Advance Auto Parts: Will this Turnaround Finally Turn?

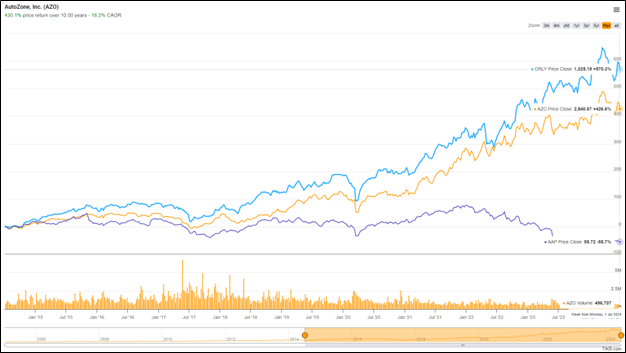

Advance Auto Parts has been a value trap for years. The company operates in an industry that is home to two of the best performing stocks over the past several decades: O’Reilly Auto Parts and AutoZone. Advance Auto Parts, on the other hand, has been in a constant state of catch-up. The gap in the returns of O’Reilly and AutoZone versus Advance has been staggering.

Since 2014 O’Reilly has returned 570%, AutoZone has returned 426%, and Advance has returned, uh, -55%.

With a very similar business model, why have Advance’s returns lagged peers so drastically? For years respected activist investors have taken a run at fixing the company with no success. In 2015 Starboard Value laid out a compelling turnaround plan, but almost a decade later the company remains stuck in neutral. We’ve owned AutoZone for years, admired O’Reilly from the sidelines, and each year scratch our heads at the performance gap between the two leaders and Advance. Recently we have finally tried to build a better understanding of what might be happening, aided in no small part by discussions with Legion Partners this summer.

After a disastrous 2023 for the business and the stock, the latest two prominent activists – Third Point and Legion – disclosed stakes in the company in early 2024. The company recently hired a new CEO and CFO, announced aggressive turnaround plans, and is divesting non-core assets.

The stock looks cheap and prospective returns are enticing if the company can finally close just a portion of the gap to its peers. The situation begs the most dangerous question in investing; is this time different?

Do you have a “stranded” 401k from a past job that is neglected and unmanaged? These accounts are often an excellent fit for Eagle Point Capital’s long-term investment approach. Eagle Point manages separately manage accounts for retail investors. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Industry Overview

Advance Auto Parts is a specialty retailer serving the aftermarket auto parts industry. The market is driven by a mixture of failure-driven repairs (those that cannot wait because your car is broken) and discretionary upgrades. Below is a list of the major parts that the company sells.

The industry has two end customers; commonly referred to as “DIY” and “Pro”/ “Commercial”. The DIY customers are retail car owners that come in to pick up a new battery or set of brakes to service their own car. The Pro segment distributes parts to repair shops who perform the work for end customers.

The business operates under three segments; the core Advance Auto Parts stores (~4,800 locations) which serve a mix of DIY & Pro customers, the CarQuest brand (~1,245 locations), which Advance acquired for $2B in 2014 that serves mostly Pro customers, and the WORLDPAC (325 locations) segment that also serves Pro customers with a focus on import parts.

About 60% of Advance’s revenue is from the Pro Segment, compared to AutoZone which is close to 30%, while O’Reilly splits the different with 47% commercial mix.

The industry structure is favorable. AutoZone and O’Reilly lead a rational oligopoly, with the leaders rarely engaging in heated price competition, and the big guys slowly bleeding market share from a small and fragmented base of disadvantaged mom and pop auto parts stores.

Additionally, the industry tends to be recession resistant if not outright recession proof. During an economic downturn customers opt to save money by performing some of their own car repairs. AutoZone has repeatedly noted that they acquire new customers during downturns, and those customers subsequently don’t leave even when economic conditions improve, meaning there is rarely a reversal in revenue coming out of a downturn. Because much of the business is driven by non-discretionary repairs, the business tends to be quite predictable and robust to extrinsic factors.

