British American Tobacco: Left for Dead

British American Tobacco: Left for Dead

There’s a price for almost every (profitable) businesses where the valuation is so low that almost nothing needs to go right for the stock to generate attractive returns. After following the company for years, at ~6x earnings and a 10% dividend yield, British American Tobacco (BTI) appears to have crossed that threshold and is now “too cheap to ignore”.

Do you have a “stranded” 401k from a past job that is neglected and unmanaged? These accounts are often an excellent fit for Eagle Point Capital’s long-term investment approach. Eagle Point manages separately managed accounts for retail investors. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Background

There are many solid overviews and deep dives written about BTI so I won’t go into great depth on the history of the business. I would suggest reading Invariant’s Substack to get up to speed. He does a far better job at breaking down the tobacco industry than I ever will. Other good resources are Trevor Scott’s recent article and Librarian Capital’s Substack.

At a high level, British American Tobacco sells a wide variety of nicotine products all over the world. The company’s roots go back to 1902 when the UK’s Imperial Tobacco Company formed a joint venture with the American Tobacco Company. Over its 120+ year history BTI has acquired a plethora of brands. The company took its current form after in 2017 it acquired the 58 percent of U.S.-based Reynolds American that BTI didn’t already own at a $49B valuation.

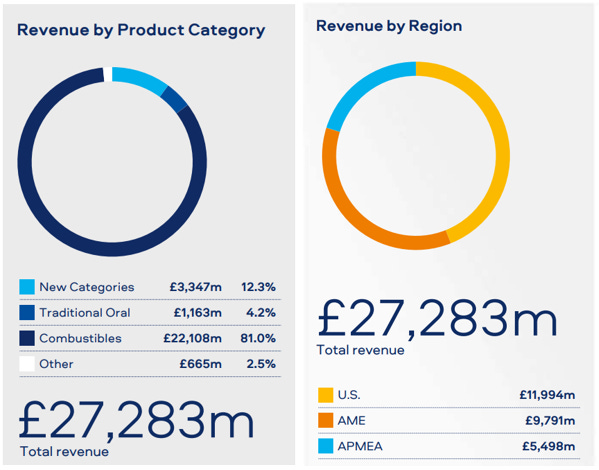

BTI generates revenue from four categories; combustibles, new categories, traditional oral, and other. Revenue is split 44/36/20% between the U.S., the America’s and Europe, and Asia-Pacific/Middle-East, respectively.

Most of the company’s revenue (81%) is still tied to combustibles, or traditional cigarettes. BTI sells 555 billion sticks per year and operates 38 manufacturing facilities in 36 markets. For better or worse, the cigarettes business is and will continue to be an absolute cash cow for tobacco companies for the foreseeable future. This segment has funded the development of smokeless products, which are the future of the industry. The largest global cigarette brands owned under the BTI banner are Dunhill, Kent, Lucky Strike, Pall Mall and Rothmans.

Smokeless “New Categories” include Vapour, which are battery powered e-liquid “vapes” that use nicotine but no tobacco. Heated products and modern oral are the other two main reduced-risk products (RRPs). BTI’s flagship vapour brand is Vuse which has overtaken Juul as the dominant Vapour brand in the U.S. Vuse’s market share in the U.S. is around 42%.

Heated products are similar to vapes in that they contain nicotine but do not produce smoke, but the delivery is different. Heated products – like Philip Morris’ IQOS (which we’ve written about in the past) – are products where a device similar in feel to a traditional cigarette is inserted into a battery-powered cartridge that releases nicotine and flavor through precision heating. BTI’s heat-not-burn brand is glo which has struggled to compete with Philip Morris. BTI is in process of releasing a revamped device to better compete in this segment.

Modern oral nicotine products have exploded in popularity around the world, again led by Philip Morris’ (by way of their recent acquisition of Swedish Match) Zyn in the U.S. with BTI’s Velo maintaining a solid presence globally.

