotation is uninteresting to you today, he will be back with a new one tomorrow. Transactions are strictly at your option. Under these conditions, the more manic-depressive his behavior, the better for you.

But, like Cinderella at the ball, you must heed one warning or everything will turn into pumpkins and mice: Mr. Market is there to serve you, not to guide you. It is his pocketbook, not his wisdom, that you will find useful. If he shows up some day in a particularly foolish mood, you are free to ignore him or to take advantage of him, but it will be disastrous if you fall under his influence. Indeed, if you aren’t certain that you understand and can value your business far better than Mr. Market, you don’t belong in the game. As they say in poker, “If you’ve been in the game 30 minutes and you don’t know who the patsy is, you’re the patsy.

… [A]n investor will succeed by coupling good business judgment with an ability to insulate his thoughts and behavior from the super-contagious emotions that swirl about the marketplace. In my own efforts to stay insulated, I have found it highly useful to keep Ben’s Mr. Market concept firmly in mind.”

The clear reinforcement from this chapter is if investors are even moderately patient they are likely to be consistently presented with opportunities to buy some of the best companies in the world for less than they’re worth. Not every day or every month, but at least occasionally.

A more subtle, and I think even more important, lesson from chapter 8 is that investors need not react to every price swing. Randomness prevails over the short term but earnings prevail over the long term. Most of the money in investing is in the holding, not the acting, and the daily quotations and fluctuations of public markets make holding inherently difficult. Investors that truly internalize chapter 8 are far less likely to over-optimize a portfolio but instead let compounding do its job by buying interests in above average and easily understandable businesses and holding through the volatility.

Chapter 20: “Margin of Safety” as the Central Concept of Investment

The title of this chapter pretty much says it all. The chapter is a mere 13 pages but distills the essence of investing versus speculating. The single best way to control downside risk is to invest with a margin of safety. What exactly does this mean?

Put simply, investing with a margin of safety means conservatively estimating the price at which prospective returns for a business are satisfactory and then paying a lot less than that figure. The less you pay in relation to what you think the business is worth, the higher the margin of safety. Investing with a margin of safety helps protect you from needing to predict an unknown future with pinpoint accuracy and still achieve satisfactory outcomes.

A misnomer about Graham is that he detested growth investing and that his approach only works for statistically cheap stocks. I disagree and so does Graham. The concept of margin of safety applies to virtually any investment or security. As Graham wrote regarding growth stocks:

“the growth-stock approach may supply as dependable a margin of safety as is found in the ordinary investment – provided the calculation of the future is conservatively made, and provided it shows a satisfactory margin in relation to the price paid…The danger in a growth-stock program lies precisely here. For such favored issues the market has a tendency to set prices that will not be adequately protected by a conservative projection of future earnings…The margin of safety is always dependent on the price paid. It will be large at one price, small at some higher price, nonexistent at some still higher price.”

Whether you invest in technology stocks, “old world” industrial stocks, real estate, or anything else, you can always incorporate this concept into your investment process. As long as you deeply understand the underlying business and use conservative estimates to arrive at a future earnings power of the asset, and pay a lot less than that figure, an adequate margin of safety can be found.

One aspect I would add to this chapter, and one which Buffett has spoken about and which we actively employ, is the idea of business quality as a margin of safety. Graham emphasizes price as the core tenant of investing with a margin of safety, and I no doubt agree. However, investing in high quality businesses can allow for an adequate margin of safety at somewhat higher valuations than lower quality businesses.

Graham actually alluded to this as well. On evaluating price and quality he says:

“the risk of paying too high a price for good-quality stocks – while a real one- is not the chief hazard confronting the average buyer of securities. Observation over many years has taught us that the chief losses to investors come from the purchase of low-quality securities at times of favorable business conditions”.

Graham is cautioning against extrapolating extraordinary short term results in perpetuity and tricking yourself into thinking you are buying with a margin of safety. This warning applies equally to investors today buying commodity businesses temporarily experiencing an economic boom and fast growing internet businesses with short-term supercharged growth unlikely to persist. Buyers beware.

Bill Ackman, one of my favorite investors and a value disciple, embodies the idea of quality as a margin of safety as fully as anyone. Looking through Ackman’s portfolio he hardly seems to be a value investor in the classical sense. Few of his holdings are priced at “below average” valuations and most are in fact priced far above average. But Ackman is fishing in a stocked pond which he understands deeply.

Specifically, he almost exclusively invests in capital-light royalty businesses with outstanding competitive positions, barriers to entry, and management teams. Of course, he still endeavors to buy each of his positions for far less than he believes it is worth, even if it means paying modestly above-market prices. He relies on business quality and reliable long-duration growth to serve as a sufficient margin of safety against adverse outcomes. Other investors prefer to lean heavier on cheap valuations to serve as their margin of safety.

Both investment styles incorporate the key element of margin of safety, just in different ways. We prefer a mix of both price and quality, in varying degrees, to achieve our desired margin of safety for any individual business. There’s more than one way up the investing mountain but I can’t think of a way that is likely to work over long periods of time without emphasizing the margin of safety concept.

In Summary

To summarize Buffett’s two favorite investing chapters:

Occasionally use undue swings in stock prices to your advantage while mostly ignoring them. And;

Buy securities, whose businesses you understand, for far less than your conservative estimate of intrinsic business value.

As a full time investor it would probably benefit me to make investing sound as complicated as possible. The reality is much different; this stuff is not rocket science. A tireless and unwavering application of fundamentals, such as those laid out in chapters 8 and 20 of Graham’s book, are likely to lead to successful outcomes in the public markets over many years. Sticking to these fundamentals is simple, but not easy. It’s when investors start fooling themselves, forget to apply these sound (though perhaps boring) fundamentals, and go down the path of speculation when trouble arises.

It’s likely we’ll pull together another post or two before the end of the year, but if not, have a great Christmas and holiday season and thanks for reading.

If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com. Thank you for reading!

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.