Finally, the industry leaders have demonstrated pricing power. When inflation reared its head recently, each business passed along higher input prices straight to the end customer who is generally more dependent on parts availability than price. Because each player behaves rationally, all of the companies are able to pass price along simultaneously meaning the economics of the businesses were preserved despite rampant inflation (something few businesses can claim).

Industry Drivers

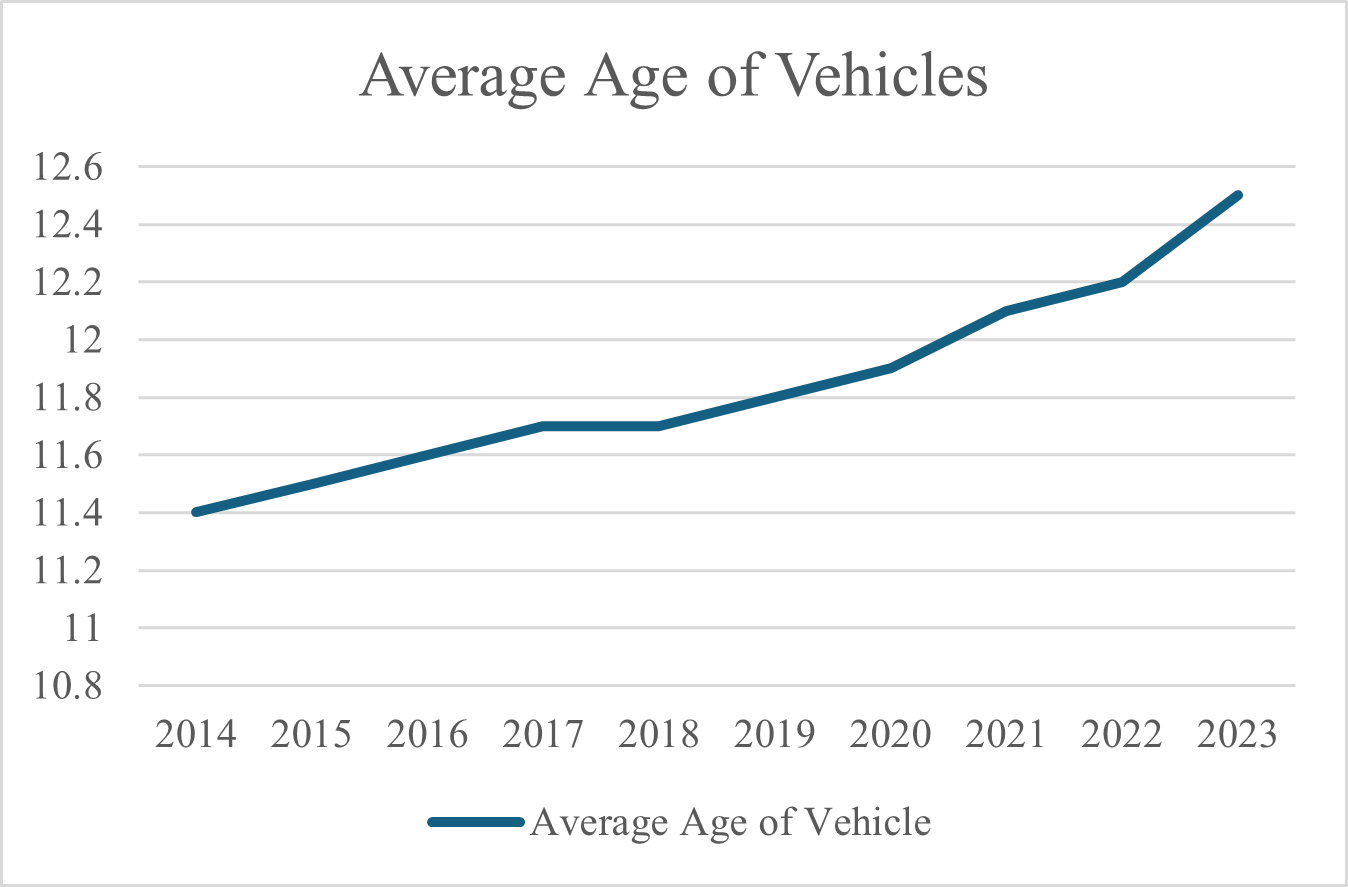

We love businesses where we can easily track identifiable non-financial business drivers. For the aftermarket auto parts industry, it’s very easy. Over multi-year periods industry growth is a result of total miles driven and the average age of vehicles. At around 7 years old cars begin to exhibit higher levels of failures and are generally no longer under warranty. It’s at this point in their life cycle that owners of these vehicles start to become customers of aftermarket auto parts retailers.

Both miles driven and the average age of passenger vehicles on the road have consistently trended in a favorable direction. The only hiccup was during COVID when miles driven went way down for a couple years because everyone was holed up at home. Fortunately stimulus checks came to the rescue during this period as retail customers rushed out to upgrade their vehicles with their stimmy checks.

For decades U.S. passenger car miles driven have trended higher. This is a function of more drivers on the road and more registered vehicles over time.