Traditional oral products (or snus and snuff) are forms of chewing tobacco that have significantly higher risk of cancer than modern oral products. BTI’s prominent traditional oral brands are Grizzly and Camel Snus.

Smoke-Free Future

British American’s objective is to generate 50%+ of revenue from reduced-risk products by 2035, putting the business in a solid second position behind Philip Morris in smoke-free products. Philip Morris is the far and away leader in RRPs and generates more than 50% of revenue from smoke-free products in 25 markets and more than 40% of its gross profit already comes from the smoke-free segment.

The company has recently sought to address the dual misconception that smoke-free products are not as profitable as traditional tobacco products and the notion that the nicotine industry is in decline just because traditional cigarette volumes continue to wane.

Philip Morris has proven that, shockingly, its heated products (IQOS) are actually more profitable than the already highly profitable cigarettes. BTI’s vapour products are also already at or close to parity in terms of profitability for its U.S. segment, and virtually all of its new category products are contributing to profits around the world.

While cigarette volumes continue to decline at a mid-to-high single digit pace, overall industry revenue is positive thanks to strong pricing power and growth in new categories.

Altria has painted a similar picture in recent years, showing how the overall nicotine market is quite stable, contrary to the narrative that it’s a declining industry.

Once again, thanks to early investments in new categories, Philip Morris has paved the way and has grown not just revenues but overall volumes for three consecutive years.

You wouldn’t surmise that British American Tobacco has any chance of becoming a “growth company” by looking at its stock price or valuation. Philip Morris has shown that it can be done, and BTI may not be too far away for those with a shred of patience. More on that later.

Competitive Position

It’s no secret that tobacco companies have been outstanding investments over long periods of time, even in the face of perpetually declining volumes. In the 1980’s Buffet succinctly explained why tobacco companies enjoy such great economics:

"I'll tell you why I like the cigarette business. It costs a penny to make. Sell it for a dollar. It's addictive. And there's fantastic brand loyalty."

That pretty much summed it up then and still sums it up today. That said, the businesses have changed quite a bit and the regulatory picture is, of course, completely different today than back in the ‘80s.

While tobacco stocks have earned extraordinary returns over very long periods of time, the last several years have been less kind to shareholders. Fundamentally the businesses are still high quality for a number of reasons. I won’t rehash the decades of regulatory developments that have entrenched the current large players into a dominant position, but to quickly hit on some of the advantages of tobacco companies business model:

Regulatory Moat

Regulatory crackdowns cut both ways for tobacco companies. On the one hand, strict requirements to warn consumers about the potential harm from tobacco use, increasing tax burdens, and advertising bans certainly hamper the growth potential of all segments. On the other hand, these same regulations make it virtually impossible for new entrants to compete in the traditional tobacco space.

The net result of the regulatory crackdowns is a stable market share split between the incumbents with no new competition. With no need to advertise or innovate, cigarettes generate tremendous returns on capital and oodles of free cash flow.

Additionally, in the new categories segment, regulations in most countries are making it increasingly onerous to bring products to market. Legacy tobacco businesses have proven much more adept at developing new products (thanks to the cash generated from legacy products) and, more importantly, they have the know-how and resources to push new products through the regulatory approval process (referred to as the PMTA process in the U.S.).

Given the regulatory environment, the incumbents seem likely to continue the same oligopolistic market structure in new categories that has unfolded in traditional cigarettes over the past several decades. Regardless of your personal opinion, the fact is humans have enjoyed consuming nicotine for thousands of years. My guess is in 10, 20, and 100 years we will still be consuming nicotine in some form.

Pricing Power

Cigarettes are the poster child of pricing power. Year in and year out, Altria, Philip Morris, BTI, and others have been able to raise prices to more than offset consistently falling volumes. With sharper than normal declines in 2023, that wasn’t quite the case as cigarette revenue fell somewhat. I doubt the pricing algorithm is broken for good. The pricing power comes largely from the non-discretionary nature of cigarettes along with brand loyalty.

