Brown & Brown

This week I’ll dive in to Brown & Brown and discuss it’s business model and some of the current headwinds that have weighed on the stock. For background on the industry, please see my previous post on insurance brokers.

Brown & Brown started in 1939 as a two-man insurance agency in Florida. In the intervening decades it has grown into the preeminent middle market insurance broker defined by an entrepreneurial, decentralized, and M&A-driven culture. As a serial acquirer with a narrow focus, the company reminds me a lot of Alimentation Couche-Tard, Constellation Software, or HEICO, all of which we’ve written about (or owned) in the past.

Overview

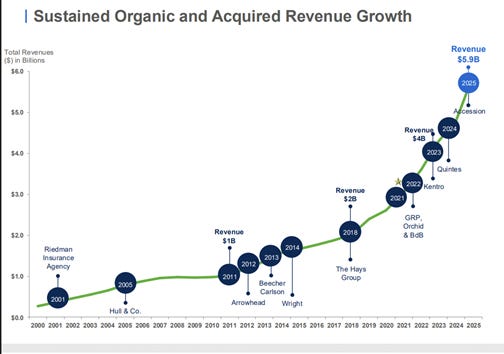

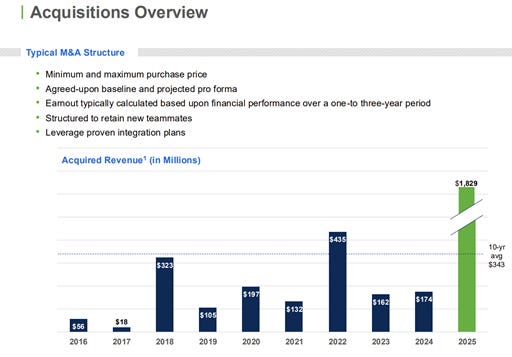

The insurance brokerage market is extremely fragmented and Brown & Brown has been acquiring brokers of all sizes for decades. Revenue has grown organically at an average 3.7% clip since 1998 (the first year I can find easily disclosed organic growth rates). Overall revenue has grown at outstanding 14.4% per year over the same period thanks to the completion of over 650 acquisitions.

Historically Brown conducted primarily tuck-in or bolt-on acquisitions, but in 2025 the company acquired Accession for almost $10B, which was by far the largest deal in the company’s history. Accession is a massive player in specialty insurance and provided Brown & Brown with further scale in the highly profitable specialty distribution segment.

Of course, revenue means nothing if it’s not driving earnings and free cash flow growth. Fortunately, the story is even brighter there, as earnings per share have grown at 15.5% per year since 1998. The fact that Brown and Brown acquired so much revenue growth while generating even higher earnings growth points to management’s skill at identifying and integrating attractive acquisition targets over the last several decades. More on that later.