It’s a simple industry; even I can grasp the concept of older cars breaking down more often and more miles driven meaning more wear and tear on car parts. This all should be great for Advance’s business over the long run provided that they can execute well enough to deliver the demand that is clearly there from end customers. Now let’s explore why Advance hasn’t been able to capitalize, at least so far, on such strong industry dynamics and tailwinds.

Competitive Position

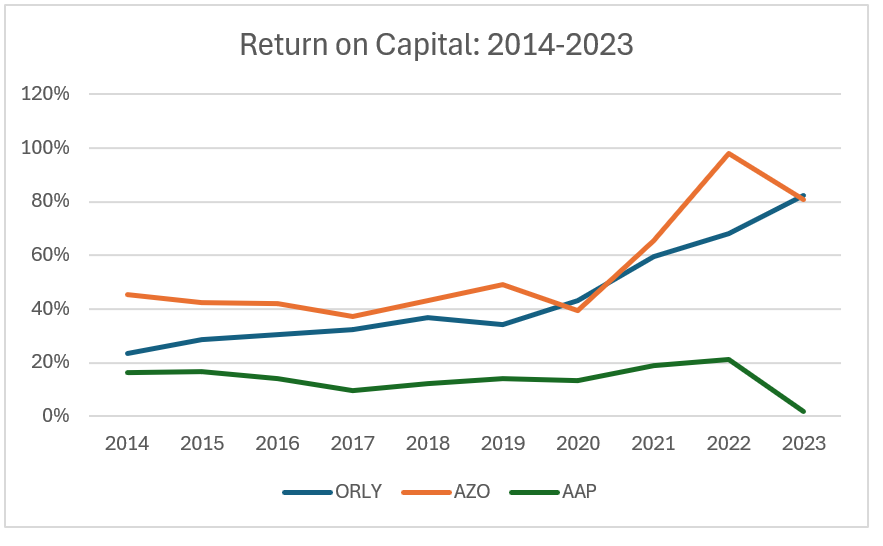

The most helpful way to frame Advances underperformance is by way of comparison of key metrics. As a specialty retailer, Advances intrinsic value will compound (or decay) as a function of how its store base performs. This in turn is a function of margins and sales trends. The results will manifest themselves in a return on capital the store base generates.

Some of the important quantitative company-level metrics to track are gross margin, same-store sales, sales per square foot, and return on invested capital (ROIC). Here is how Advance fares against O’Reilly and AutoZone for each measure:

The takeaway here is that Advance Auto Parts - despite operating in an almost identical industry - sells less per store, grows organically at a persistently lower rate, and is far less profitable and efficient than its peers. While same-store sales trends appear to be in the ballpark of ORLY and AZO, a small but persistent gap really adds up over time, as same-store sales stack on top of each other to drive powerful unit economics. This dynamic becomes evident when looking at sales per square foot, as AutoZone and O’Reilly have really started to create separation thanks to steady outperformance in same-store sales.