Eventually (I assume) there will be a day of reckoning where consumers can no longer stomach consistent mid-to-high single digit price increases. That day could come next year, or in twenty years, but until then (and likely for many years beyond), legacy profits will continue to roll in.

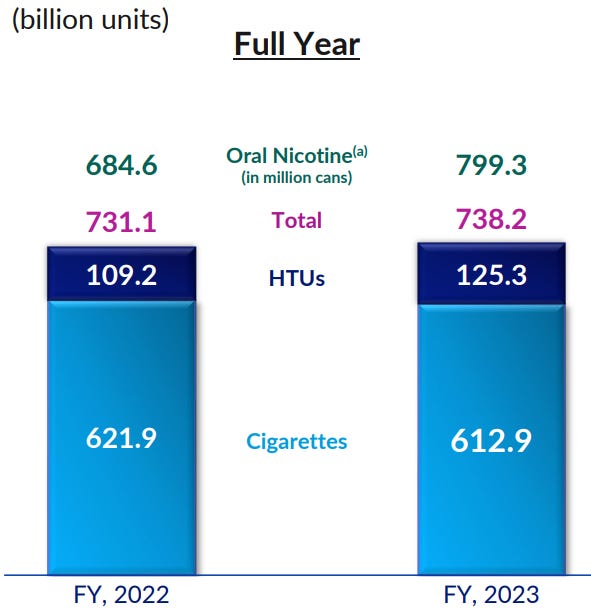

We were initially skeptical of pricing power in the vaping segment given the uncertainty of how much brand loyalty mattered compared to the legacy cigarette business. However, in 2023 BTI hiked prices for U.S. vapes by 20% to drive profitability. Despite this large price increase, volumes only declined 6.6% resulting in ~14% revenue growth for the category. This bodes well for future pricing power and profitability.

Non-Cyclicality

We love businesses that are largely uncorrelated to extrinsic factors like interest rates, stock markets in general, and other unpredictable macroeconomic indicators. While heightened inflation has certainly hurt BTI’s business to some degree given how pinched low-end consumers feel, the tobacco industry is highly resilient and predictable compared to most industries.

Why is BTI’s Stock so Cheap?

As I mentioned, BTI trades for around 6x earnings and, excluding their 29% ownership in ITC Limited (formerly the India Tobacco Company) and the earnings from ITC attributed to BTI, the core business trades for around 4x earnings. This is insanely cheap for any business; what is going on?

There are an amalgamation of issues - some company-specific some industry in general – that are working together to create an extremely cheap valuation.

“Sin Stock” Discount

Starting with the obvious – BTI is a tobacco company. Tobacco companies are very much out of favor in general thanks to the “sin” factor and ESG mandates. Most professional investors and fund managers either can’t or won’t be seen owning shares in a tobacco company. This alone creates a major valuation discount.