Business Segments

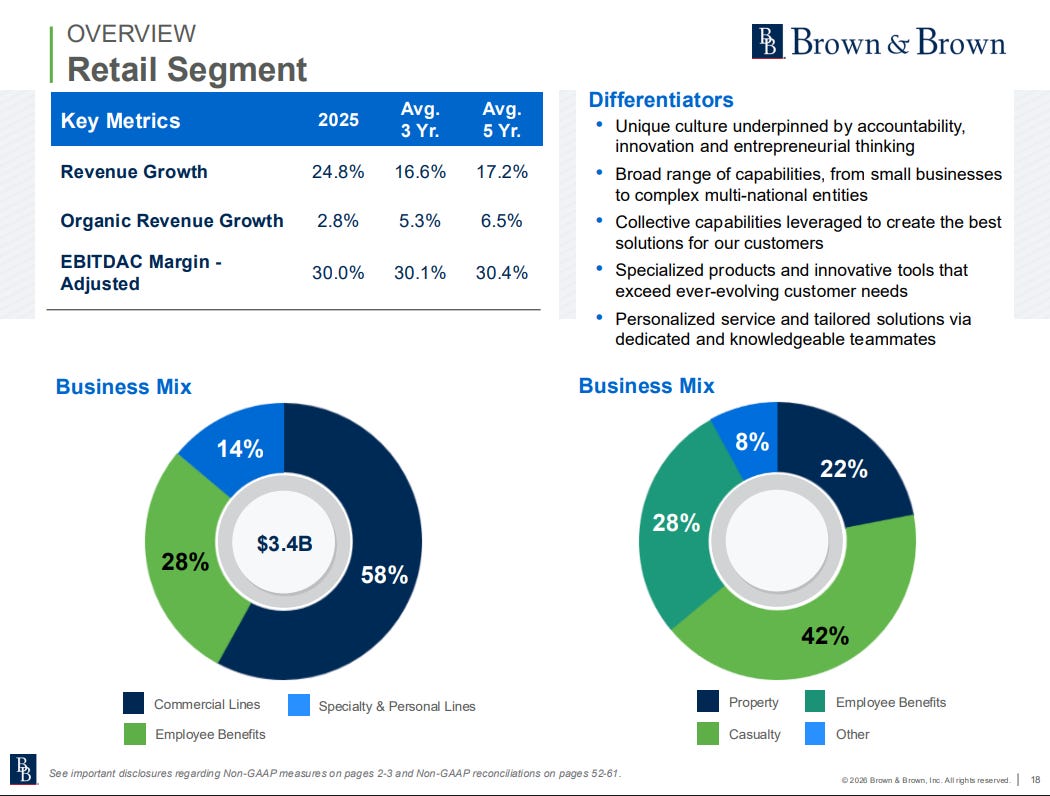

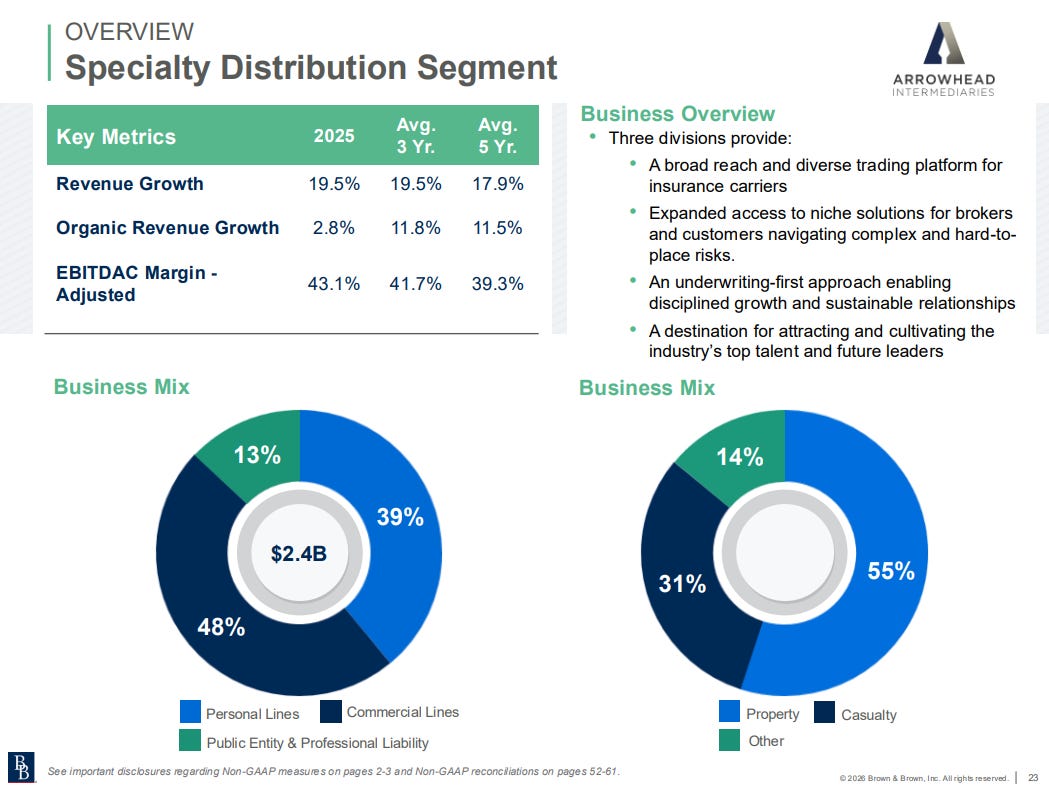

Brown & Brown operates two segments; retail and specialty distribution. Recall from last weeks’ post that the difference between retail and non-retail insurance brokerage is not what is being sold but how it is beings old. Both the retail and specialty distribution segment are primarily driven by specialty/niche insurance lines. In the retail segment Brown interfaces directly with the business buying the insurance. In the specialty distribution segment Brown interfaces with other insurance agents who are looking for insurance for their clients.

Here’s how I think of it:

Retail Segment: Brown & Brown Agent -> The Business Buying Insurance (Even if the business needs highly specialized coverage).

Specialty Distribution Segment: Brown & Brown Wholesaler -> An Outside Insurance Agent -> The Business Buying Insurance.

The retail segment makes up about 58% of revenue and has the below business mix.

The specialty distribution segment does business under the Arrowhead banner and offers wholesale brokerage as well as binding authority or “managing general agent” (MGA) services.

As a wholesale broker Brown is the “shopper”. They act as the matchmaker for retail agents when their clients have hard to place risks.

The MGA is more than a shopper, it is also the decision maker. MGAs are the entities/people that hold binding authority on behalf of carriers and do much more than “just” match retail brokers with specialty insurance carriers.

For example, a major insurance carrier might give Brown & Brown a bucket of money and say, "we want to write insurance for marinas, we don't have expertise in that area, but you do. Here are our parameters, go run the program for us."

Arrowhead MGAs do everything from marketing lines to underwriting and pricing risks and binding carriers to policies. They often manage claims as well, meaning an MGA often acts like an insurance company without taking the underwriting risk. The programs are then distributed through a network of thousands of independent agents.

Brown & Brown is largely U.S.-centric with 86% of revenue coming from the U.S. 10% of revenue is from the U.K. and 4% elsewhere.

Business Model Advantages

Insurance brokers are inherently good businesses. They are capital light and high margin, high ROIC, and provide an essential service with sticky client relationships.