We like to analyze businesses with a cash-in, cash-out framework as it helps us get our heads around how much reinvestment a business needs and what returns they earn on reinvested capital. I promise this will be the last comparison between the three businesses (maybe), but here is what it has looked like over the past decade for each business:

AutoZone and O’Reilly have very similar reinvestment and incremental return profiles. The high returns on retained capital enable attractive returns while also returning substantial capital to shareholders via share repurchases. The result has been excellent compounding of per share intrinsic value over the last ten years (and beyond).

Advance, on the other hand, has retained more capital, mostly due to chunky acquisitions that have resulted in the disparate supply chain we’ll discuss below, and earned very poor returns on retained capital. The playbook is there for Advance, but they haven’t been able to execute thus far.

Now that it’s clear Advance is lagging across the board, the question is why?

Parts Availability and Supply Chain

While customers are by no means blind to price discrepancies among competitors, parts availability and in-store experience are the most important considerations when cars breaks down. It’s a major inconvenience when your car breaks down, and time is of the essence to get it fixed, so customers are willing to relegate price to a secondary consideration as long as the gap isn’t too dramatic. Likewise, in the Pro segment, if a mechanic has a car on a lift and needs brakes for a specific model, every minute they sit waiting for the parts to arrive is money out of their pocket.

It’s also for this reason that Amazon has not disrupted the aftermarket auto parts market in any meaningful way. Customers need the part they need today, not in a day or two.

AutoZone and O’Reilly have fine-tuned their supply chains to maximize parts availability using a hub and spoke strategy. Stores are serviced by “mega hubs” which house zillions of parts and can quickly source almost any part not held in the stores that same day. Additionally, the ERP systems, ordering processes, and demand forecasting methods have been refined over the years with a maniacal focus on operating a supply chain that best serves the customers.

Almost inexplicably, Advance, CarQuest, and WORLDPAC operate on largely separate ERP systems with separate SKUs and partially overlapping processes. This means the exact same part from the customers perspective may have multiple different SKUs in Advance’s system depending on the store, creating a massive duplication of effort and hampered visibility into availability. The results can be lost sales, higher costs, and frustrated customers.

Additionally, until recently, the company has not pursued the focused mega-hub strategy that has worked wonders for AZO and ORLY.

Management clearly understands how important parts availability is and that it drives revenue and store performance, as they repeatedly harp on improving availability on earnings calls. As new CEO Shane O’Kelly explained recently:

“The next component of the unified network will be market hubs. As discussed last quarter, this is a new node of our network, and we recently completed a successful pilot. Our market hubs will have an average SKU count of more than 80,000 and will enhance our existing hub network. There are 3 ways that we will be adding market hubs. Number one, converting existing stores with sufficient footprint; number two, converting smaller existing DCs; and number three, greenfielding new locations.”

The 80,000 SKUs available in these market hubs compares to around 23,000 in a traditional Advance store.

Management is also working to consolidate the supply chain onto one system and eliminate duplication of SKUs, which feels like it has been a long time coming.

Time will tell if the conversion and construction of hubs and consolidation of the supply chain will bear fruit in better availability and higher revenue per box, but it’s certainly a step in the right direction.