Perceived Dying Industry

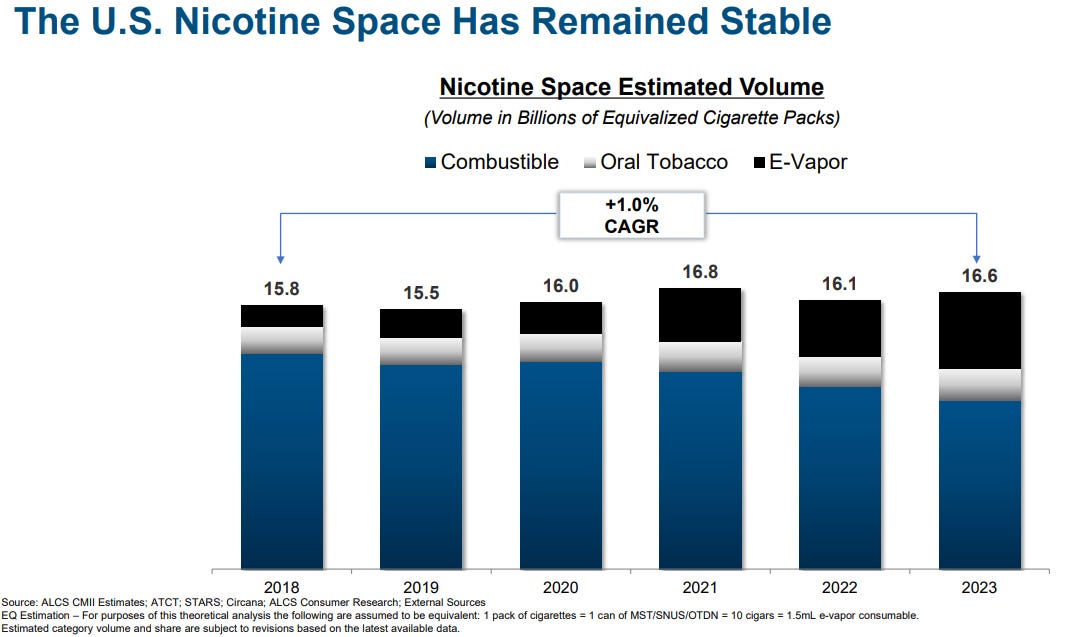

Next, U.S. tobacco volumes have experienced accelerating declines in recent years. During the pandemic there was a temporary increase in volumes (driven by stay at home trends and stimulus payments). In the years since, volume declines have picked up and in 2023 its estimated overall industry volumes were down 8%. It’s likely that short-term macro headwinds accounted for 3-4% of the decline and the secular decline rate is closer to 5-6%. Still, an 8% headline industry decline raises alarm bells for investors.

As shown above, the overall nicotine market is actually growing. It’s not growing fast given the declines in cigarettes that new categories need to absorb, but it’s growing nonetheless.

Proposed U.S. Menthol Ban

The U.S. recently introduced a proposal to ban menthol flavored cigarettes. This could represent an outsized risk to BTI as they hold the largest share of the menthol market. More than half of BTI’s U.S. cigarette sales are tied to menthol flavors. Some studies have suggested banning menthol flavors could have an outsized impact on smokers quitting – causing up to 25% of smokers to quit. In reality it’s not clear there will be a major, if any, impact on BTI’s U.S. business even in the event of a country-wide menthol ban.

Management claims it will retain 80%+ of menthol smokers – a result that would be consistent with how menthol bans have played out in California, Canada, Turkey, and elsewhere in the EU. It seems probable that menthol bans have a de minimis impact on smoker retention; smokers either switch from menthol to regular flavors or move to new categories like vapes.

In addition to the fuzzy impact a widespread menthol ban will have on BTI’s business, it will take years to unfold. If and when the FDA does implement a menthol ban, all of the tobacco companies will challenge the ruling and it will take many years to play out in the slow motion style of the U.S. courts. All the while BTI will be selling menthol products and paying out the proceeds to shareholders.

Illicit Vaping Products

The company has been grappling with illicit vapes in the U.S. and abroad for several years, and the growing share of illicit products has impacted the growth of BTI’s reduced-risk products business. The company estimates 12% of the global market is comprised of illicit products. In the U.S. it’s no secret that illicit products have flooded the market and are being sold en masse. The company estimates a full 60% of the U.S. vape market is illegal, most of which are unregulated Chinese single-use products. Legitimate tobacco companies are begging for regulators to step in.

There are finally some signs of regulators enforcing selling bans on unapproved nicotine products. Louisiana recently enacted laws to curb the distribution and sale of illicit vaping products. Altria explained the early results in its recent earnings call:

“To stem the sale of illicit products at retail, we work with legislatures in several states that have passed or considering legislation, requiring manufacturers to certify that they are compliant with FDA requirements.

