Bank Of Hawaii Has A Wide Moat But Little Opportunity To Reinvest

Moats aren't always metaphors. In Bank of Hawaii's case, their moat is literally the Pacific ocean.

Hawaiians are proud of their home, lineage, and culture, as they should be. This makes them unusually loyal to their own institutions, and leery of those imported from the mainland. This is why no mainland banks operate on the island.

The Hawaiian banking industry is an oligopoly. Four banks control 90% of deposits and just two banks control 70%. Bank of Hawaii is one of those two, with a 32% share.

Source: FDIC

Markets structured as oligopolies tend to allow all participants to earn above-average returns on their capital. Just look at the Canadian banks. In theory, high returns should attract new competition. In 1992, it did. Bank of America (NYSE:BAC) purchased Honolulu Federal Credit Union to give it a toehold on the island.

But they sold in 1997 to American Savings Bank, a subsidiary of Hawaiian Electric Industries (HE) because they "couldn't achieve critical mass" and "the investment required to improve the profitably of BofA Hawaii could be put to better use elsewhere" (source). Hawaii is too small of a market to interest mainland banks.

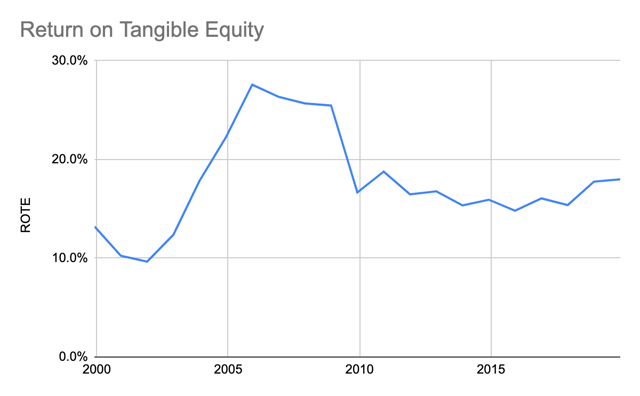

Bank of Hawaii is unusually profitable because it has little competition. Return on assets have been consistently above 1.0% and return on tangible equity has averaged 18%.

Source: Author, data from annual reports

Source: Author, data from annual reports

The key to this superb record is Bank of Hawaii's low cost of deposits. The bank has $16.7 billion of earning assets ($11.0 loans and leases plus $5.7 securities) financed almost entirely by $15.8 billion of deposits which cost it just 0.43% and $1.3 billion of tangible common equity.

Forward Returns

Companies that produce consistently high returns on tangible equity are usually good investments if they can continue to reinvest their profits at high returns. This is where Bank of Hawaii falls short.

Historically, Bank of Hawaii has retained 12% of economic earnings (PTPP-NCOs) and re-deployed it at a 7% rate.

Bank of Hawaii's incremental ROIC, as calculated, probably understates reality since interest rates have fallen over the course of this analysis. Most likely they've reinvested at about their average ROTE, which is 18%. Still, using a 12% reinvestment rate and an 18% incremental ROIC only suggests 2% growth.

Bank of Hawaii's problem is that it cannot reinvest in itself. Hawaii is a small island. Its 11,000 square miles is home to 1.4 million people who produce 0.45% of US GDP. Mature banks can only grow about as fast as GDP, which has been 1-2% lately.

Since the bank cannot meaningfully grow organically, the stock's return will largely depend on how management allocates profits between inorganic growth, dividends, and stock buybacks.

Bank of Hawaii tried to expand onto the US mainland in the late 90s, but wrote some bad loans and beat a hasty retreat in the early 2000s. Memories of that pain should prevent management from empire building outside of the islands.

That leaves dividends and buybacks. Historically, the bank has paid about 50% of profits as dividends and returned the remaining 40% of earnings as buybacks. The stock's median PE is 15x, which means investors can expect a normalized yield of about 6.0% (0.9/15). Added to growth of 1-2% suggests a total return of 7-8%.

That isn't particularly compelling, especially when you consider the risks in the short term.

Credit Quality

Tourism directly and indirectly accounts for 16.9% of Hawaii's GDP, according to Bank of Hawaii's 2019 annual report. From this perspective, the pandemic will have an outsized impact on Hawaii's economy.

There are a couple of mitigating factors, however. First, government and military spending constitute 19.5% of GDP. This piece of the economy is stable and will balance out declines in private sector activity.