Leadership and Culture

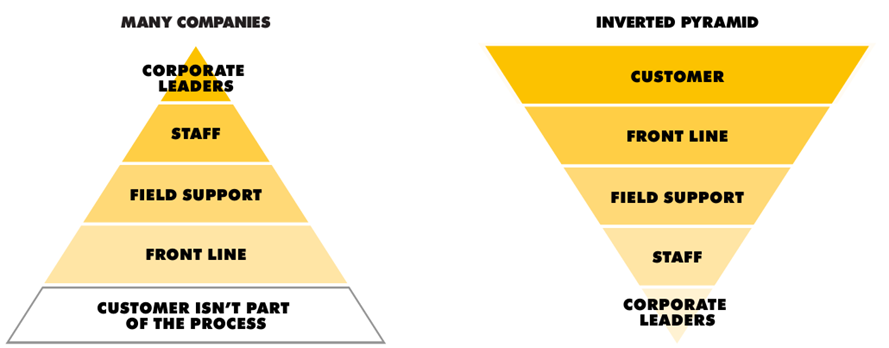

Without actually working in each business, it’s much harder to put a finger on the cultural differences between Advance and its competitors, but anecdotally it appears there has, unsurprisingly, been a major difference in culture at the store level.

AutoZone relentlessly emphasizes how critical the “AutoZoners” are to the success of the business, and by all accounts have incentivized and trained its store associates to be helpful and pleasant to deal with. I may just be taking cues from how well the stock has done, but the company appears to espouse a servant leadership model that puts frontline employee success at the forefront.

The culture on the front lines is a subtle but critical component of the business model given the level of interaction with customers, particularly on the DIY side. If you go to an AutoZone or O’Reilly, the store associates will happily (and for free) help you diagnose a problem, quickly find the part you need, explain how to make the repair, and lend you any tools necessary to complete the job. I get the sense many of these elements are absent, or present to a lesser degree, across the Advance network.

Once again the new CEO is saying the right things. He has only been on the job for a handful of months, but has preached about implementing an “inverted pyramid” culture and incentivizing store employees to turn the culture around and become customer centric. The playbook is there from AutoZone and O’Reilly, but implementing it may prove a semi-herculean task.

Prospective Returns

Management has communicated five key value creation priorities to investors over the last few months, which are:

Exploring the separate sales of Worldpac and Canadian businesses

Significantly reducing costs to remain competitive while reinvesting a portion of these savings into frontline team members

Making strategic organizational changes to position for success

Assessing the productivity and improving the profitability of all assets, and

Consolidating the supply chain.

These are all sensible goals, but the devil is in the details. Let’s take a gander at what a successful outcome might look like.

Management is currently running a process to sell Worldpac and is far down the path to an exit. I expect that they will announce a binding deal this quarter. They have been coy about the valuation that they may receive, but estimates from the activists indicate that Worldpac could fetch close to $2B in proceeds. Anything close to this is very meaningful given the current market cap is just $3.5B. The proceeds are likely to be split between debt paydown, reinvestment to accelerate the supply chain consolidation, and some share buybacks. I’m not sure the market is currently factoring in such a handsome sale price.

An equally interesting opportunity exists in terms of working capital. We’ve written before about the magic of negative net working capital that is at play at AutoZone (and a few other of our holdings, like McKesson) as the business consistently generates more than 100% of net income in free cash flow due to consistent releases of net working capital. Check out the trends in NWC as a percentage of revenue at each business over the last decade:

The effect of negative net working capital means that suppliers essentially finance growth interest-free because customers pay you immediately and you don’t pay vendors for a few months. A knock-on effect of growth releasing cash is that more cash can be returned to shareholders while simultaneously reinvesting in the business, it’s a win-win.

Because of Advances supply chain challenges, smaller scale, and lack of execution, they have not experienced the same benefit from working capital. Management has identified this as a clear opportunity, and it could be very meaningful to shareholders if they can execute.

If Advance can improve working capital efficiency, and get working capital down to, let’s say, 5% of revenue (down from 9% of revenue currently, though still far from AZO and ORLY), that would release more than $500M of cash, or well north of10% of the current market cap.

AutoZone and O’Reilly sport ~13% free cash flow margins. Advance is in a structurally disadvantaged position given its relative scale and starting point, but the current 4% free cash flow margins seem clearly depressed. Once again, if the business can just close a portion of the gap, and return to 7% FCF margins in the coming years, it would provide tremendous tailwinds to returns.