Initial data from Louisiana, one state that passed this legislation, show a significant decline in shipment volume to retail for illegal disposable products and an increase in products [ to watch ] manufacturers certified compliance. The good news is virtually all stakeholders agree on the need for a fully regulated marketplace, and our business strategy is aligned with the overwhelming public support for harm reduction as the right path forward to the benefit of smokers and public health.”

Regulation to stem the distribution of unapproved products is slow but seems inevitable. BTI management is similarly lobbying for increased action to curb the flow of unapproved RRPs in the U.S. Any further move to enforce these laws would be a net positive for BTI as their products are more likely to make it through the PMTA process.

Reynold’s Impairment Charge

BTI’s stock was already beaten down for the above reasons, and then in December the company announced it was taking a $31.5B impairment charge on its American cigarette brands. This caused the stock to drop another ~10% to where it trades today.

Rather than carry the goodwill from the 2017 Reynold’s acquisition on its balance sheet indefinitely, the company decided that it was now appropriate to assess the carrying value of those brands over the course of the next 30 years:

“Consistent with our vision to 'Build a Smokeless World', and in combination with the current macro-economic headwinds impacting the U.S. combustibles industry, in 2023 we will take an accounting non-cash adjusting impairment charge of around £25bn. This accounting adjustment mainly relates to some of our acquired U.S. combustibles brands, as we now assess their carrying value and useful economic lives over an estimated period of 30 years. Accordingly, we will commence amortisation of the remaining value of our U.S. combustibles brands from January 2024.”

Regardless of the economic or cash impacts (near or short term) a $31.5B impairment charge is hard for investors to swallow. I happen to think the impairment charge will have a far larger accounting than economic impact, particularly over any reasonable time table. Others may take a different view and conclude the U.S. combustibles business is headed for a cliff, and the associated impairment charge is wholly appropriate. Time will tell.

In case you’re not tired of reading about the negatives, there are some smaller lingering headwinds such as a pending Canadian settlement that is tying up a couple billion dollars of restricted cash, recent foreign exchange headwinds, and inflationary pressures in the U.S. causing a trade-down effect from BTI’s premium combustibles. Also, BTI’s main listing is also in London, which tends to result in a lower valuation. Most of these factors I would consider more transitory than secular.

There’s a lot going on here, and plenty of negatives or possible risks that investors can point to. The pertinent question is; how likely are these risks to harm the business and to what degree are the risks already reflected in the share price?

Valuation and Forward Returns

Rather than follow the sentiment (or the stock price), we prefer to follow the cash when trying to understand a business’s economic characteristics and investment potential. All numbers referenced below are in British pounds.

British American generated about $10B of free cash flow last year. With a market cap of around $51B, the stock trades for just over 5x trailing fee cash flow (or a 20% free cash flow yield). That’s really cheap. Normally companies trading for valuations like this are hyper-cyclical and at a profitability peak, levered equity stubs, businesses whose immediate future is in doubt, etc.

The stock yields around 10%. Generally, when a stock’s dividend yield sniffs double-digits it means the market is questioning the ongoing ability of the company to service the dividend and is effectively pricing in a dividend cut. Last year BTI paid about $5B of dividends, or roughly half of its free cash flow. With only half of free cash flow being used to pay dividends, and not an extreme amount of leverage (leverage ratio is ~2.5x), those dividend payments are far from at risk.

In fact, rather than being cut, the dividend seems likely to grow. Since the Reynold’s acquisition, BTI has raised the dividend around 3% per year, in-line with pretax income and free cash flow growth. If this continues for the next few years, which seems probable, the stock will be yielding ~15% from today’s price. In other words, investors will receive their entire principle back in 7-10 years, and anything beyond dividends is pure upside.

Speaking of upside, let’s say BTI continues to grow earnings at a low-single-digit pace thanks to continued momentum in new categories and continued price vs. volume dynamics in the combustibles segment. This seems like a plausible outcome. Assuming BTI grows the dividend in-line with earnings and begins repurchasing stock again (BTI is steadily delevering at the pace of about 0.2x per year and I expect share repurchases to really ramp up within a year or so) then underlying returns would be in the low double-digits to low-teens. Not bad. But remember, the stock trades for 5x free cash flow.