Second, Hawaii has had relatively fewer cases of COVID-19. That's one benefit of its isolation. Hawaii is enforcing a 14-day mandatory quarantine for anyone arriving on the islands after March 24th (source). This is keeping visitors low.

The distribution of possible outcomes is admittedly wide. No one knows how bad this could get. Looking back to the 2008-2009 period is probably the best we can do to consider what a downside scenario might entail.

Source: Author, data from annual reports

Since 2005, the net charge-off rate averaged 0.38%. It peaked in 2001 at 1.57%, but that was the result of bad mainland lending outside of its core competency. NCOs peaked again in 2009 at 1.43% and remained elevated in 2010 at 0.94% before returning to normal in 2011 at 0.40%. NCOs returned to normal so quickly because Bank of Hawaii was quick and aggressive about writing off assets in 2009 and subsequently saw meaningful recoveries.

CEO Peter Ho said on the Q1 call that they've improved their portfolio quality a lot since 2008. Since then, they've reduced their exposure to shared national credits, small businesses, land loans, aircraft leasing, and sub-prime consumer loans. These were their biggest problem areas in 2009.

To double check, I looked at Bank of Hawaii's current loan book and applied First Hawaiian's loss rates to them. I used First Hawaiian's loss rates because they provide more granular loss rate data than Bank of Hawaii. Though First Hawaiian has proven to be a more conservative lender than Bank of Hawaii, the numbers should be in the same ballpark as they both focus almost exclusively on the Hawaiian islands.

Note that TCC stands for "through the cycle" and represents NCOs between 2007 and 2019.

Source: Bank of Hawaii 2019 10-K, First Hawaiian Q1 Presentation

The results show that Bank of Hawaii's portfolio recomposition might reduce its net write-off rate by 50% relative to 2009. Unfortunately, the present crisis is not similar, so I chose to use the more conservative (original) 2009 data.

Here are my assumptions:

2020 NCOs peak at 1.5% and take four years to return to normal at 0.4%.

Loans and leases stay constant at $11 billion.

Pre-tax pre-provision income (PTPP) stays constant at $300 million.

There's virtually zero chance that these assumptions prove correct. The point here isn't to predict the future but provide a frame of reference about what could happen.

Source: Author

This suggests Bank of Hawaii could earn about $1 billion pre-tax over the next five years. Notably, it suggests that Bank of Hawaii will not lose money, even in 2020.

Assuming no repurchases and a 15x after-tax multiple, shares might be worth $75 per share. If the bank continues to pay out its current dividend of $2.68, then shareholders will receive $13.40 total over the next five years. Altogether, total returns could be 47% total or 8% annually. This isn't far off what I calculated earlier based on Bank of Hawaii's reinvestment rate.

Risks

If Hawaii cannot reopen its economy, it risks slipping into a major contraction. If tourism spending goes to zero, almost twenty percent of Hawaii's economy will disappear.

Even if Hawaii does reopen, that doesn't mean tourists will come. Hawaiians will need to prove that their island is safe and open for business. I'd expect at least a year of disruption, if not two.

The good news is that Hawaii will always be a desirable place to visit. It has always attracted tourists and always will. The question is when, not if, business will resume as normal.

To model a downside scenario, I doubled the loss rate from the scenario above. That is, net write-offs peak at 3.0% and decline to 0.4% over five years.

Source: Author

In this scenario, Bank of Hawaii would lose a modest amount in 2020. This proves Bank of Hawaii should remain solvent. But the stock could be dead money for a few years while it works though problem loans.

Summary

Bank of Hawaii has a wide moat but no capacity to reinvest in itself. It is smart enough not to "diworsify" abroad and returns 90% of net income to shareholders. The stock tends to trade at a 15x multiple, which limits the benefits of buybacks (you'd get more bang-for-your buck if the stock traded at 10x, for instance). Adding 1-2% of expected growth to 6% of yield suggests total returns of 7-8% annually.

Although the bank looks solvent enough to weather the pandemic, Bank of Hawaii is heavily exposed to the Hawaiian economy and therefore tourism.

Bank of Hawaii's potential returns don't seem to adequately compensate shareholders for uncertainty over how Hawaiian tourism will recover. The stock's wide moat makes it worth following and perhaps buying significantly lower in a crash.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.