In a scenario where revenue grows 3% per year, FCF margins revert to ~7%, Worldpac sells for $1.5B, and the business releases $500M of cash from working capital improvements, and the stock ends up trading for an undemanding 10x FCF (Advance is presently valued at 14x 2024’s depressed free cash flow), it’s not hard to pencil in 25%+ annual total returns for the foreseeable future. For those keeping tally, a $500M working capital release and $1.5B sale of Worldpac amounts to more than half of the current market cap.

This scenario is not a prediction, it’s simply an illustration of a reasonable outcome if the company is semi-successful in its turnaround efforts. The task is to assess how likely an outcome like this is, and what could go wrong on the downside.

The problem is, the same opportunity exists today that existed in 2015, and it’s tough to shake that nagging feeling that if it was so easy, why haven’t any of the previous management teams been able to execute?

Do you have a “stranded” 401k from a past job that is neglected and unmanaged? These accounts are often an excellent fit for Eagle Point Capital’s long-term investment approach. Eagle Point manages separately manage accounts for retail investors. If you would like to invest with Eagle Point Capital or connect with us, please email info@eaglepointcap.com.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.

Further: https://www.reddit.com/r/advanceautoparts/comments/1chzepo/please_read_before_purchasing_a_battery_at/

"Last week, 4/23/24, my car battery died. On the Advance Auto Parts website I found an in-stock $89.99 "Value" battery for my 2013 Chevy Captiva Sport. I had my car jumped and went to the Boynton Beach, FL location to purchase the battery and have it installed as I am an older man without any tools or mechanical knowledge and their website indicates free installation. Employee Thomas S. said that there was no such Value battery for my car. After much back and forth I was told that if my car did not say SPORT on the back of the vehicle then my car was not a SPORT model. After checking and returning inside, I informed him that it does not say SPORT on the back but told him that is the make and model of my car. He proceeded to tell me that the least expensive battery was $214.99. I was so confused and had no choice but to purchase the battery. He then informed me that he only had 3 employees in the store and they could not install or assist me with the installation. I was very surprised as they weren't even busy. After inquiring, he said he did not have any tools to let me use. Without help, I managed to get my car started and take the new battery home and find someone in my community to assist me with installation.

I then went back to the company website to verify the Value Battery by entering my VIN number. Indeed, the $89.99 value battery was displayed as an option. I immediately returned to the store and inquired as to why he had upsold a battery to me when I had requested the VALUE battery which was on the website for my make/model. We went back and forth as he kept telling me that I was wrong. When he realized that I was not going to back down he started to look in the system and say, "Oh, I must have pulled up a different vehicle." I was dumbfounded how that was possible as we discussed what vehicle it was and he had repeated it to me numerous times after telling me that I did not have a SPORT model. "

To capture the point Dan has made I guess?

https://www.reddit.com/r/advanceautoparts/comments/rv6yrc/i_will_never_ever_shop_at_advance_auto_parts_again/

"I visited my AAP that I've been a customer of for the past 10 years or so. I wanted THIS item and he explained he didn't have it in stock, but could either get it for me OR I could visit the store on Edgewood and Commonwealth as they had 3 in stock. No big deal, I'll go there and get it and I wished the guys, "Happy New Year."

I arrived at the AAP on Edgewood and asked the young lady if she had the product of which she replied, "I have 3, how many do you want? Just 1. Thanks!" and she brings it up to the counter and proceeds to tell me the price is now "36.99." I show her the website and she states, "We don't match our online prices."

OK, let me pay for it online and I'll pick it up. Except I can't pay for it online because the AAP website says the closest store that has it in stock is 40 miles away in St. Augustine. So I asked, "So I can't buy it directly from you for $20,99, I have to go to St. Augustine to pick one up because the APP website says you're out of stock when you actually have 3 in stock?" "That's right" was her response.""