If, over the next five years, the stock were to re-rate to a still undemanding 8x free cash flow annual returns would be in excess of 20%. For reference, an 8x multiple implies a forever-shrinking business, so any sustained growth suggests a higher multiple. Altria, who has had its fair share of missteps, is fully exposed to the U.S. market, and has nowhere near the upside from New Categories as BTI, trades for around 9x. If the market wakes up in 5-10 years and decides that, like Philip Morris, BTI has a real future in leading the transition to smoke-free products and places a market multiple (of 15x+) onto the business, well, you can do the math on what that means to returns. Needless to say, the upside will take care of itself if things go remotely right. Time is better spent envisioning how they could go wrong.

With a 10% current yield, it would probably take a dramatic reduction in earnings power, a slash to the dividend, and a litany of further negative developments to make losing money at current prices a reality. This means the simple question that investors in BTI need to grapple with is; how likely is it that earnings crumble over the next several years?

One scenario that could play out is that the U.S. enacts a full ban on all menthol products, and it has a dramatic, immediate, and lasting impact on BTI’s economics. This would run contrary to what management expects and what previous menthol bans have suggested. I struggle to envision a scenario where a menthol ban impacts BTI’s ability to continue paying its dividend. Even if U.S. revenues drop by a third, and all of that impact is reflected as a reduction in earnings with no offsets from growing new categories or cost savings, the company would still be paying out only ~70% of free cash flow as the dividend. For comparison, Altria currently pays out ~75% of free cash flow yet trades at a large premium to BTI.

It seems there would need to be some combination of a menthol ban with outsized negative consequences, and an accelerated pickup in smoking declines globally, and a stall-out in new category momentum, and continued inaction against illicit vapes in the U.S., and horrific capital allocation from management to really impair the company’s earnings power. Maybe all of this happens, sure, but it seems like a stretch.

ITC Ownership

I almost forgot to mention, this is all before considering the fact that BTI owns 29% of ITC (formerly known as the India Tobacco Company). ITC is, you guessed it, a high-quality leading tobacco company in India. BTI’s ownership in ITC is worth around $18B (USD), or close to 27% of the current market cap despite accounting for <5% of BTI’s reported profits.

BTI would like to maintain a 25% ownership stake in ITC because of the veto rights it confers. Recently management has signaled a willingness to reduce its stake in ITC to unlock further cash to return to shareholders. While BTI is not selling its full position any time soon (nor should they), it provides yet another cushion and optionality against some of the potential negative outcomes mentioned above.

Takeaway

There is plenty of hair on British American Tobacco. The combination of being a “sin stock”, a foreign listing, the (seemingly incorrect) perception of participating in a declining market, and a recently announced large impairment charge have resulted in investors abandoning BTI.

You can kill any investment with enough doom-loop and what-if analysis. Howard Marks calls this the “limits to negativism”. At some point the price compensates for the pessimism in a business, and BTI investors need to ask themselves how much worse the future needs to look than the past to incur losses from here. Simply maintaining the status quo should prove quite profitable.

Not much has to go right in the business for handsome returns for investors. If reduced-risk products continue to gain momentum, a menthol ban proves non-draconian, the U.S. cracks down on illicit vapes, smoking rates don’t fall off a cliff, or the business simply demonstrates its resilient earnings power via continuing dividends and increased share repurchases, today’s prices are unlikely to look rational within a few years.

Do you have a “stranded” 401k from a past job that is neglected and unmanaged? These accounts are often an excellent fit for Eagle Point Capital’s long-term investment approach. Eagle Point manages separately managed accounts for retail investors. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

Excellent writing, thanks for the insight.

Thanks Dan. Nice write up. Do you have any idea if illicit vapes have loyalty like cigarettes have? My understanding is that at least some of the time, the vape "juice" can be used with a variety of consumption devices.